Question: QUESTION 1 Master Bhd manufactures and sels computer parts for the local market. The company is preparing its financial statements for the year ended 31

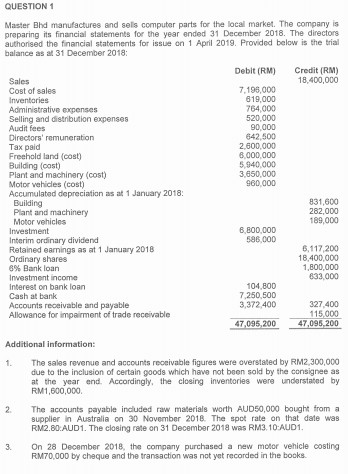

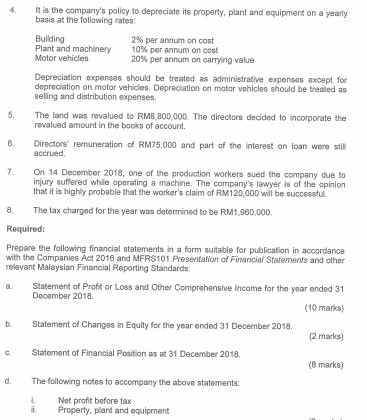

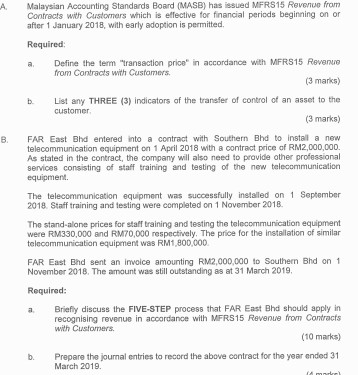

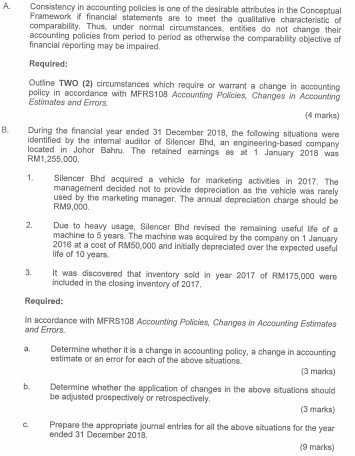

QUESTION 1 Master Bhd manufactures and sels computer parts for the local market. The company is preparing its financial statements for the year ended 31 December 2018. The directors authorised the financial statements for issue on 1 April 2019. Provided below is the trial balance as at 31 December 2018 Debit (RM) Credit (RM) Sales 18,400,000 Cost of sales 7,198,000 Inventories 619,000 Administrative expenses 764,000 Selling and distribution expenses 520,000 Audit fees 90.000 Directors' remuneration 642,500 Tax paid 2,600,000 Freehold land (cost) 8,000,000 Building (oost) 5.940.000 Plant and machinery (cost) 3.650.000 Motor vehicles (cost) 960,000 Accumulated depreciation as at 1 January 2018: Building 831,600 Plant and machinery 282,000 Motor vehicles 189,000 Investment 8,800,000 Interim ordinary dividend 586,000 Retained earnings as at 1 January 2018 6,117,200 Ordinary shares 18,400,000 8% Bank loan 1,800,000 Investment income 833.000 Interest on bank loan 104,800 Cash at bank 7,250,500 Accounts receivable and payable 3,372,400 327,400 Allowance for impairment of trade receivable 115,000 47,095,200 47,095,200 Additional information: 1. The sales revenue and accounts receivable figures were overstated by RM2,300,000 due to the inclusion of certain goods which have not been sold by the consignee as at the year end. Accordingly, the closing inventories were understated by RM1,500,000 2 The accounts payable included raw materials worth AUD50,000 bought from a supplier in Australia on 30 November 2016. The spot rate on that date was RM2.80 AUD1. The closing rate on 31 December 2018 was RM3.10:AUD1. 3. On 28 December 2018, the company purchased a new motor vehicle costing RM70,000 by cheque and the transaction was not yet recorded in the books. It is the company's policy to depreciate its property, plant and equipment on a yearly basis at the following rates: Building 2% per annum on cost Plant and machinery 10% per annum on cost Motor vehicles 20% per annum on carrying value Depreciation expenses should be treated as administrative expenses except for depreciation on motor vehicles. Depreciation on motor vehicles should be treated as seling and distribution expenses 5. The land was revalued to RM8,800,000. The directors decided to incorporate the revalued amount in the books of account B. Directors' remuneration of RM75,000 and part of the interest on loan were still accrued 7. On 14 December 2018, one of the production workers sued the company due to injury suffered while operating a machine. The company's lawyer is of the opinion that it is highly probable that the worker's claim of RM120,000 will be successful 8. The tax charged for the year was determined to be RM1,960,000. Required: Prepare the following financial statements in a form suitable for publication in accordance with the Companies Act 2016 and MFRS101 Presentation of Financial Statements and other relevant Malaysian Financial Reporting Standards: a. Statement of Profit or Loss and Other Comprehensive Income for the year ended 31 December 2018 (10 marks) b. Statement of Changes in Equity for the year ended 31 December 2018 (2 marks) . Statement of Financial Position as at 31 December 2018, (8 marks) d. The following notes to accompany the above statements: Net profit before tax . Property, plant and equipment A Malaysian Accounting Standards Board (MASB) has issued MFRS15 Revenue from Contracts with Customers which is effective for financial periods beginning on or after 1 January 2018, with early adoption is permitted, B Required Define the term "transaction price in accordance with MFRS15 Revenue from Contracts with Customers. (3 marks) b List any THREE (3) Indicators of the transfer of control of an asset to the customer (3 marks) FAR East Bhd entered into a contract with Southern Bhd to install a new telecommunication equipment on 1 April 2018 with a contract price of RM2,000,000 As stated