Question 1:

Question 2:

Question 3

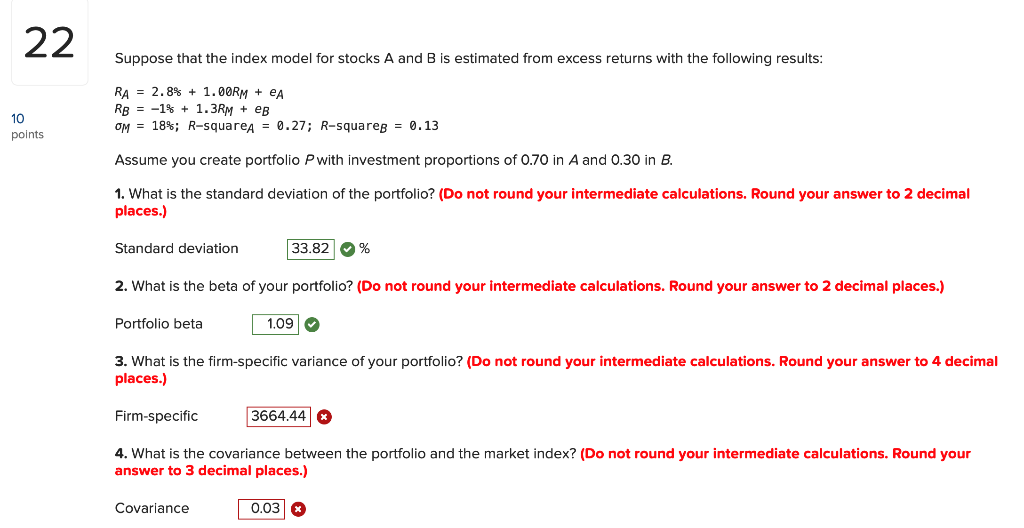

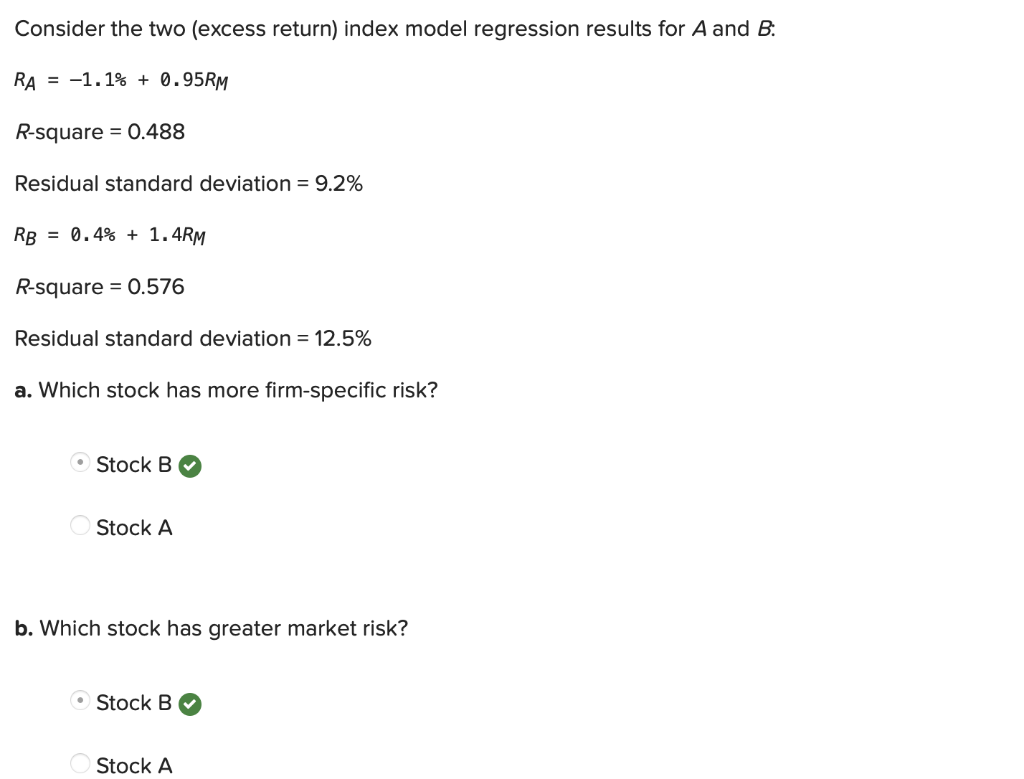

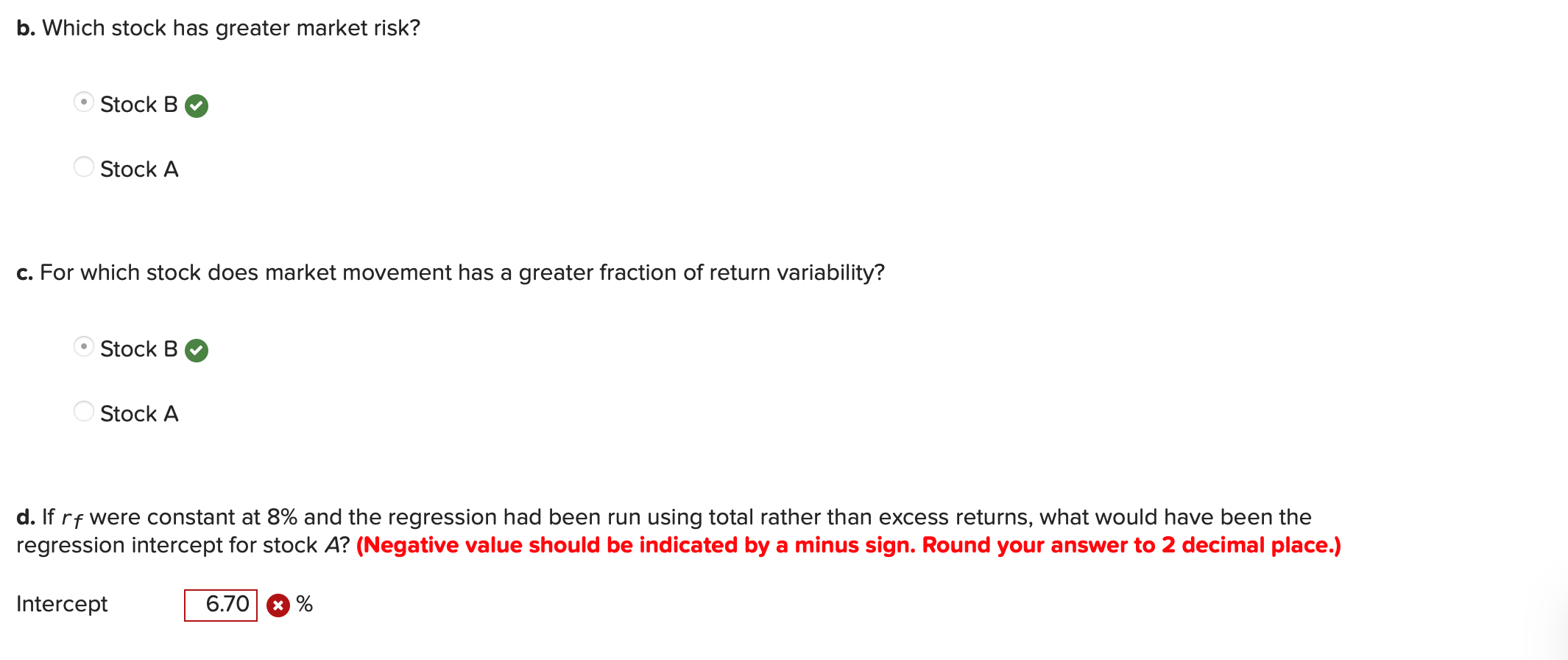

22 10 points Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA 2.8% +1.00RM + A RB 1% + 1.3RM + eB OM = 18%; R-square = 0.27; R-squareg = 0.13 Assume you create portfolio P with investment proportions of 0.70 in A and 0.30 in B. 1. What is the standard deviation of the portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.) Standard deviation 33.82 % 2. What is the beta of your portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.) Portfolio beta 1.09 3. What is the firm-specific variance of your portfolio? (Do not round your intermediate calculations. Round your answer to 4 decimal places.) Firm-specific 3664.44 x 4. What is the covariance between the portfolio and the market index? (Do not round your intermediate calculations. Round your answer to 3 decimal places.) Covariance 0.03 x Consider the two (excess return) index model regression results for A and B: RA= -1.1% + 0.95RM R-square= 0.488 Residual standard deviation = 9.2% RB = 0.4% + 1.4RM R-square = 0.576 Residual standard deviation = 12.5% a. Which stock has more firm-specific risk? Stock B Stock A b. Which stock has greater market risk? Stock B Stock A b. Which stock has greater market risk? Stock B Stock A c. For which stock does market movement has a greater fraction of return variability? Stock B Stock A d. If rf were constant at 8% and the regression had been run using total rather than excess returns, what would have been the regression intercept for stock A? (Negative value should be indicated by a minus sign. Round your answer to 2 decimal place.) Intercept 6.70 * % Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA= 4.0%+0.50RM + eA RB 1.2 % + 0.70RM + eB OM 17%; R-square = 0.26; R-squareg = 