QUESTION 1

This question uses the same information privided for assignment 4 question 1 part c : SO using this following information QUESTION 1 part c following:

QUESTION 1 part c - for assignment 4 ENDS.

ANSWER THIS QUESTION:

Required:

(a) Assume Parent Ltd only acquired 20% of the equity in Subsidiary Ltd for $124 000 on 1 April 2008.

Prepare the notional journal entry on 31 March 2023 to account for Parent Ltds investment in Subsidiary Ltd using the equity method as required by NZ IAS 28 Investments in Associates. The directors believe the investment asset has never been impaired. The tax rate is 28%. Complete a quick estimate in the space provided.

(b) Refer back to your answer for (a) and determine the dollar amount of the investment asset after being equity accounted for in the financial statements as of 31 March 2023. Show your workings

Use this to answer the above question: QUESTION 1

| (a) Notional journal entry on 31/03/23 Workings must be shown. | | |

| | $ | $ |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

Workings to be shown of the quick estimate:

| (b) The investment asset, after being equity accounted for, will be measured at: | $ |

| Workings: | |

QUESTION 2

Shuai Ltd completed their financial statements for the year ended 31 March 2023 and authorised them for issue on 12 June 2023. The new managing director, who started in May of 2023, is unsure about the treatment of the following material events that occurred in 2023 and has asked for your professional advice.

(i) 10 January 2023

On 10 January 2023, the directors declared a final dividend of $200 000 for the year

ended 31 March 2023. This final dividend was paid on 10 June 2023.

(ii) 5 April 2023

Initially measured at the cost of $900 600, slow-moving inventory was measured at a net

realisable value of $700 000 in the general ledger inventory account on 31 March 2023.

On 5 April 2023, this inventory sold for $820 000.

(iii) 24 April 2023

In December 2022, a customer initiated legal proceedings against Shuai Ltd concerning a breach of contract. On 31 March 2023, the companys legal advisers informed the directors that Shuai Ltd could be found liable for an estimated $600 000. Because of this advice, a provision was recognised in the financial statements. On 24 April 2023, the court found Shuai Ltd liable and was required to pay damages of $500 000.

Question 2 continued:

(iv) 2 May 2023 On 31 March 2023, a credit sale customer Desperate Ltd owed Shuai Ltd $250 000. Desperate Ltd's balance was considered doubtful at balance date. On 2 May 2023, Desperate Ltd went into bankruptcy.

(v) 15 May 2023

On 15 May 2023, Shuai Ltd noticed that its investment in Failing Ltd was listed on the stock exchange at $3.20 per share. On 31 March 2023, this investment of 80 000 shares in Failing Ltd had been measured at the fair value of $4.60 per share.

Required:

(a) Prepare a professional report (as taught in ACCTG 211) for the Shuai Ltd managing director to explain the treatment of the above five events according to NZ IAS 10 Events after the Reporting Period.

(b) The managing director emailed you specific questions about these five events, and you provided answers within your report. These specific questions are included in the Answer Booklet.

ANSWER USING THS FOLLOWING:

QUESTION 2

| Professional Report for Shuai Ltd |

| (i)10 January 2018 |

| Explain the treatment according to NZ IAS 10: |

| Specific question from the managing director: What was the effect of the declared dividend on the Statement of Financial Position as at 31 March 2023? |

| (ii) 5 April 2023 |

| Explain the treatment according to NZ IAS 10: |

| Specific question from the managing director: What was the effect on the general ledger accounts when this inventory was first remeasured from cost to NRV $700 000? |

Question 2 continued:

| (iii) 24 April 2023 |

| Explain the treatment according to NZ IAS 10: |

| Specific question from the managing director: What was the effect on the general ledger accounts after Shuai Ltd followed the legal advice and recognised a provision on 31 March 2023? |

| (iv) 2 May 2023 |

| Explain the treatment according to NZ IAS 10: |

| Specific question from the managing director: As of 31 March 2023, please determine the carrying amount of the individual account receivable Desperate Ltd, i.e., before Shuai Ltd found out about the bankruptcy. |

