Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Question #1 please need to show work and also it could be hand written or Microsoft Word. Thanks. You are Cindy, completing the analysis and

Question #1 please need to show work and also it could be hand written or Microsoft Word. Thanks.

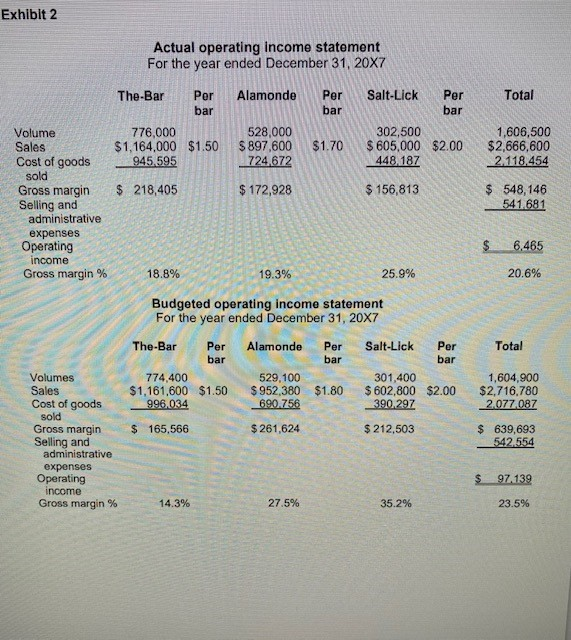

You are Cindy, completing the analysis and developing a final report to Alan, president of BBCC. The report should analyze BBCC's current cost allocations and give advice for the future. It should be formatted as a memo and include the following: 1. Revised 20X7 income statement (7 marks) a) Manufacturing overhead allocation (2 marks) BBCC has adopted a normal costing approach with manufacturing overhead costs allocated based on direct labour hours. However, the actual cost of product manufactured report in Exhibit 3 in the Project Details document appears to have included an allocation of actual manufacturing overhead based on a percentage of sales. Revise this report so the normal costing approach adopted by the company is properly reflected. b) Income statement results (5 marks) Prepare a revised 20X7 actual income statement (Exhibit 2) using the cost of goods manufactured in part (a) and adjusting for over- or underapplied overhead. It is the company's policy to write off any total over- or underapplied overhead to the total cost of goods sold rather than individual products during the period in which it is incurred. Comment on the change in gross margin overall, and for each product individually, as a result of the changes applied. The finished product beginning and ending inventory for all three products is as follows: The-Bar Alamonde Salt-Lick Beginning inventory $17,561 $10,702 $0 Ending inventory 18,292 10,497 2. Overview of 20X7 results (6 marks) Prepare an overview of the 20x7 results. Discuss any significant differences between the 20x7 budget and the actual figures (Exhibits 2 to 4). Base the analysis on the revised figures from requirement 1. Your analysis should include a discussion of the following: difference between actual and budgeted sales quantities for each product changes in unit selling price and effect on sales . . PROJECT DETAILS Since the first candy bar was made in Great Britain by Joseph Fry in 1847, companies have continued to perfect the quality of this decadent treat. The Boston Bar Chocolate Company (BBCC) is no exception. BBCC began operations 10 years ago by two brothers, Alan and Calvin, who had a passion for chocolate and a vision for creating a treat that was both tasty and healthy. is vision. The company's slogan is "Raising THE-BAR on health," and for good reason. Customers keep coming back for more, not only because of The-Bar's great taste, but also because of the growing number of health reports stating that the flavanols in chocolate help to reduce blood pressure and increase memory retention. BBCC roasts its own cocoa beans to ensure maximum flavanol content. This gives BBCC a competitive advantage in the premium-quality chocolate market. The two brothers continue to own a majority of the shares and are actively involved in the company - Alan as president and Calvin as marketing manager. Divisions and processes BBCC's processing plant consists of two divisions: the cocoa bean division and the chocolate bar division. The cocoa bean division purchases the raw cocoa beans and ferments and roasts them. The products and byproducts that cannot be used in the chocolate bar division are packaged and sold to customers for a variety of other final products. The chocolate bar division produces the wrapped chocolate bars that are sold to retailers. All products follow the same mixing procedure and some products have an additional step of adding particulates such as almonds or salt granules. The mixture is then poured into moulds, cooled, separated into bars, and wrapped. While most of the resources in the two divisions are separate, the divisions operate on the same premises. Chocolate bar division The chocolate bar division currently produces 1.6 million chocolate bars per year. This represents around 80% of its practical capacity. Practical capacity is 12,000 direct labour hours or about 2 million bars per year. In addition to The-Bar, the chocolate bar division also produces a version of The-Bar with almonds called Alamonde and another with pieces of pink Himalayan salt called Salt-Lick. Most national grocery chains carry The-Bar and Alamonde. In addition, health-food stores carry Salt-Lick as a health booster because the Himalayan pink salt is said to detoxify the body by balancing pH. Because Salt-Lick is fairly new, it is produced as a special order and no inventory is kept on hand. It takes about the same amount of effort and resources to produce The-Bar as it does to produce Alamonde. As such, a process costing system is used. The batches are processed in a similar manner and receive the same amount of direct labour costs, basic ingredients, and manufacturing overhead costs. Therefore, these costs are averaged over all batches. The production process involves several operations in which conversion costs and ingredients are added to manufacture the product. Ingredients are added at the beginning of each operation. Direct labour costs and overhead are added evenly throughout the process based on direct labour hours. While the Salt-Lick bar is also processed in batches, it is special ordered, and production runs are scheduled based on demand. As a result, costs are assigned to a distinct batch using a job costing system. Current situation Alan has not been complacent about the success of the company. He continually monitors progress and scrutinizes costs. While candy bar consumption has fallen, the overall consumption of chocolate per capita in the market is stable, and the company has been able to maintain its market share due to continued consumer demand for healthy chocolate products. However, Alan would like to ensure that the company is adequately controlling costs and reducing risk. As such, he would also like to make some pricing predictions on his products. Recently, Alan engaged Cindy, CPA, to review the latest operating statements. He anticipates that Cindy will be able to provide some insight into how to be proactive in addressing some of the issues. The following exhibits provide more details on these issues along with details about the budgeted and actual financial position of the company. This information will be used to complete the requirements of Project 1 and Project 2 Note: To reduce complexity in the case study, process costing is used. A batch system like candy bar production would normally use an operational costing system, which is a hybrid of process and job costing In order to properly analyze the financial statements, the following information is also provided: Exhibit 3 Actual cost of product manufactured For the year ended December 31, 20X7 Direct ingredients used Direct labour Manufacturing overhead Total manufacturing costs Add: beginning work-in-process Deduct: ending work-in-process Cost of goods manufactured The-Bar Alamonde $ 333,507 $ 232,724 135,876 123,926 476.954 367.795 $ 946,337 $ 724,445 1,196 837 (1.207) (815) $ 946.326 $724,467 Salt-Lick Total $ 129,948 $ 696,179 70,338 330,140 247 901 1,092.650 $ 448,187 $ 2,118,969 2,033 (2.022) $448.187 $ 2.118.980 Budgeted cost of product manufactured For the year ended December 31, 20X7 Direct ingredients used Direct labour Manufacturing overhead Total manufacturing costs Add: beginning work-in-process Deduct: ending work-in-process Cost of good manufactured The-Bar $ 330,271 147,744 518,685 $ 996,700 2,991 (2.885) 996.806 Alamonde $ 231,514 101,736 357 165 $ 690,415 2,094 (1.949) $ 690,560 Salt-Lick $ 128,694 57.996 203,607 $ 390,297 Total $ 690,479 307,476 1,079,457 $ 2,077,412 5,085 (4.834) $ 2,077.663 $ 390 297 Exhibit 2 Actual operating income statement For the year ended December 31, 20X7 The-Bar Per bar Alamonde Per bar Salt-Lick Total Per bar 776,000 $1,164,000 $1.50 945,595 528,000 $ 897,600 724,672 $1.70 302,500 $ 605,000 $2.00 448,187 1,606,500 $2,666,600 2.118,454 $ 218,405 $ 172,928 $ 156,813 Volume Sales Cost of goods sold Gross margin Selling and administrative expenses Operating income Gross margin % $ 548,146 541681 $ 6,465 18.8% 19.3% 25.9% 20.6% Total Budgeted operating income statement For the year ended December 31, 20X7 The-Bar Per Alamonde Per Salt-Lick Per bar bar bar 774,400 529,100 301,400 $1,161,600 $1.50 $ 952,380 $1.80 $ 602,800 $2.00 996.034 690.756 390.297 1,604,900 $2,716,780 2077087 $ 165,566 $ 261,624 $ 212,503 Volumes Sales Cost of goods sold Gross margin Selling and administrative expenses Operating income Gross margin % $ 639,693 542 554 $ 97.139 14.3% 27.5% 35.2% 23.5% You are Cindy, completing the analysis and developing a final report to Alan, president of BBCC. The report should analyze BBCC's current cost allocations and give advice for the future. It should be formatted as a memo and include the following: 1. Revised 20X7 income statement (7 marks) a) Manufacturing overhead allocation (2 marks) BBCC has adopted a normal costing approach with manufacturing overhead costs allocated based on direct labour hours. However, the actual cost of product manufactured report in Exhibit 3 in the Project Details document appears to have included an allocation of actual manufacturing overhead based on a percentage of sales. Revise this report so the normal costing approach adopted by the company is properly reflected. b) Income statement results (5 marks) Prepare a revised 20X7 actual income statement (Exhibit 2) using the cost of goods manufactured in part (a) and adjusting for over- or underapplied overhead. It is the company's policy to write off any total over- or underapplied overhead to the total cost of goods sold rather than individual products during the period in which it is incurred. Comment on the change in gross margin overall, and for each product individually, as a result of the changes applied. The finished product beginning and ending inventory for all three products is as follows: The-Bar Alamonde Salt-Lick Beginning inventory $17,561 $10,702 $0 Ending inventory 18,292 10,497 2. Overview of 20X7 results (6 marks) Prepare an overview of the 20x7 results. Discuss any significant differences between the 20x7 budget and the actual figures (Exhibits 2 to 4). Base the analysis on the revised figures from requirement 1. Your analysis should include a discussion of the following: difference between actual and budgeted sales quantities for each product changes in unit selling price and effect on sales . . PROJECT DETAILS Since the first candy bar was made in Great Britain by Joseph Fry in 1847, companies have continued to perfect the quality of this decadent treat. The Boston Bar Chocolate Company (BBCC) is no exception. BBCC began operations 10 years ago by two brothers, Alan and Calvin, who had a passion for chocolate and a vision for creating a treat that was both tasty and healthy. is vision. The company's slogan is "Raising THE-BAR on health," and for good reason. Customers keep coming back for more, not only because of The-Bar's great taste, but also because of the growing number of health reports stating that the flavanols in chocolate help to reduce blood pressure and increase memory retention. BBCC roasts its own cocoa beans to ensure maximum flavanol content. This gives BBCC a competitive advantage in the premium-quality chocolate market. The two brothers continue to own a majority of the shares and are actively involved in the company - Alan as president and Calvin as marketing manager. Divisions and processes BBCC's processing plant consists of two divisions: the cocoa bean division and the chocolate bar division. The cocoa bean division purchases the raw cocoa beans and ferments and roasts them. The products and byproducts that cannot be used in the chocolate bar division are packaged and sold to customers for a variety of other final products. The chocolate bar division produces the wrapped chocolate bars that are sold to retailers. All products follow the same mixing procedure and some products have an additional step of adding particulates such as almonds or salt granules. The mixture is then poured into moulds, cooled, separated into bars, and wrapped. While most of the resources in the two divisions are separate, the divisions operate on the same premises. Chocolate bar division The chocolate bar division currently produces 1.6 million chocolate bars per year. This represents around 80% of its practical capacity. Practical capacity is 12,000 direct labour hours or about 2 million bars per year. In addition to The-Bar, the chocolate bar division also produces a version of The-Bar with almonds called Alamonde and another with pieces of pink Himalayan salt called Salt-Lick. Most national grocery chains carry The-Bar and Alamonde. In addition, health-food stores carry Salt-Lick as a health booster because the Himalayan pink salt is said to detoxify the body by balancing pH. Because Salt-Lick is fairly new, it is produced as a special order and no inventory is kept on hand. It takes about the same amount of effort and resources to produce The-Bar as it does to produce Alamonde. As such, a process costing system is used. The batches are processed in a similar manner and receive the same amount of direct labour costs, basic ingredients, and manufacturing overhead costs. Therefore, these costs are averaged over all batches. The production process involves several operations in which conversion costs and ingredients are added to manufacture the product. Ingredients are added at the beginning of each operation. Direct labour costs and overhead are added evenly throughout the process based on direct labour hours. While the Salt-Lick bar is also processed in batches, it is special ordered, and production runs are scheduled based on demand. As a result, costs are assigned to a distinct batch using a job costing system. Current situation Alan has not been complacent about the success of the company. He continually monitors progress and scrutinizes costs. While candy bar consumption has fallen, the overall consumption of chocolate per capita in the market is stable, and the company has been able to maintain its market share due to continued consumer demand for healthy chocolate products. However, Alan would like to ensure that the company is adequately controlling costs and reducing risk. As such, he would also like to make some pricing predictions on his products. Recently, Alan engaged Cindy, CPA, to review the latest operating statements. He anticipates that Cindy will be able to provide some insight into how to be proactive in addressing some of the issues. The following exhibits provide more details on these issues along with details about the budgeted and actual financial position of the company. This information will be used to complete the requirements of Project 1 and Project 2 Note: To reduce complexity in the case study, process costing is used. A batch system like candy bar production would normally use an operational costing system, which is a hybrid of process and job costing In order to properly analyze the financial statements, the following information is also provided: Exhibit 3 Actual cost of product manufactured For the year ended December 31, 20X7 Direct ingredients used Direct labour Manufacturing overhead Total manufacturing costs Add: beginning work-in-process Deduct: ending work-in-process Cost of goods manufactured The-Bar Alamonde $ 333,507 $ 232,724 135,876 123,926 476.954 367.795 $ 946,337 $ 724,445 1,196 837 (1.207) (815) $ 946.326 $724,467 Salt-Lick Total $ 129,948 $ 696,179 70,338 330,140 247 901 1,092.650 $ 448,187 $ 2,118,969 2,033 (2.022) $448.187 $ 2.118.980 Budgeted cost of product manufactured For the year ended December 31, 20X7 Direct ingredients used Direct labour Manufacturing overhead Total manufacturing costs Add: beginning work-in-process Deduct: ending work-in-process Cost of good manufactured The-Bar $ 330,271 147,744 518,685 $ 996,700 2,991 (2.885) 996.806 Alamonde $ 231,514 101,736 357 165 $ 690,415 2,094 (1.949) $ 690,560 Salt-Lick $ 128,694 57.996 203,607 $ 390,297 Total $ 690,479 307,476 1,079,457 $ 2,077,412 5,085 (4.834) $ 2,077.663 $ 390 297 Exhibit 2 Actual operating income statement For the year ended December 31, 20X7 The-Bar Per bar Alamonde Per bar Salt-Lick Total Per bar 776,000 $1,164,000 $1.50 945,595 528,000 $ 897,600 724,672 $1.70 302,500 $ 605,000 $2.00 448,187 1,606,500 $2,666,600 2.118,454 $ 218,405 $ 172,928 $ 156,813 Volume Sales Cost of goods sold Gross margin Selling and administrative expenses Operating income Gross margin % $ 548,146 541681 $ 6,465 18.8% 19.3% 25.9% 20.6% Total Budgeted operating income statement For the year ended December 31, 20X7 The-Bar Per Alamonde Per Salt-Lick Per bar bar bar 774,400 529,100 301,400 $1,161,600 $1.50 $ 952,380 $1.80 $ 602,800 $2.00 996.034 690.756 390.297 1,604,900 $2,716,780 2077087 $ 165,566 $ 261,624 $ 212,503 Volumes Sales Cost of goods sold Gross margin Selling and administrative expenses Operating income Gross margin % $ 639,693 542 554 $ 97.139 14.3% 27.5% 35.2% 23.5%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management And Cost Accounting

Authors: Mike Tayles, Colin Drury

11th Edition

147377361X, 978-1473773615