0.18 Assume you create a portfolio Q, with investment proportions of 0.40 in a risky portfolio P, 0.35 in the market index, and 0.25 in T-bill. Portfolio P is composed of 70% Stock A and 30% Stock B. 1. What is the standard deviation of portfolio Q? (Calculate using numbers in decimal form, not percentages. Do not round intermediate calculations. Round your answer to 2 decimal places.) Standard deviation 0.17% 2. What is the beta of portfolio Q? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Portfolio beta 3. What is the "firm-specific" risk of portfolio Q? (Calculate using numbers in decimal form, not percentages. Do not round intermediate calculations. Round your answer to 4 decimal places.) Firm-specific 0.0101 4. What is the covariance between the portfolio and the market index? (Calculate using numbers in decimal form, not percentages. Do not round intermediate calculations. Round your answer to 2 decimal places.) Covariance 0.22 x 22 10 points Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA 2.8% +1.00RM + A RB 1% + 1.3RM + eB OM = 18%; R-square = 0.27; R-squareg = 0.13 Assume you create portfolio P with investment proportions of 0.70 in A and 0.30 in B. 1. What is the standard deviation of the portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.) Standard deviation 33.82 % 2. What is the beta of your portfolio? (Do not round your intermediate calculations. Round your answer to 2 decimal places.) Portfolio beta 1.09 3. What is the firm-specific variance of your portfolio? (Do not round your intermediate calculations. Round your answer to 4 decimal places.) Firm-specific 3664.44 x 4. What is the covariance between the portfolio and the market index? (Do not round your intermediate calculations. Round your answer to 3 decimal places.) Covariance 0.03 x Consider the two (excess return) index model regression results for