Question

question 1 show all calculations for part marks a) prepare the statement of comprehensive income of Bakone ltd for the year ended 30 june 2018

question 1 show all calculations for part marks a) prepare the statement of comprehensive income of Bakone ltd for the year ended 30 june 2018 in accordance with IFRS (27marks) b) prepare the statement of changes in equity of Bakome ltd for the year ended 30 june 2018 in accordance with IFRS(15 marks)

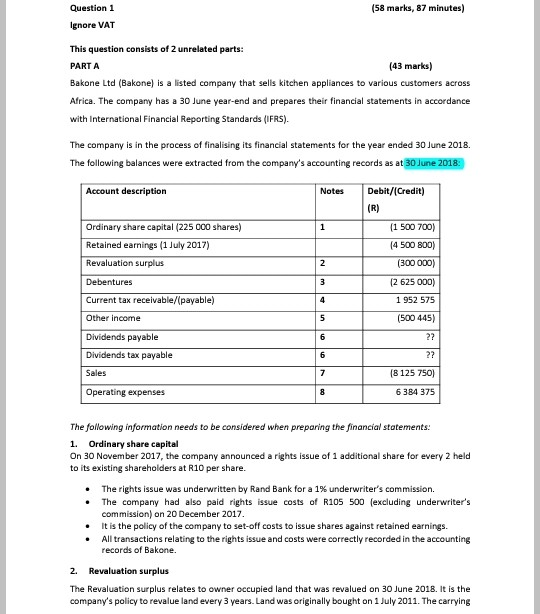

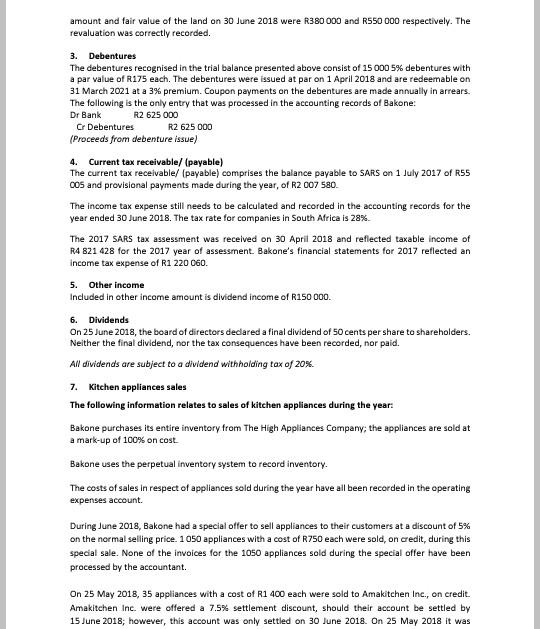

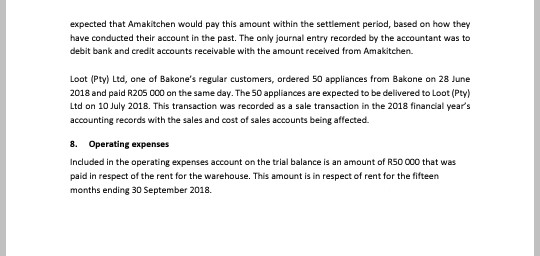

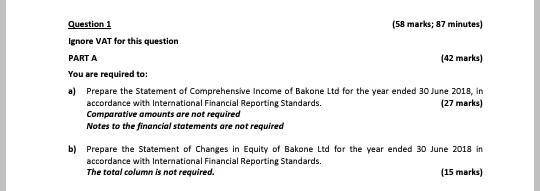

(58 marks, 87 minutes) Question 1 Ignore VAT This question consists of 2 unrelated parts: PARTA (43 marks) Bakone Ltd (Bakone) is a listed company that sells kitchen appliances to various customers across Africa. The company has a 30 June year-end and prepares their financial statements in accordance with International Financial Reporting Standards (IFRS). The company is in the process of finalising its financial statements for the year ended 30 June 2018. The following balances were extracted from the company's accounting records as at 30 June 2018: Account description Notes Debit/Credit) (R) 1 (1 500 700) (4 500 800) 2 Ordinary share capital (225 000 shares) Retained earnings (1 July 2017) Revaluation surplus Debentures Current tax receivable/(payable) Other income 3 4 (300 000) (2 625 000) 1 952 575 (500 445) ?? ?? 5 Dividends payable 6 6 Dividends tax payable Sales 7 (8 125 750) 6 384 375 Operating expenses 8 The following information needs to be considered when preparing the financial statements: 1. Ordinary share capital On 30 November 2017, the company announced a rights issue of 1 additional share for every 2 held to its existing shareholders at R10 per share. The rights issue was underwritten by Rand Bank for a 1% underwriter's commission. The company had also paid rights issue costs of R10S 500 (excluding underwriter's commission) on 20 December 2017. It is the policy of the company to set-off costs to issue shares against retained earnings. . All transactions relating to the rights issue and costs were correctly recorded in the accounting records of Bakone. 2. Revaluation surplus The Revaluation surplus relates to owner occupied land that was revalued on 30 June 2018. It is the company's policy to revalue land every 3 years. Land was originally bought on 1 July 2011. The carrying amount and fair value of the land on 30 June 2018 were R380 000 and R550 000 respectively. The revaluation was correctly recorded. 3. Debentures The debentures recognised in the trial balance presented above consist of 15 000 5% debentures with a par value of R175 each. The debentures were issued at par on 1 April 2018 and are redeemable on 31 March 2021 at a 3% premium. Coupon payments on the debentures are made annually in arrears. The following is the only entry that was processed in the accounting records of Bakone: Dr Bank R2 625 000 Cr Debentures R2 625 000 (Proceeds from debenture issue) 4. Current tax receivable/ (payable) The current tax receivable/ (payable) comprises the balance payable to SARS on 1 July 2017 of R55 cos and provisional payments made during the year, of R2 007 580. The income tax expense still needs to be calculated and recorded in the accounting records for the year ended 30 June 2018. The tax rate for companies in South Africa is 28%. The 2017 SARS tax assessment was received on 30 April 2018 and reflected taxable income of R4 821 428 for the 2017 year of assessment. Bakone's financial statements for 2017 reflected an income tax expense of R1 220 060 5. Other income Included in other income amount is dividend income of R150 000 6. Dividends On 25 June 2018, the board of directors declared a final dividend of 50 cents per share to shareholders. Neither the final dividend, nor the tax consequences have been recorded, nor paid. All dividends are subject to a dividend withholding tax of 20%. 