Answered step by step

Verified Expert Solution

Question

1 Approved Answer

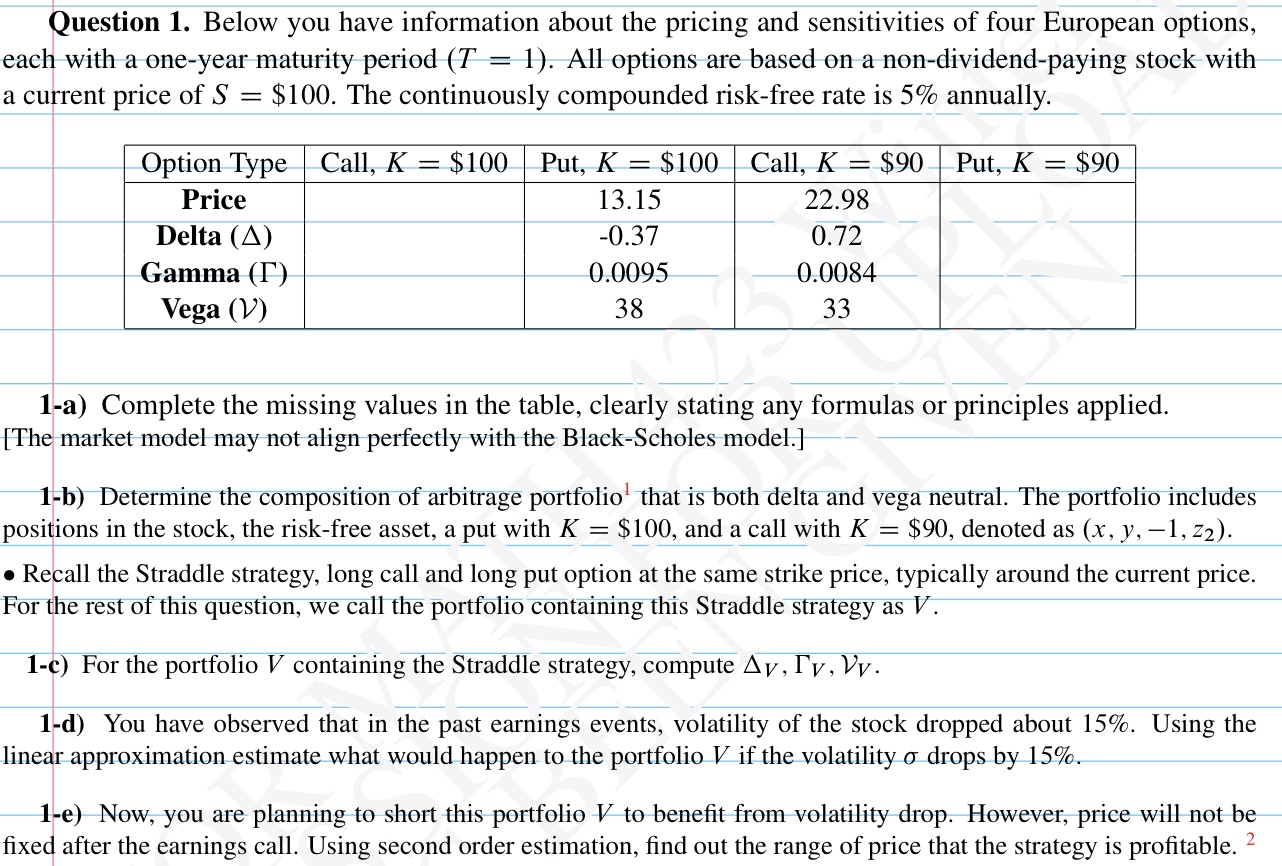

Question 1. Below you have information about the pricing and sensitivities of four European options, each with a one-year maturity period (T = 1).

Question 1. Below you have information about the pricing and sensitivities of four European options, each with a one-year maturity period (T = 1). All options are based on a non-dividend-paying stock with a current price of S $100. The continuously compounded risk-free rate is 5% annually. = Option Type Call, K $100 Price Put, K 13.15 = $100 Call, K = $90 Put, K = $90 22.98 Delta (A) -0.37 0.72 Gamma (F) 0.0095 0.0084 Vega (V) 38 33 1-a) Complete the missing values in the table, clearly stating any formulas or principles applied. [The market model may not align perfectly with the Black-Scholes model.] 1-b) Determine the composition of arbitrage portfolio that is both delta and vega neutral. The portfolio includes positions in the stock, the risk-free asset, a put with K = $100, and a call with K = $90, denoted as (x, y, 1, Z2). Recall the Straddle strategy, long call and long put option at the same strike price, typically around the current price. For the rest of this question, we call the portfolio containing this Straddle strategy as V. 1-c) For the portfolio V containing the Straddle strategy, compute Av, Tv, Vv. 1-d) You have observed that in the past earnings events, volatility of the stock dropped about 15%. Using the linear approximation estimate what would happen to the portfolio V if the volatility drops by 15%. 1-e) Now, you are planning to short this portfolio V to benefit from volatility drop. However, price will not be fixed after the earnings call. Using second order estimation, find out the range of price that the strategy is profitable. 2

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction to Investment Banks, Hedge Funds, and Private Equity

Authors: David P. Stowell

1st edition

978-0123745033, 0123745039, 978-9380931074