A and B: RA= -1.1% + 0.95RM R-square= 0.488 Residual standard deviation = 9.2% RB = 0.4% + 1.4RM R-square = 0.576 Residual standard deviation = 12.5% a. Which stock has more firm-specific risk? Stock B Stock A b. Which stock has greater market risk? Stock B Stock A b. Which stock has greater market risk? Stock B Stock A c. For which stock does market movement has a greater fraction of return variability? Stock B Stock A d. If rf were constant at 8% and the regression had been run using total rather than excess returns, what would have been the regression intercept for stock A? (Negative value should be indicated by a minus sign. Round your answer to 2 decimal place.) Intercept 6.70 * % Suppose that the index model for stocks A and B is estimated from excess returns with the following results: RA= 4.0%+0.50RM + eA RB 1.2 % + 0.70RM + eB OM 17%; R-square = 0.26; R-squareg = 0.18 Assume you create a portfolio Q, with investment proportions of 0.40 in a risky portfolio P, 0.35 in the market index, and 0.25 in T-bill. Portfolio P is composed of 70% Stock A and 30% Stock B. 1. What is the standard deviation of portfolio Q? (Calculate using numbers in decimal form, not percentages. Do not round intermediate calculations. Round your answer to 2 decimal places.) Standard deviation 0.17% 2. What is the beta of portfolio Q? (Do not round intermediate calculations. Round your answer to 2 decimal places.) Portfolio beta 3. What is the "firm-specific" risk of portfolio Q? (Calculate using numbers in decimal form, not percentages. Do not round intermediate calculations. Round your answer to 4 decimal places.) Firm-specific 0.0101 4. What is the covariance between the portfolio and the market index? (Calculate using numbers in decimal form, not percentages. Do not round intermediate calculations. Round your answer to 2 decimal places.) Covariance 0.22 x