in the contract, the company will also need to provide other professional services consisting of staff training and testing of the new telecommunication equipment. The telecommunication equipment was successfully installed on 1 September 2018. Staff training and testing were completed on 1 November 2018 The stand-alone prices for staff training and testing the telecommunication equipment were RM330,000 and RM70,000 respectively. The price for the installation of similar telecommunication equipment was RM1,800,000 FAR East End sent an invoice amounting RM2,000,000 to Southern Bhd on 1 November 2018. The amount was still outstanding as at 31 March 2019, Required: a Briefly discuss the FIVE-STEP process that FAR East Bhd should apply in recognising revenue in accordance with MFRS15 Revenue from Contracts with Customers. (10 marks) Prepare the journal entries to record the above contract for the year ended 31 March 2019. AHL A B Consistency in accounting policies is one of the desirable attributes in the Conceptual Framework if financial statements are to meet the qualitative characteristic of comparability. Thus, under normal circumstances, entities do not change their accounting policies from period to period as otherwise the comparability objective of financial reporting may be impaired Required: Outine TWO (2) circumstances which require or warrant a change in accounting policy in accordance with MFRS108 Accounting Policies Changes in Accounting Estimates and Errors. (4 marks) During the financial year ended 31 December 2018, the following situations were identified by the internal auditor of Silencer Bhd, an engineering-based company located in Johor Bahru. The retained earnings as a 1 January 2018 was RM1,255,000 1 Silencer Bhd acquired a vehicle for marketing activities in 2017. The management decided not to provide depreciation as the vehicle was rarely used by the marketing manager. The annual depreciation charge should be RM9,000 2. Due to heavy usage, Silencer Bhd revised the remaining useful life of a machine to 5 years. The machine was acquired by the company on 1 January 2016 at a cost of RM50,000 and initially depreciated over the expected useful life of 10 years. It was discovered that inventory sold in year 2017 of RM175,000 were included in the closing inventory of 2017 Required: In accordance with MFRS108 Accounting Policies Changes in Accounting Estimates and Errors. a Determine whether it is a change in accounting policy, a change in accounting estimate or an error for each of the above situations (3 marks) b. Determine whether the application of changes in the above situations should be adjusted prospectively or retrospectively (3 marks) Prepare the appropriate joumal entries for all the above situations for the year ended 31 December 2018 (9 marks) d Compute the restated opening balance of the retained earnings as at 1 January 2018 in the books of Silencer Bhd. (2 marks) (Total: 21 marks) QUESTION 4 A The issues of events after the end of the reporting period are considered important because many items in the accounts are recognised and/or measured based on estimates at the time the items were recorded. The events that occur after the end of the reporting period may provide additional information on the measurement of the items that exist at the end of the reporting period. Required: Briefly explain the following terms according to MFRS110 Events after the Reporting Period Adjusting events b. Non-adjusting events (3 marks) B. Haussei Bhd ends its financial year on 31 December each year. The company is in the process of finalising its financial statements prior to the approval by the board of directors on 31 March 2019. The following information were identified after 31 December 2018 1. On 7 January 2019, Haussel Bhd discovered that as a result of a computational error, depreciation expense for 2018 was overstated by RM24.000 2 On 15 January 2019, Haussei Bhd declared a final ordinary dividend amounting to RM180,000 in respect of the financial year ended 31 December 2018. On 1 February 2019, the chief executive officer of Haussel Bhd announced a major restructuring plan of the business, commencing in June 2019 Required: Determine the nature in each of the above events