Question

QUESTION 1 Cocoa Group (CG) manufactures chocolate-based products, including various chocolate bars for well-known private brands. The company has recently been approached by Allmazing, a

QUESTION 1

Cocoa Group (CG) manufactures chocolate-based products, including various chocolate bars for well-known private brands. The company has recently been approached by Allmazing, a large national supermarket chain, to submit a quotation for the supply of a special-flavoured milk chocolate bar. Each chocolate bar should weigh 100 grams. However, due to uncertainty of demand, Allmazing has requested CG to submit a quotation for three different monthly volumes: 30,000, 40,000 and 50,000 bars. CG has, at present, excess capacity on some of its machines to produce a maximum of 55,000 chocolate bars a month.

The management accountant of CG has been asked to prepare a costing for the chocolate bars required by Allmazing. The accountant has determined that the full cost will consist of four elements: raw materials of 0.40 per bar, wages for direct labour hired when required of 0.30 per bar, fixed manufacturing and administration overheads absorbed at 200% of direct labour wages per bar, and packaging cost of 0.10 per bar. The manufacturing and administration overheads are forecasted as fixed at 30,000 per month, unless output drops to 40,000 bars or below per month, where a saving of 6,000 per month can be made. An additional 4,000 per month can be saved if monthly output drops to 30,000 bars or below. If nothing is produced, all manufacturing and administration overheads will be saved except for 2,000 per month. If CG sells to Allmazing, the volume produced and sold will be determined by the demand of Allmazing.

The company intends to prepare the quotation based on relevant cost plus 50% of relevant cost as mark-up. The sales manager has suggested that as an incentive to encourage higher volumes of purchase from Allmazing, the mark-up be reduced by 10% and 15% respectively if 40,000 and 50,000 bars are purchased per month.

Required:

a) Compute the selling price per bar for each of the three monthly volumes requested by Allmazing. The selling prices should be expressed in and rounded to 2 decimal places. (9 marks)

b) CG produces chocolate cakes for another customer, Sweety Limited. Market research indicates that there will be no demand for cakes if a selling price of 30 is charged. It has also been ascertained that 500 cakes can be sold at a price of 20. The variable cost for the manufacture of a cake is 10. Required: Compute the selling price that maximises revenue. (6 marks)

c) The accountant of CG recently read about activity-based management and has managed to convince the board of directors of its benefits. He is now in the process of identifying the major activities within the company but is unsure of how the degree of disaggregation can be determined.3 BEA2017 Turn over Required: Propose a set of criteria that can be used to determine the degree of disaggregation of activities within the company. (6 marks)

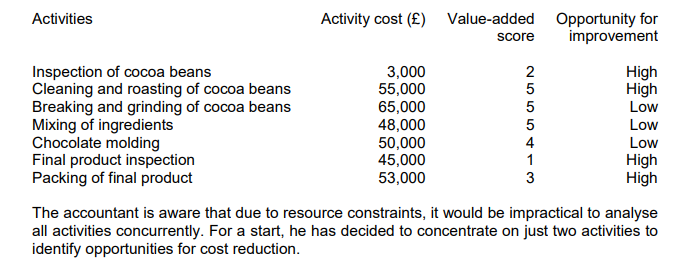

d) Using the criteria proposed in part c), the accountant identified the major activities for the production of chocolate bars. Customers perception of the value-added of each activity (measured on a scale of 1 to 5; 1 being non-value-added and 5 being an activity regarded as the highest value-added) and the current efficiency of the respective activities has also been identified, and are as follows:

Required:

Identify the two activities on which the accountant should concentrate his cost reduction efforts on. Clearly explain your decision process

e) In a recent discussion, confusion arose over the use of the term life cycle costing and fullcost accounting.

Required:

Explain the difference between life cycle costing and full-cost accounting. (4 marks)

f) In order for sustainable development to take root within organizations, Dillard et al. (2005) argued for the adoption of the enlightened management approach.

Required:

Explain the difference between the enlightened management approach and the competitive advantage approach

Activities Activity cost () Value-added Opportunity for improvement score Inspection of cocoa beans 3,000 2 High Cleaning and roasting of cocoa beans 55,000 5 High Breaking and grinding of cocoa beans 65,000 5 Low Mixing of ingredients 48,000 5 Low Chocolate molding 50,000 4 Low Final product inspection 45,000 1 High Packing of final product 53,000 3 High The accountant is aware that due to resource constraints, it would be impractical to analyse all activities concurrently. For a start, he has decided to concentrate on just two activit to identify opportunities for cost reduction. N Activities Activity cost () Value-added Opportunity for improvement score Inspection of cocoa beans 3,000 2 High Cleaning and roasting of cocoa beans 55,000 5 High Breaking and grinding of cocoa beans 65,000 5 Low Mixing of ingredients 48,000 5 Low Chocolate molding 50,000 4 Low Final product inspection 45,000 1 High Packing of final product 53,000 3 High The accountant is aware that due to resource constraints, it would be impractical to analyse all activities concurrently. For a start, he has decided to concentrate on just two activit to identify opportunities for cost reduction. NStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Working Capital Management Applications And Case Studies

Authors: James Sagner

1st Edition

1118933834,1118933850