7. Kitchen appliances sales The following information relates to sales of kitchen appliances during the year: Bakone purchases its entire inventory from The High Appliances Company; the appliances are sold at a mark-up of 100% on cost. Bakone uses the perpetual inventory system to record inventory. The costs of sales in respect of appliances sold during the year have all been recorded in the operating expenses account During June 2018, Bakone had a special offer to sell appliances to their customers at a discount of 5% on the normal selling price. 1050 appliances with a cost of R750 each were sold, on credit, during this special sale. None of the invoices for the 100 appliances sold during the special offer have been processed by the accountant. On 25 May 2018, 35 appliances with a cost of R1 400 each were sold to Amakitchen Inc., credit. Amakitchen Inc. were offered a 7.5% settlement discount, should their account be settled by 15 June 2018; however, this account was only settled on 30 June 2018. On 25 May 2018 it was expected that Amakitchen would pay this amount within the settlement period, based on how they have conducted their account in the past. The only journal entry recorded by the accountant was to debit bank and credit accounts receivable with the amount received from Amakitchen. Loot (Pty) Ltd, one of Bakone's regular customers, ordered 50 appliances from Bakone on 28 June 2018 and paid R20 000 on the same day. The 50 appliances are expected to be delivered to Loot (Pty) Ltd on 10 July 2018. This transaction was recorded as a sale transaction in the 2018 financial year's accounting records with the sales and cost of sales accounts being affected. 8. Operating expenses Included in the operating expenses account on the trial balance is an amount of R50 000 that was paid in respect of the rent for the warehouse. This amount is in respect of rent for the fifteen months ending 30 September 2018. Question 1 (58 marks; 87 minutes) Ignore VAT for this question PARTA (42 marks) You are required to: a) Prepare the Statement of Comprehensive Income of Bakone Ltd for the year ended 30 June 2018, in accordance with International Financial Reporting Standards. (27 marks) Comparative amounts are not required Notes to the financial statements are not required b) Prepare the Statement of Changes in Equity of Bakone Ltd for the year ended 30 June 2018 in accordance with International Financial Reporting Standards. The total column is not required. (15 marks) (58 marks, 87 minutes) Question 1 Ignore VAT This question consists of 2 unrelated parts: PARTA (43 marks) Bakone Ltd (Bakone) is a listed company that sells kitchen appliances to various customers across Africa. The company has a 30 June year-end and prepares their financial statements in accordance with International Financial Reporting Standards (IFRS). The company is in the process of finalising its financial statements for the year ended 30 June 2018. The following balances were extracted from the company's accounting records as at 30 June 2018: Account description Notes Debit/Credit) (R) 1 (1 500 700) (4 500 800) 2 Ordinary share capital (225 000 shares) Retained earnings (1 July 2017) Revaluation surplus Debentures Current tax receivable/(payable) Other income 3 4 (300 000) (2 625 000) 1 952 575 (500 445) ?? ?? 5 Dividends payable 6 6 Dividends tax payable Sales 7 (8 125 750) 6 384 375 Operating expenses 8 The following information needs to be considered when preparing the financial statements: 1. Ordinary share capital On 30 November 2017, the company announced a rights issue of 1 additional share for every 2 held to its existing shareholders at R10 per share. The rights issue was underwritten by Rand Bank for a 1% underwriter's commission. The company had also paid rights issue costs of R10S 500 (excluding underwriter's commission) on 20 December 2017. It is the policy of the company to set-off costs to issue shares against retained earnings. . All transactions relating to the rights issue and costs were correctly recorded in the accounting records of Bakone. 2. Revaluation surplus The Revaluation surplus relates to owner occupied land that was revalued on 30 June 2018. It is the company's policy to revalue land every 3 years. Land was originally bought on 1 July 2011. The carrying amount and fair value of the land on 30 June 2018 were R380 000 and R550 000 respectively. The revaluation was correctly recorded. 