Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Question 1 Drop down answers 13% 10% 5% 12% Question 2 Drop down answers 1100 1120 1130 1000 Question 3 Drop down answers 10 0

| Question 1 Drop down answers | 13% | 10% | 5% | 12% |

| Question 2 Drop down answers | 1100 | 1120 | 1130 | 1000 |

| Question 3 Drop down answers | 10 | 0 | -10 | 100 |

| Question 4 Drop down answers | 10 | -10 | 20 | 0 |

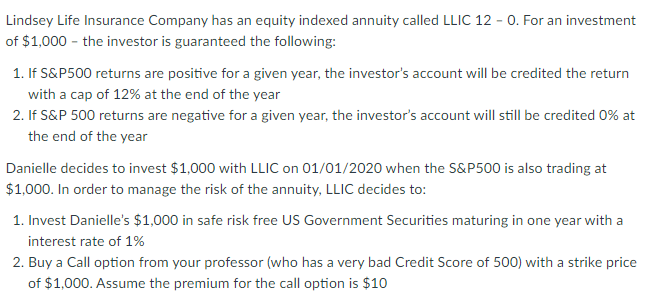

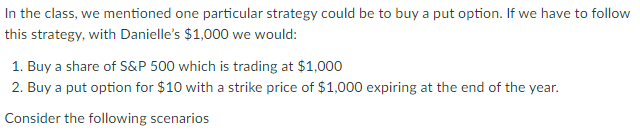

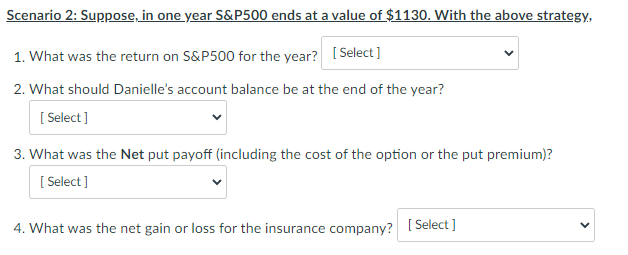

Lindsey Life Insurance Company has an equity indexed annuity called LLIC 12 -0. For an investment of $1,000 - the investor is guaranteed the following: 1. If S&P500 returns are positive for a given year, the investor's account will be credited the return with a cap of 12% at the end of the year 2. If S&P 500 returns are negative for a given year, the investor's account will still be credited 0% at the end of the year Danielle decides to invest $1,000 with LLIC on 01/01/2020 when the S&P500 is also trading at $1,000. In order to manage the risk of the annuity, LLIC decides to: 1. Invest Danielle's $1,000 in safe risk free US Government Securities maturing in one year with a interest rate of 1% 2. Buy a Call option from your professor (who has a very bad Credit Score of 500) with a strike price of $1,000. Assume the premium for the call option is $10 In the class, we mentioned one particular strategy could be to buy a put option. If we have to follow this strategy, with Danielle's $1,000 we would: 1. Buy a share of S&P 500 which is trading at $1,000 2. Buy a put option for $10 with a strike price of $1,000 expiring at the end of the year. Consider the following scenarios Scenario 2: Suppose, in one year S&P500 ends at a value of $1130. With the above strategy, 1. What was the return on S&P500 for the year? [Select] 2. What should Danielle's account balance be at the end of the year? [Select] 3. What was the Net put payoff (including the cost of the option or the put premium)? [Select] 4. What was the net gain or loss for the insurance company? [Select]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forecasting And Predictive Analytics With Forecast X

Authors: Barry Keating, J. Holton Wilson, John Solutions Inc.

7th International Edition

1260085236, 9781260085235