Answered step by step

Verified Expert Solution

Question

1 Approved Answer

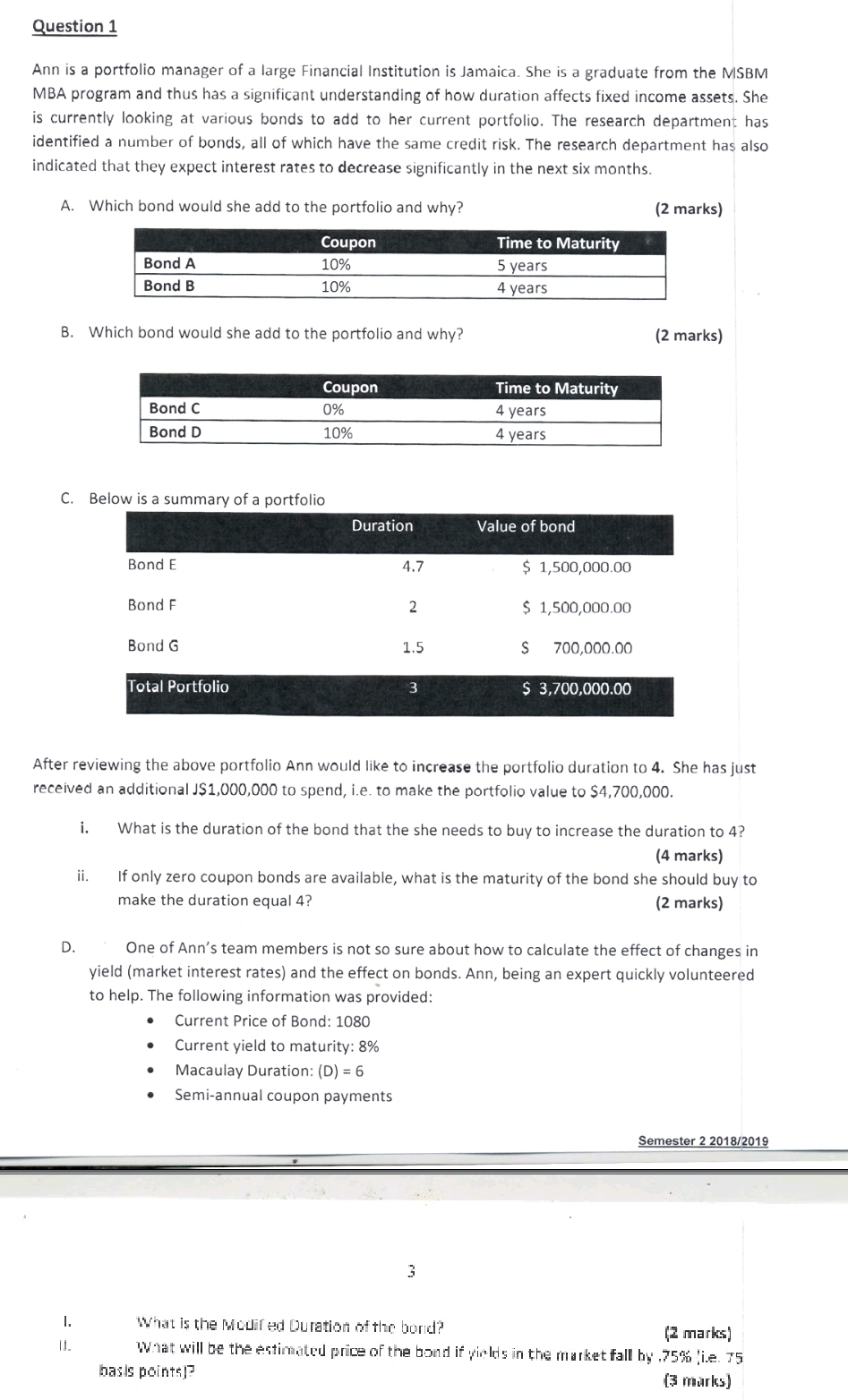

Question 1 Ann is a portfolio manager of a large Financial Institution is Jamaica. She is a graduate from the MSBM MBA program and

Question 1 Ann is a portfolio manager of a large Financial Institution is Jamaica. She is a graduate from the MSBM MBA program and thus has a significant understanding of how duration affects fixed income assets. She is currently looking at various bonds to add to her current portfolio. The research department has identified a number of bonds, all of which have the same credit risk. The research department has also indicated that they expect interest rates to decrease significantly in the next six months. A. Which bond would she add to the portfolio and why? Bond A Bond B Coupon 10% 10% B. Which bond would she add to the portfolio and why? (2 marks) Time to Maturity 5 years 4 years (2 marks) Time to Maturity Bond C Bond D Coupon 0% 4 years 10% 4 years C. Below is a summary of a portfolio Bond E Bond F Bond G Total Portfolio Duration Value of bond 4.7 $1,500,000.00 2 $ 1,500,000.00 1.5 $ 700,000.00 3 $ 3,700,000.00 After reviewing the above portfolio Ann would like to increase the portfolio duration to 4. She has just received an additional J$1,000,000 to spend, i.e. to make the portfolio value to $4,700,000. D. i. ii. What is the duration of the bond that the she needs to buy to increase the duration to 4? (4 marks) If only zero coupon bonds are available, what is the maturity of the bond she should buy to make the duration equal 4? (2 marks) One of Ann's team members is not so sure about how to calculate the effect of changes in yield (market interest rates) and the effect on bonds. Ann, being an expert quickly volunteered to help. The following information was provided: Current Price of Bond: 1080 Current yield to maturity: 8% Macaulay Duration: (D) = 6 Semi-annual coupon payments 3 Semester 2 2018/2019 I. What is the Modified Duration of the bord? (2 marks) 11. What will be the estimated price of the bond if yields in the market fall by .75% i.e. 75 basis points]? [3 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Answer A In order to determine which bond Ann should add to her portfolio we need to consider the concept of duration Duration measures the sensitivity of a bonds price to changes in interest rates Ge...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Economics For Investment Decision Makers

Authors: Sandeep Singh, Christopher D Piros, Jerald E Pinto

1st Edition

1118111966, 9781118111963