Question 1: (Needs Approach)

The correct answers are based on the set of facts and tables provided below. All the data you need to perform the necessary calculations are contained in the tables following the three paragraphs below. Show all your calculations so you can receive partial credit even if you make a mistake. The appearance of your homework is a factor in your grade; therefore, it is suggested it be presented in a professional manner (i.e. pretend it is like something you would prepare for your boss).

Pat and Mandy are married and have a son, Steve, age 8. Mandy, age 29, earns $40,000 annually from her job. Pat, age 31, earns $50,000 annually from his job. Assume that Pat will die before Mandy. The family wants to ensure that they have adequate life insurance on Pat to cover their cash and income needs if Pat dies. Hence, they want to determine if they should purchase additional life insurance on Pat to cover these needs using Needs Approach. (you may find some hints from your textbook, page 207~209)

The tables below provide figures on their: 1) cash needs; 2) present insurance and financial assets; 3) income needs; and 4) income that the family will receive if no additional life insurance is purchased. Use the values in these tables to determine how much, if any, additional life insurance the family should purchase on Pat to cover their needs. In your answer, calculate and show the components of any additional life insurance needed in terms of cash needs and income needs and the total amount of additional life insurance needed.

This exercise assumes that 1) Pat dies immediately; 2) Mandy continues to work if Pat dies, however her earning will not be enough. So the needs shown in the table are net of Mandy's earning; 3) Mandy plans to retire at age 65; and 4) the life insurance proceeds are invested at an interest rate equal to the rate of inflation (so, you do not have to worry about time-value of money issues).

USE THE NEEDS APPROACH TO CALCULATE HOW MUCH ADDITIONAL LIFE INSURANCE ON PAT TO COVER THEIR CASH AND INCOME NEEDS IF PAT DIES!

| Cash Needs: | |

| Estate Clearance | $15,000 |

| Mortgage Redemption | $150,000 |

| Emergency fund | $20,000 |

| Educational Fund | $100,000 |

| | |

| Present Insurance and Financial Assets: | |

| Whole Life Insurance | $150,000 |

| Investments/Savings | $10,000 |

| | |

| Income Needs: | |

| Readjustment Period | $5,000 monthly for 2 years |

| Dependency Period | $5,000 monthly for 8 years |

| Blackout Period | $3,500 monthly for 28 years |

| Mandy's Retirement Period | $3,500 monthly for 25 years |

| | |

| Expected Income from Sources Other than Life Insurance: | |

| Readjustment Period | $3,500 monthly for 2 years |

| Dependency Period | $3,500 monthly for 8 years |

| Blackout Period | $3,000 monthly for 28 years |

| Mandy's Retirement Period | $3,000 monthly for 25 years |

Question 2: (Capital Retention Approach)

Pat estimates that $60,000 is seen as sufficient wealth to meet his familys needs after his death. Currently, the family has $800,000 total assets, including bank saving, securities investment, house, cars, etc. The family currently has $220,000 total liability (e.g., mortgage payoff, auto loan, credit card balance), $135,000 cash needs (e.g., emergency fund, educational fund, and final expenses), and $145,000 non-income-producing capital. Ignore any other potential capital resources or needs, e.g., Social Security benefits.

USE CAPTIAL RETENTION APPROACH TO CALCULATE HOW MUCH LIFE INSURANCE IS NEEDED!

Assuming a 5% rate of return, how much life insurance does the Capital Retention Approach suggest? (You may find some hints at Module 4--> Life Insurance-->Reading). Again, please show all your work and calculations.

