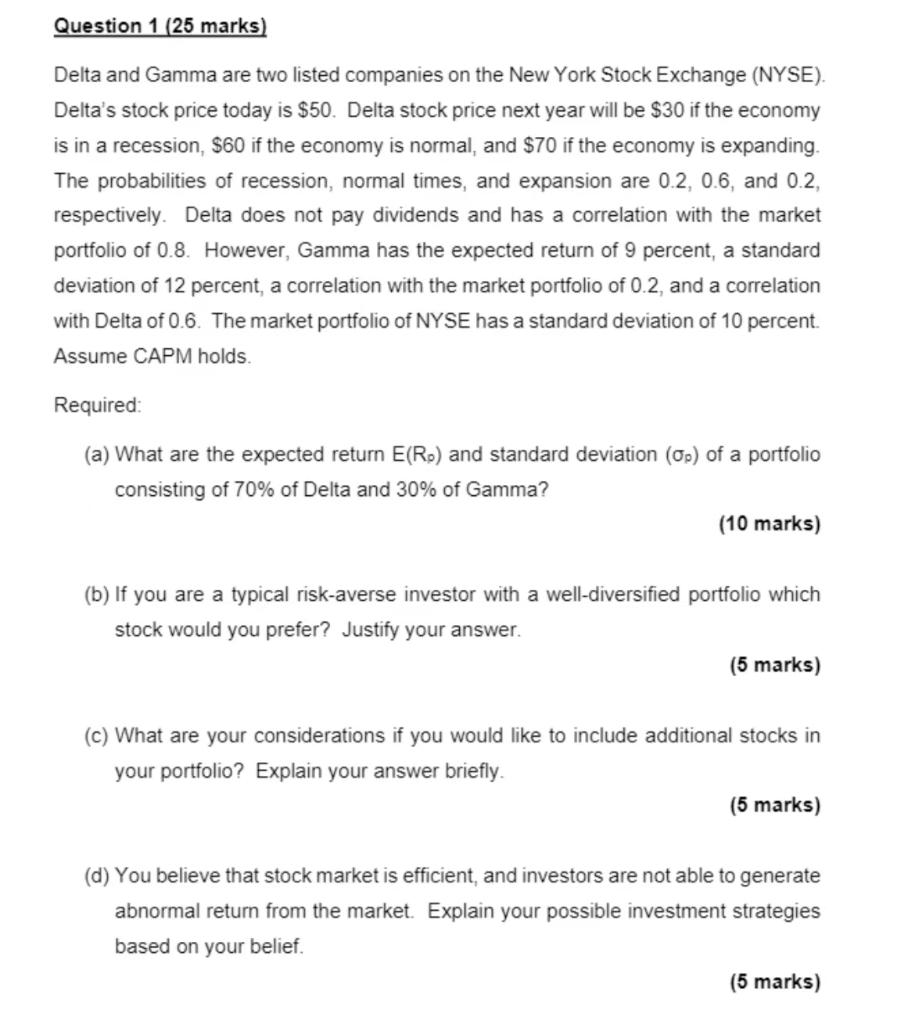

Question 1 (25 marks) Delta and Gamma are two listed companies on the New York Stock Exchange (NYSE). Delta's stock price today is $50. Delta stock price next year will be $30 if the economy is in a recession, $60 if the economy is normal, and $70 if the economy is expanding. The probabilities of recession, normal times, and expansion are 0.2,0.6, and 0.2, respectively. Delta does not pay dividends and has a correlation with the market portfolio of 0.8. However, Gamma has the expected return of 9 percent, a standard deviation of 12 percent, a correlation with the market portfolio of 0.2, and a correlation with Delta of 0.6. The market portfolio of NYSE has a standard deviation of 10 percent. Assume CAPM holds. Required: (a) What are the expected return E(R) and standard deviation () of a portfolio consisting of 70% of Delta and 30% of Gamma? (10 marks) (b) If you are a typical risk-averse investor with a well-diversified portfolio which stock would you prefer? Justify your answer. (5 marks) (c) What are your considerations if you would like to include additional stocks in your portfolio? Explain your answer briefly. (5 marks) (d) You believe that stock market is efficient, and investors are not able to generate abnormal return from the market. Explain your possible investment strategies based on your belief. (5 marks) Question 1 (25 marks) Delta and Gamma are two listed companies on the New York Stock Exchange (NYSE). Delta's stock price today is $50. Delta stock price next year will be $30 if the economy is in a recession, $60 if the economy is normal, and $70 if the economy is expanding. The probabilities of recession, normal times, and expansion are 0.2,0.6, and 0.2, respectively. Delta does not pay dividends and has a correlation with the market portfolio of 0.8. However, Gamma has the expected return of 9 percent, a standard deviation of 12 percent, a correlation with the market portfolio of 0.2, and a correlation with Delta of 0.6. The market portfolio of NYSE has a standard deviation of 10 percent. Assume CAPM holds. Required: (a) What are the expected return E(R) and standard deviation () of a portfolio consisting of 70% of Delta and 30% of Gamma? (10 marks) (b) If you are a typical risk-averse investor with a well-diversified portfolio which stock would you prefer? Justify your answer. (5 marks) (c) What are your considerations if you would like to include additional stocks in your portfolio? Explain your answer briefly. (5 marks) (d) You believe that stock market is efficient, and investors are not able to generate abnormal return from the market. Explain your possible investment strategies based on your belief