whether adjusting or non- adjusting with reference to MFRS110 Events after the Reporting Perlod (3 marks) b. Explain the appropriate accounting treatment in each of the above events in the financial statements of Haussel Bhd in accordance with MFRS110 Events QUESTIONS A MFRS137 Provisions, Contingent Liabilities and Contingent Assets prescribes, among others, that a provision shall be recognised when an entity has a present obligation (legal or constructive) as a result of a past event. Required: Explain briefly the term 'obligating event in accordance with MFRS137 Provisions, Contingent Liabilities and Contingent Assets. (2 marks) b. Describe the criteria for an obligation to be recognised as a contingent liability (5 marks) B Coach'e Jam Bhd is considering the following events in finalising its financial statements for the year ended 31 December 2018 1. Coach'e Jam Bhd is currently facing a legal suit from its former employee According to the legal advisor, the company is highly probable to be held accountable for an unfair dismissal act. The case is expected to be settled within one year. The compensation for damages was estimated to be RM180.000 2. The company offers a three-year warranty for every unit of electrical appliance sold. Based on the previous experience is estimated that the company will incur RM10,000 of warranty cost in 2018. 3. During the year ended 31 December 2018, one of the customers claimed that an electrical appliance purchased from the company exploded and had caused severe injuries to him. Legal action has been taken by the customer There is a possibility that the company will be liable but the investigation to determine the real cause of the incident is still ongoing Required: a. For each of the events described above, advise the management of Coach' Jam Bhd on the proper accounting treatment in accordance with MFRS137 Provisions, Contingent Liables and Contingent Assets (8 marks) b. Prepare the relevant journal entries for the above transactions, if any, (4 marks) c. Construct the following extracts of financial statements in respect of the above transactions for the year ended 31 December 2018 1. Statement of Profit or Loss (extract) (2 marks) II. Statement of Financial Position (extract) market QUESTION 1 Master Bhd manufactures and sels computer parts for the local market. The company is preparing its financial statements for the year ended 31 December 2018. The directors authorised the financial statements for issue on 1 April 2019. Provided below is the trial balance as at 31 December 2018 Debit (RM) Credit (RM) Sales 18,400,000 Cost of sales 7,198,000 Inventories 619,000 Administrative expenses 764,000 Selling and distribution expenses 520,000 Audit fees 90.000 Directors' remuneration 642,500 Tax paid 2,600,000 Freehold land (cost) 8,000,000 Building (oost) 5.940.000 Plant and machinery (cost) 3.650.000 Motor vehicles (cost) 960,000 Accumulated depreciation as at 1 January 2018: Building 831,600 Plant and machinery 282,000 Motor vehicles 189,000 Investment 8,800,000 Interim ordinary dividend 586,000 Retained earnings as at 1 January 2018 6,117,200 Ordinary shares 18,400,000 8% Bank loan 1,800,000 Investment income 833.000 Interest on bank loan 104,800 Cash at bank 7,250,500 Accounts receivable and payable 3,372,400 327,400 Allowance for impairment of trade receivable 115,000 47,095,200 47,095,200 Additional information: 1. The sales revenue and accounts receivable figures were overstated by RM2,300,000 due to the inclusion of certain goods which have not been sold by the consignee as at the year end. Accordingly, the closing inventories were understated by RM1,500,000 2 The accounts payable included raw materials worth AUD50,000 bought from a supplier in Australia on 30 November 2016. The spot rate on that date was RM2.80 AUD1. The closing rate on 31 December 2018 was RM3.10:AUD1. 