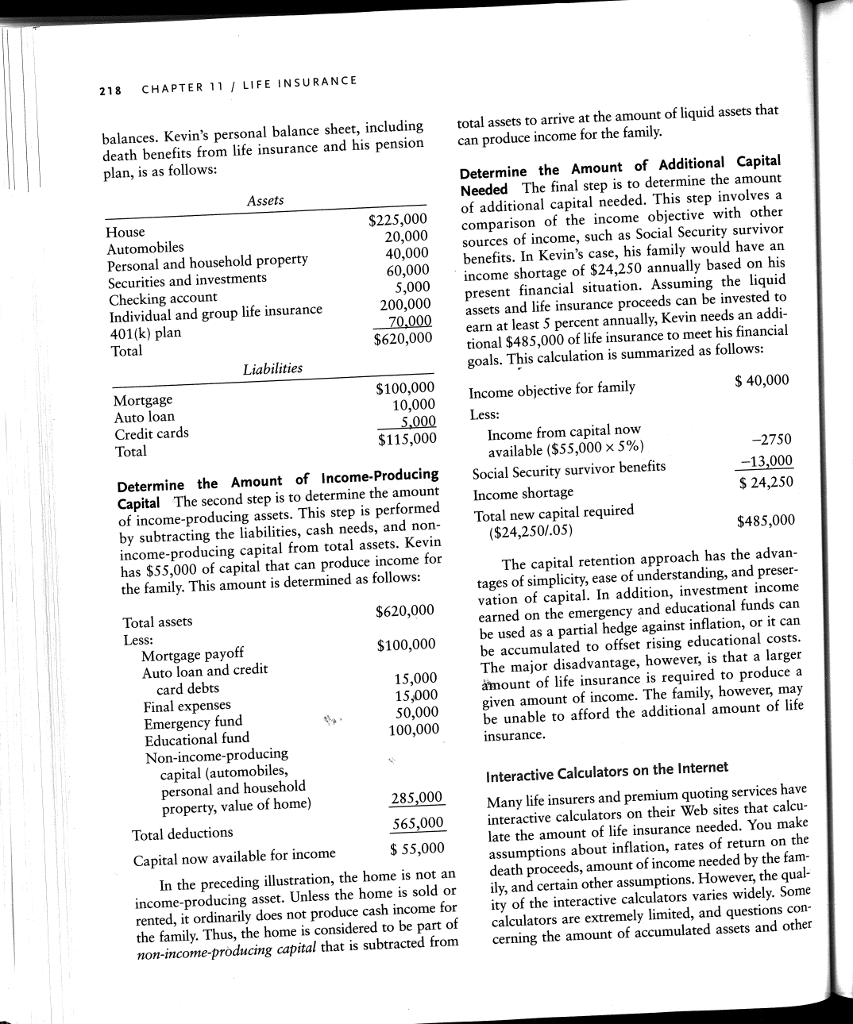

218 CHAPTER 11 LIFE INSURANCE balances. Kevin's personal balance sheet, including death benefits from life insurance and his pension plan, is as follows: total assets to arrive at the amount of liquid assets that can produce income for the family Determine the Amount of Additional Capital Needed The final step is to determine the amount of additional capital needed. This step involves a comparison of the income objective with other sources of income, such as Social Security survivor benefits. In Kevin's case, his family would have an income shortage of $24,250 annually based on his present financial situation. Assuming the liquid assets and life insurance proceeds can be invested to earn at least 5 percent annually, Kevin needs an addi tional $485,000 of life insurance to meet his financial goals. This calculation is summarized as follows sS House Automobiles Personal and household property Securities and investments $225,000 20,000 40,000 60,000 king account dual and group life insurance 200,000 70,000 IVi Liabilities $100,000 Mortgage Auto loan Credit cards Income objective for family Income from capital now available ($55,000 x 5%) Social Security survivor benefits $115,000 -2750 13,000 Determine the Amount of Income-Producing Capital The second step is to determine the amount of income-producing assets. This step is performed by subtracting the liabilities, cash needs, and non- income-producing capital from total assets. Kevin rta Total new capital required ($24,250/.05) $485,000 has $55,000 of capital that can produce income for The capital retention approach has the advan tages of simplicity, ease of understanding, and preser- vation of capital. In addition, investment income earned on the emergency and educational funds can be used as a partial hedge against inflation, or it can be accumulated to offset rising educational costs. The major disadvantage, however, is that a larger amount of life insurance is required to produce a given amount of income. The family, however, may be unable to afford the additional amount of life the family. This amount is determined as follows Total assets $620,000 Less: $100,000 Mortgage payoff Auto loan and credit Final expenses Emergency fund Educational fund Non-income-producing 15,000 50,000 100,000 insurance. capital (automobiles, Interactive Calculators on the Internet rsonal and household pe property, value of home) 285,000 565,000 $55,000 Many life insurers and premium quoting services have interactive calculators on their Web sites that calcu late the amount of life insurance needed. You make assumptions about inflation, rates of return on the In the preceding illustration, the home is not an death proceeds, amount of income needed by the fam- income-producing asset. Unless the home is sold orily, and certain other assumptions. However, the qual- rented, it ordinarily does not produce cash income for ity of the interactive calculators varies widely. Some the family. Thus, the home is considered to be part of calculators are extremely limited, and questions con- non-income-producing capital that is subtracted from cerning the amount of accumulated assets and other Total deductions Capital now available for income 218 CHAPTER 11 LIFE INSURANCE balances. Kevin's personal balance sheet, including death benefits from life insurance and his pension plan, is as follows: total assets to arrive at the amount of liquid assets that can produce income for the family Determine the Amount of Additional Capital Needed The final step is to determine the amount of additional capital needed. This step involves a comparison of the income objective with other sources of income, such as Social Security survivor benefits. In Kevin's case, his family would have an income shortage of $24,250 annually based on his present financial situation. Assuming the liquid assets and life insurance proceeds can be invested to earn at least 5 percent annually, Kevin needs an addi tional $485,000 of life insurance to meet his financial goals. This calculation is summarized as follows sS House Automobiles Personal and household property Securities and investments $225,000 20,000 40,000 60,000 king account dual and group life insurance 200,000 70,000 IVi Liabilities $100,000 Mortgage Auto loan Credit cards Income objective for family Income from capital now available ($55,000 x 5%) Social Security survivor benefits $115,000 -2750 13,000 Determine the Amount of Income-Producing Capital The second step is to determine the amount of income-producing assets. This step is performed by subtracting the liabilities, cash needs, and non- income-producing capital from total assets. Kevin rta Total new capital required ($24,250/.05) $485,000 has $55,000 of capital that can produce income for The capital retention approach has the advan tages of simplicity, ease of understanding, and preser- vation of capital. In addition, investment income earned on the emergency and educational funds can be used as a partial hedge against inflation, or it can be accumulated to offset rising educational costs. The major disadvantage, however, is that a larger amount of life insurance is required to produce a given amount of income. The family, however, may be unable to afford the additional amount of life the family. This amount is determined as follows Total assets $620,000 Less: $100,000 Mortgage payoff Auto loan and credit Final expenses Emergency fund Educational fund Non-income-producing 15,000 50,000 100,000 insurance. capital (automobiles, Interactive Calculators on the Internet rsonal and household pe property, value of home) 285,000 565,000 $55,000 Many life insurers and premium quoting services have interactive calculators on their Web sites that calcu late the amount of life insurance needed. You make assumptions about inflation, rates of return on the In the preceding illustration, the home is not an death proceeds, amount of income needed by the fam- income-producing asset. Unless the home is sold orily, and certain other assumptions. However, the qual- rented, it ordinarily does not produce cash income for ity of the interactive calculators varies widely. Some the family. Thus, the home is considered to be part of calculators are extremely limited, and questions con- non-income-producing capital that is subtracted from cerning the amount of accumulated assets and other Total deductions Capital now available for income