Answered step by step

Verified Expert Solution

Question

1 Approved Answer

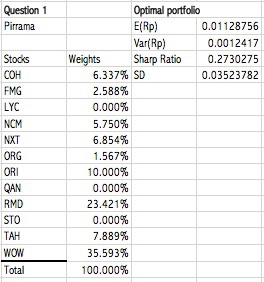

Question 1 Pirrama Stocks COH FMG LYC NCM NXT ORG ORI QAN RMD STO TAH WOW Total Optimal portfolio E(Rp) 0.01128756 Var(Rp) 0.0012417 Weights Sharp

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis for Financial Management

Authors: Robert C. Higgins

10th edition

007803468X, 978-0078034688