3. On 28 December 2018, the company purchased a new motor vehicle costing RM70,000 by cheque and the transaction was not yet recorded in the books. It is the company's policy to depreciate its property, plant and equipment on a yearly basis at the following rates: Building 2% per annum on cost Plant and machinery 10% per annum on cost Motor vehicles 20% per annum on carrying value Depreciation expenses should be treated as administrative expenses except for depreciation on motor vehicles. Depreciation on motor vehicles should be treated as seling and distribution expenses 5. The land was revalued to RM8,800,000. The directors decided to incorporate the revalued amount in the books of account B. Directors' remuneration of RM75,000 and part of the interest on loan were still accrued 7. On 14 December 2018, one of the production workers sued the company due to injury suffered while operating a machine. The company's lawyer is of the opinion that it is highly probable that the worker's claim of RM120,000 will be successful 8. The tax charged for the year was determined to be RM1,960,000. Required: Prepare the following financial statements in a form suitable for publication in accordance with the Companies Act 2016 and MFRS101 Presentation of Financial Statements and other relevant Malaysian Financial Reporting Standards: a. Statement of Profit or Loss and Other Comprehensive Income for the year ended 31 December 2018 (10 marks) b. Statement of Changes in Equity for the year ended 31 December 2018 (2 marks) . Statement of Financial Position as at 31 December 2018, (8 marks) d. The following notes to accompany the above statements: Net profit before tax . Property, plant and equipment A Malaysian Accounting Standards Board (MASB) has issued MFRS15 Revenue from Contracts with Customers which is effective for financial periods beginning on or after 1 January 2018, with early adoption is permitted, B Required Define the term "transaction price in accordance with MFRS15 Revenue from Contracts with Customers. (3 marks) b List any THREE (3) Indicators of the transfer of control of an asset to the customer (3 marks) FAR East Bhd entered into a contract with Southern Bhd to install a new telecommunication equipment on 1 April 2018 with a contract price of RM2,000,000 As stated in the contract, the company will also need to provide other professional services consisting of staff training and testing of the new telecommunication equipment. The telecommunication equipment was successfully installed on 1 September 2018. Staff training and testing were completed on 1 November 2018 The stand-alone prices for staff training and testing the telecommunication equipment were RM330,000 and RM70,000 respectively. The price for the installation of similar telecommunication equipment was RM1,800,000 FAR East End sent an invoice amounting RM2,000,000 to Southern Bhd on 1 November 2018. The amount was still outstanding as at 31 March 2019, Required: a Briefly discuss the FIVE-STEP process that FAR East Bhd should apply in recognising revenue in accordance with MFRS15 Revenue from Contracts with Customers. (10 marks) Prepare the journal entries to record the above contract for the year ended 31 March 2019. AHL A B Consistency in accounting policies is one of the desirable attributes in the Conceptual Framework if financial statements are to meet the qualitative characteristic of comparability. Thus, under normal circumstances, entities do not change their accounting policies from period to period as otherwise the comparability objective of financial reporting may be impaired Required: Outine TWO (2) circumstances which require or warrant a change in accounting policy in accordance with MFRS108 Accounting Policies Changes in Accounting Estimates and Errors. (4 marks) During the financial year ended 31 December 2018, the following situations were identified by the internal auditor of Silencer Bhd, an engineering-based company located in Johor Bahru. The retained earnings as a 1 January 2018 was RM1,255,000 1 Silencer Bhd acquired a vehicle for marketing activities in 2017. The management decided not to provide depreciation as the vehicle was rarely used by the marketing manager. The annual depreciation charge should be RM9,000 2. Due to heavy usage, Silencer Bhd revised the remaining useful life of a machine to 5 years. The machine was acquired by the company on 1 January 2016 at a cost of RM50,000 and initially depreciated over the expected useful life of 10 years. It was discovered that inventory sold in year 2017 of RM175,000 were included in the closing inventory of 2017 