Answered step by step

Verified Expert Solution

Question

1 Approved Answer

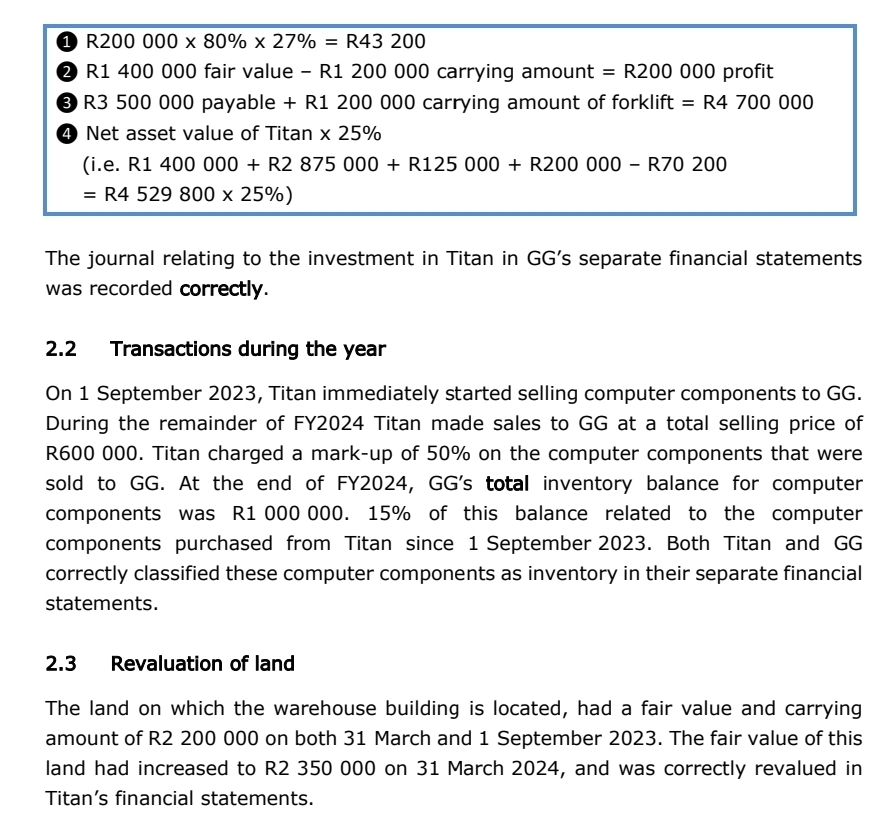

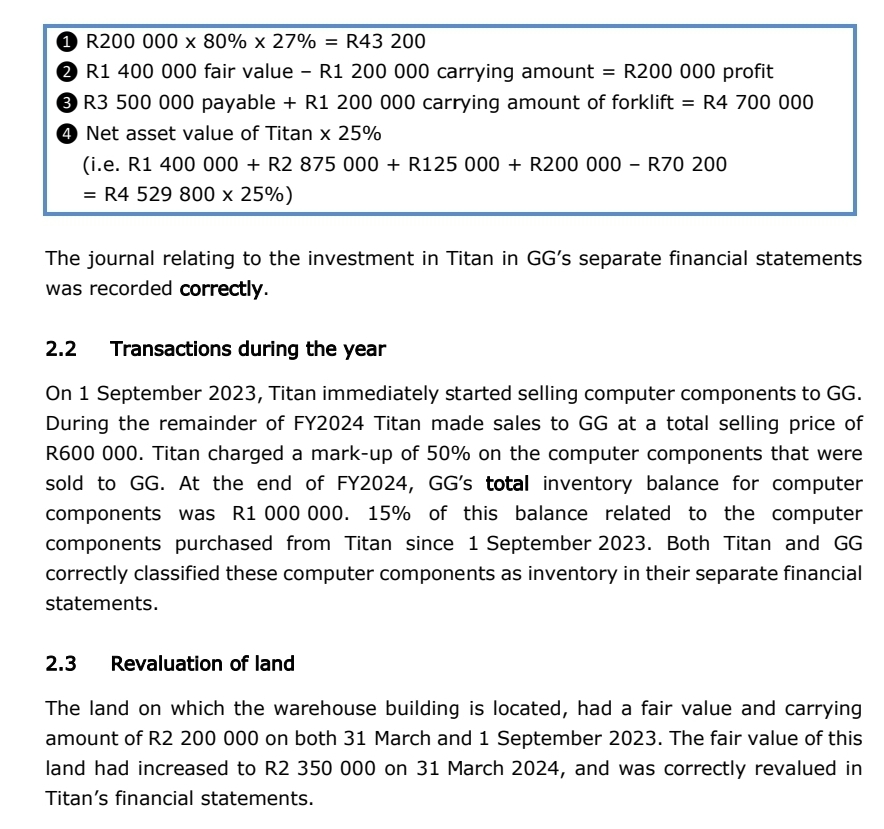

QUESTION 1 ( a ) Explain, with reasons, the errors and / or omissions made by the junior accountant in drafting the at - acquisition

QUESTION

a Explain, with reasons, the errors andor omissions made by the junior accountant in drafting the atacquisition proforma journal entry relating to GGs acquisition of Titan on September

Titan Tech Pty Ltd

Titan is a prominent computer hardware manufacturer based in South Africa that specializes in producing a wide array of computer components including processors, motherboards, and storage devices. These highquality components are supplied to electronic retailers across the country. GG realised that by obtaining a controlling interest in Titan, it could reduce the costs of acquiring computer components.

On September GG acquired a controlling interest in Titan by purchasing ordinary shares from Titan's existing shareholders, who are unrelated to the GG group.

On March Titan's equity consisted of ordinary share capital of Rwhich remained unchanged throughout FY and retained earnings of R This information was confirmed in Titan's FY audited annual financial statements.

All Titan's assets and liabilities were fairly valued on September except for the following items:

On September the carrying amount of Titan's warehouse building the warehouse" used to store Titan's inventory, was correctly determined to be R On the same date the fair value of the warehouse was R The fair value adjustment on the warehouse was correctly calculated to be an amount of R

The warehouse was purchased on September at a cost of R and on the date of purchase, it had an estimated useful life of years, with a nil residual value. These estimates remained unchanged.

The South African Revenue Services SARS grants capital allowances of per annum not apportioned for periods shorter than a year on the warehouse.

GG agreed to pay the following consideration to Titan's previous shareholders in exchange for the controlling interest in Titan:

A cash amount of R payable one year after acquisition date, on August No interest will be charged on this amount. This payment arrangement is beyond the normal credit term of three months.

A forklift used in the warehouse, which had a carrying amount of R and fair value of R on September

GG elected to measure the noncontrolling interest relating to this business combination at their fair value. The fair value of the noncontrolling interest on September was correctly determined to be an amount of R

Draft atacquisition journal entry

GGs junior accountant posted the following atacquisition proforma journal entry on September to account for Titan in the GG group financial statements:

tableAccountDebit,CreditDr Share capital EQDr Retained earnings EQDr Buildings SFPDr Gain on bargain purchase PL Balancing,Cr Deferred tax SFP

Your answer should not include calculations or amounts.

You are not required to prepare correcting journal entries.

Recommendations are not required.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Advanced Accounting

Authors: Joe Ben Hoyle, Thomas Schaefer, Timothy Doupnik

7th edition

1259722635, 978-1259722639