Answered step by step

Verified Expert Solution

Question

1 Approved Answer

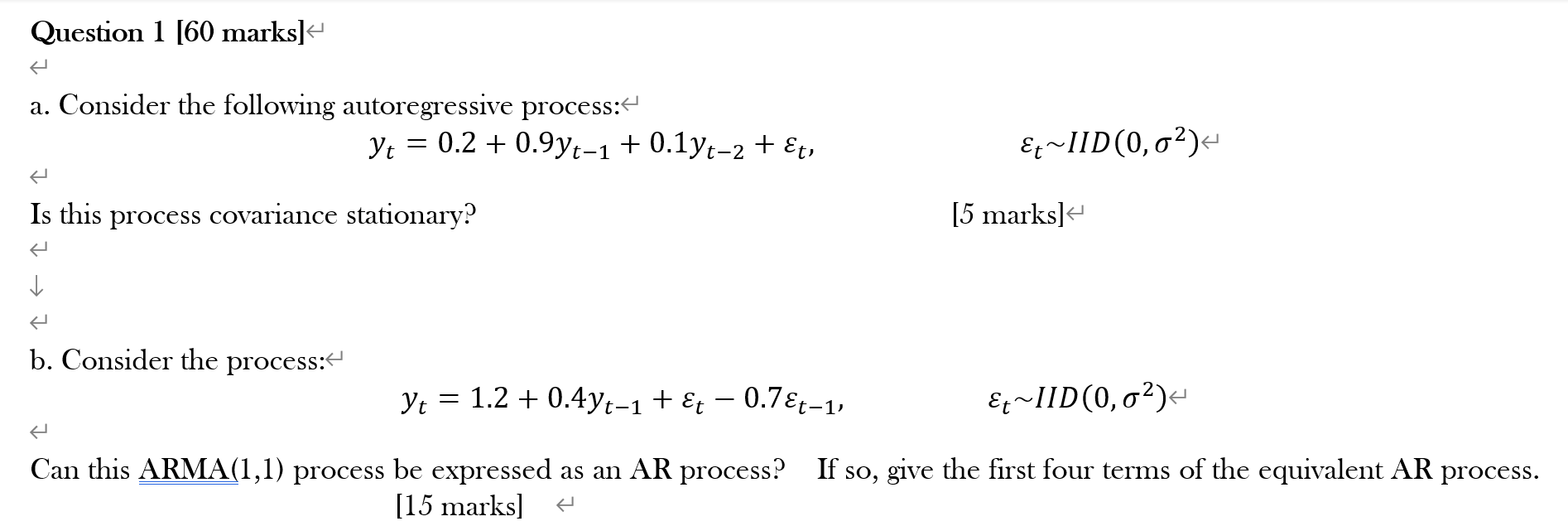

Question 1 [60 marks] a. Consider the following autoregressive process: Question 1 [60 marksle a. Consider the following autoregressive process: Yt = 0.2 + 0.9Yt_1

Question 1 [60 marksle a. Consider the following autoregressive process: Yt = 0.2 + 0.9Yt_1 + 0. I y t _ 2 -k E Is this process covariance stationary. p b. Consider the process: Yt = 1.2 + 0.4yt_1 + Et o.7Et-1, [5 marks]e Can this ARMA(I,I) process be expressed as an AR process? If so, give the first four terms of the equivalent AR process. [15 marks]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Algebra And Trigonometry

Authors: Ron Larson

9th Edition

1285605705, 9781285605708