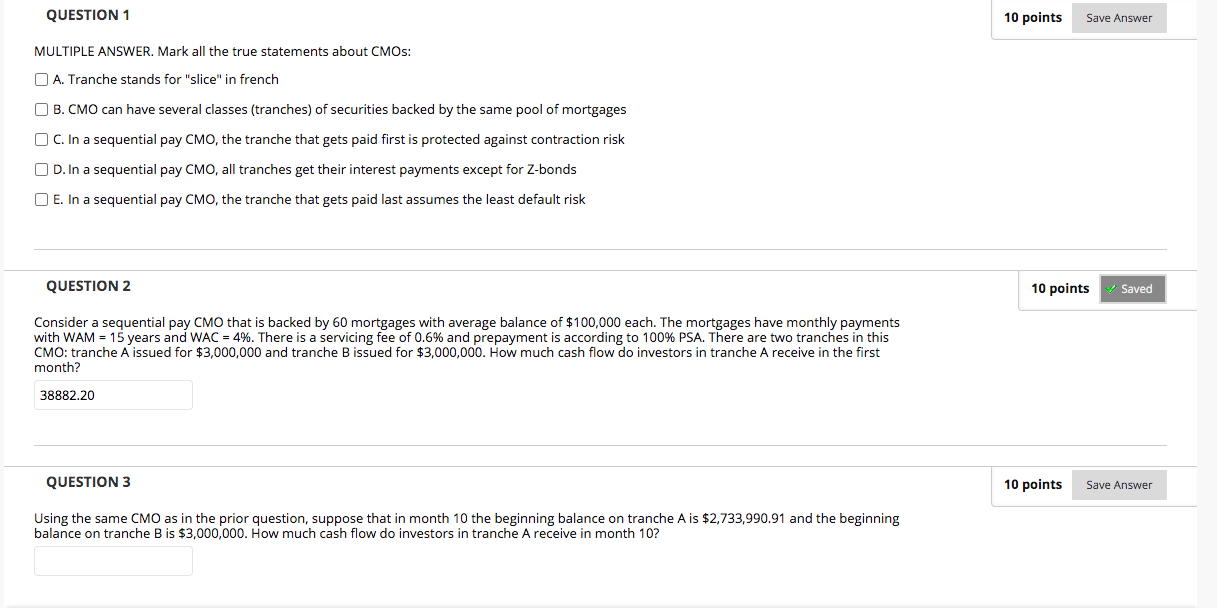

QUESTION 1 10 points Save Answer MULTIPLE ANSWER. Mark all the true statements about CMOs: A. Tranche stands for "slice" in french B. CMO can have several classes (tranches) of securities backed by the same pool of mortgages C. In a sequential pay CMO, the tranche that gets paid first is protected against contraction risk OD. In a sequential pay CMO, all tranches get their interest payments except for Z-bonds E. In a sequential pay CMO, the tranche that gets paid last assumes the least default risk QUESTION 2 10 points Saved Consider a sequential pay CMO that is backed by 60 mortgages with average balance of $100,000 each. The mortgages have monthly payments with WAM = 15 years and WAC = 4%. There is a servicing fee of 0.6% and prepayment is according to 100% PSA. There are two tranches in this CMO: tranche A issued for $3,000,000 and tranche B issued for $3,000,000. How much cash flow do investors in tranche A receive in the first month? 38882.20 QUESTION 3 10 points Save Answer Using the same CMO as in the prior question, suppose that in month 10 the beginning balance on tranche A is $2,733,990.91 and the beginning balance on tranche B is $3,000,000. How much cash flow do investors in tranche A receive in month 10? QUESTION 1 10 points Save Answer MULTIPLE ANSWER. Mark all the true statements about CMOs: A. Tranche stands for "slice" in french B. CMO can have several classes (tranches) of securities backed by the same pool of mortgages C. In a sequential pay CMO, the tranche that gets paid first is protected against contraction risk OD. In a sequential pay CMO, all tranches get their interest payments except for Z-bonds E. In a sequential pay CMO, the tranche that gets paid last assumes the least default risk QUESTION 2 10 points Saved Consider a sequential pay CMO that is backed by 60 mortgages with average balance of $100,000 each. The mortgages have monthly payments with WAM = 15 years and WAC = 4%. There is a servicing fee of 0.6% and prepayment is according to 100% PSA. There are two tranches in this CMO: tranche A issued for $3,000,000 and tranche B issued for $3,000,000. How much cash flow do investors in tranche A receive in the first month? 38882.20 QUESTION 3 10 points Save Answer Using the same CMO as in the prior question, suppose that in month 10 the beginning balance on tranche A is $2,733,990.91 and the beginning balance on tranche B is $3,000,000. How much cash flow do investors in tranche A receive in month 10