3. Debentures The debentures recognised in the trial balance presented above consist of 15 000 5% debentures with a par value of R175 each. The debentures were issued at par on 1 April 2018 and are redeemable on 31 March 2021 at a 3% premium. Coupon payments on the debentures are made annually in arrears. The following is the only entry that was processed in the accounting records of Bakone: Dr Bank R2 625 000 Cr Debentures R2 625 000 (Proceeds from debenture issue) 4. Current tax receivable/ (payable) The current tax receivable/ (payable) comprises the balance payable to SARS on 1 July 2017 of R55 cos and provisional payments made during the year, of R2 007 580. The income tax expense still needs to be calculated and recorded in the accounting records for the year ended 30 June 2018. The tax rate for companies in South Africa is 28%. The 2017 SARS tax assessment was received on 30 April 2018 and reflected taxable income of R4 821 428 for the 2017 year of assessment. Bakone's financial statements for 2017 reflected an income tax expense of R1 220 060 5. Other income Included in other income amount is dividend income of R150 000 6. Dividends On 25 June 2018, the board of directors declared a final dividend of 50 cents per share to shareholders. Neither the final dividend, nor the tax consequences have been recorded, nor paid. All dividends are subject to a dividend withholding tax of 20%. 7. Kitchen appliances sales The following information relates to sales of kitchen appliances during the year: Bakone purchases its entire inventory from The High Appliances Company; the appliances are sold at a mark-up of 100% on cost. Bakone uses the perpetual inventory system to record inventory. The costs of sales in respect of appliances sold during the year have all been recorded in the operating expenses account During June 2018, Bakone had a special offer to sell appliances to their customers at a discount of 5% on the normal selling price. 1050 appliances with a cost of R750 each were sold, on credit, during this special sale. None of the invoices for the 100 appliances sold during the special offer have been processed by the accountant. On 25 May 2018, 35 appliances with a cost of R1 400 each were sold to Amakitchen Inc., credit. Amakitchen Inc. were offered a 7.5% settlement discount, should their account be settled by 15 June 2018; however, this account was only settled on 30 June 2018. On 25 May 2018 it was expected that Amakitchen would pay this amount within the settlement period, based on how they have conducted their account in the past. The only journal entry recorded by the accountant was to debit bank and credit accounts receivable with the amount received from Amakitchen. Loot (Pty) Ltd, one of Bakone's regular customers, ordered 50 appliances from Bakone on 28 June 2018 and paid R20 000 on the same day. The 50 appliances are expected to be delivered to Loot (Pty) Ltd on 10 July 2018. This transaction was recorded as a sale transaction in the 2018 financial year's accounting records with the sales and cost of sales accounts being affected. 8. Operating expenses Included in the operating expenses account on the trial balance is an amount of R50 000 that was paid in respect of the rent for the warehouse. This amount is in respect of rent for the fifteen months ending 30 September 2018. Question 1 (58 marks; 87 minutes) Ignore VAT for this question PARTA (42 marks) You are required to: a) Prepare the Statement of Comprehensive Income of Bakone Ltd for the year ended 30 June 2018, in accordance with International Financial Reporting Standards. (27 marks) Comparative amounts are not required Notes to the financial statements are not required b) Prepare the Statement of Changes in Equity of Bakone Ltd for the year ended 30 June 2018 in accordance with International Financial Reporting Standards. The total column is not required. (15 marks)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modern Auditing

Authors: Graham Cosserat

1st Edition

0471810584, 9780471810582