Required: In accordance with MFRS108 Accounting Policies Changes in Accounting Estimates and Errors. a Determine whether it is a change in accounting policy, a change in accounting estimate or an error for each of the above situations (3 marks) b. Determine whether the application of changes in the above situations should be adjusted prospectively or retrospectively (3 marks) Prepare the appropriate joumal entries for all the above situations for the year ended 31 December 2018 (9 marks) d Compute the restated opening balance of the retained earnings as at 1 January 2018 in the books of Silencer Bhd. (2 marks) (Total: 21 marks) QUESTION 4 A The issues of events after the end of the reporting period are considered important because many items in the accounts are recognised and/or measured based on estimates at the time the items were recorded. The events that occur after the end of the reporting period may provide additional information on the measurement of the items that exist at the end of the reporting period. Required: Briefly explain the following terms according to MFRS110 Events after the Reporting Period Adjusting events b. Non-adjusting events (3 marks) B. Haussei Bhd ends its financial year on 31 December each year. The company is in the process of finalising its financial statements prior to the approval by the board of directors on 31 March 2019. The following information were identified after 31 December 2018 1. On 7 January 2019, Haussel Bhd discovered that as a result of a computational error, depreciation expense for 2018 was overstated by RM24.000 2 On 15 January 2019, Haussei Bhd declared a final ordinary dividend amounting to RM180,000 in respect of the financial year ended 31 December 2018. On 1 February 2019, the chief executive officer of Haussel Bhd announced a major restructuring plan of the business, commencing in June 2019 Required: Determine the nature in each of the above events whether adjusting or non- adjusting with reference to MFRS110 Events after the Reporting Perlod (3 marks) b. Explain the appropriate accounting treatment in each of the above events in the financial statements of Haussel Bhd in accordance with MFRS110 Events QUESTIONS A MFRS137 Provisions, Contingent Liabilities and Contingent Assets prescribes, among others, that a provision shall be recognised when an entity has a present obligation (legal or constructive) as a result of a past event. Required: Explain briefly the term 'obligating event in accordance with MFRS137 Provisions, Contingent Liabilities and Contingent Assets. (2 marks) b. Describe the criteria for an obligation to be recognised as a contingent liability (5 marks) B Coach'e Jam Bhd is considering the following events in finalising its financial statements for the year ended 31 December 2018 1. Coach'e Jam Bhd is currently facing a legal suit from its former employee According to the legal advisor, the company is highly probable to be held accountable for an unfair dismissal act. The case is expected to be settled within one year. The compensation for damages was estimated to be RM180.000 2. The company offers a three-year warranty for every unit of electrical appliance sold. Based on the previous experience is estimated that the company will incur RM10,000 of warranty cost in 2018. 3. During the year ended 31 December 2018, one of the customers claimed that an electrical appliance purchased from the company exploded and had caused severe injuries to him. Legal action has been taken by the customer There is a possibility that the company will be liable but the investigation to determine the real cause of the incident is still ongoing Required: a. For each of the events described above, advise the management of Coach' Jam Bhd on the proper accounting treatment in accordance with MFRS137 Provisions, Contingent Liables and Contingent Assets (8 marks) b. Prepare the relevant journal entries for the above transactions, if any, (4 marks) c. Construct the following extracts of financial statements in respect of the above transactions for the year ended 31 December 2018 1. Statement of Profit or Loss (extract) (2 marks) II. Statement of Financial Position (extract) market

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts