Answered step by step

Verified Expert Solution

Question

1 Approved Answer

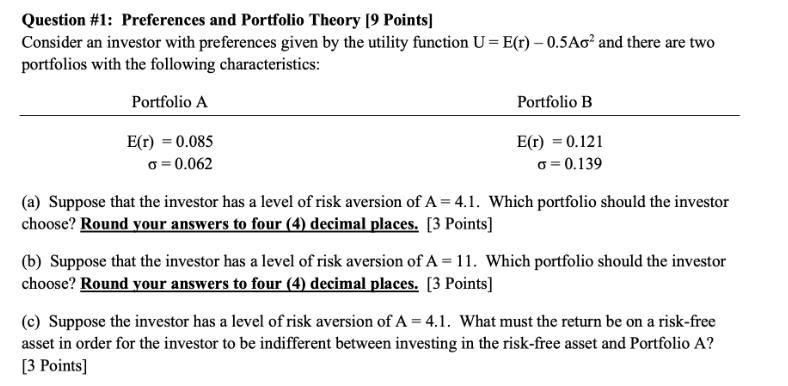

Question #1: Preferences and Portfolio Theory [9 Points] Consider an investor with preferences given by the utility function U = E(r) - 0.5Ao and

Question #1: Preferences and Portfolio Theory [9 Points] Consider an investor with preferences given by the utility function U = E(r) - 0.5Ao and there are two portfolios with the following characteristics: Portfolio A E(r) = 0.085 o = 0.062 Portfolio B E(r) = 0.121 o = 0.139 (a) Suppose that the investor has a level of risk aversion of A=4.1. Which portfolio should the investor choose? Round your answers to four (4) decimal places. [3 Points] (b) Suppose that the investor has a level of risk aversion of A=11. Which portfolio should the investor choose? Round your answers to four (4) decimal places. [3 Points] (c) Suppose the investor has a level of risk aversion of A=4.1. What must the return be on a risk-free asset in order for the investor to be indifferent between investing in the risk-free asset and Portfolio A? [3 Points]

Step by Step Solution

★★★★★

3.37 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

ANSWER a To determine which portfolio the investor should choose we can compare the utility values f...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microeconomics An Intuitive Approach with Calculus

Authors: Thomas Nechyba

1st edition

538453257, 978-0538453257