Question 2 continued:

| (v) 15 May 2023 |

| Explain the treatment according to NZ IAS 10: |

| Specific question from the managing director: What was the general ledger balance of the asset Investment in Failing Ltd when Shuai Ltd measured it at fair value on 31 March 2023? |

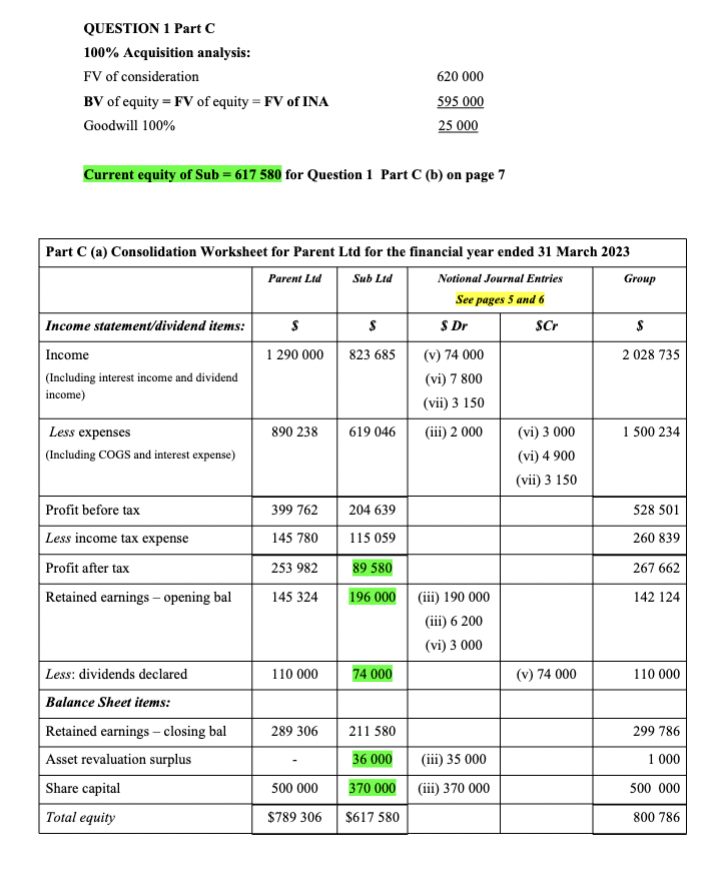

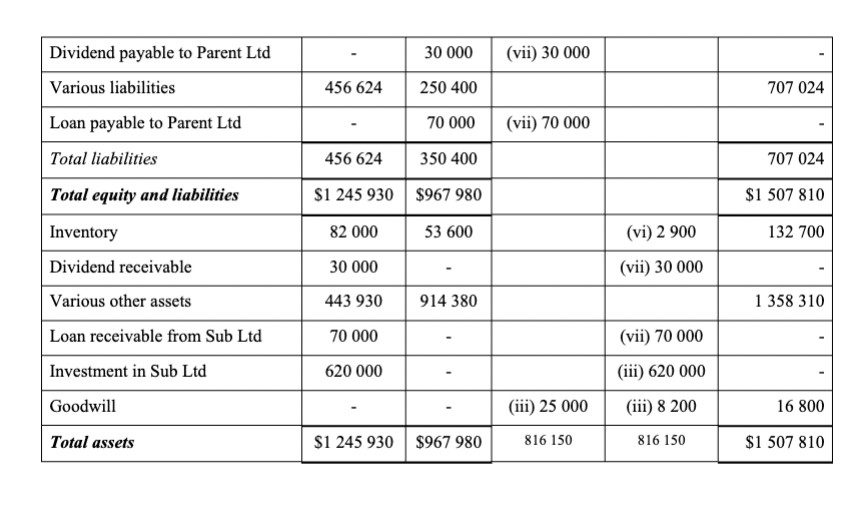

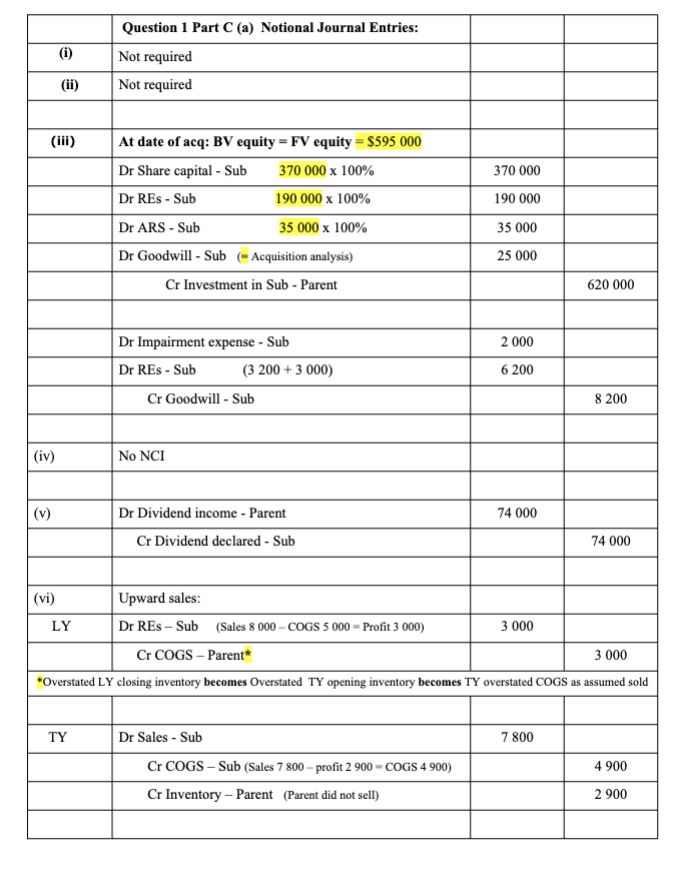

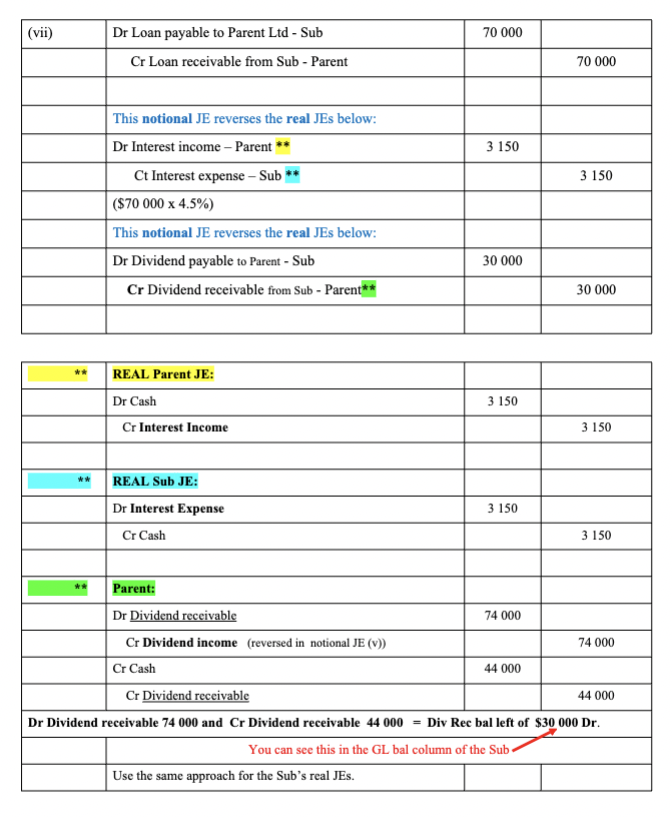

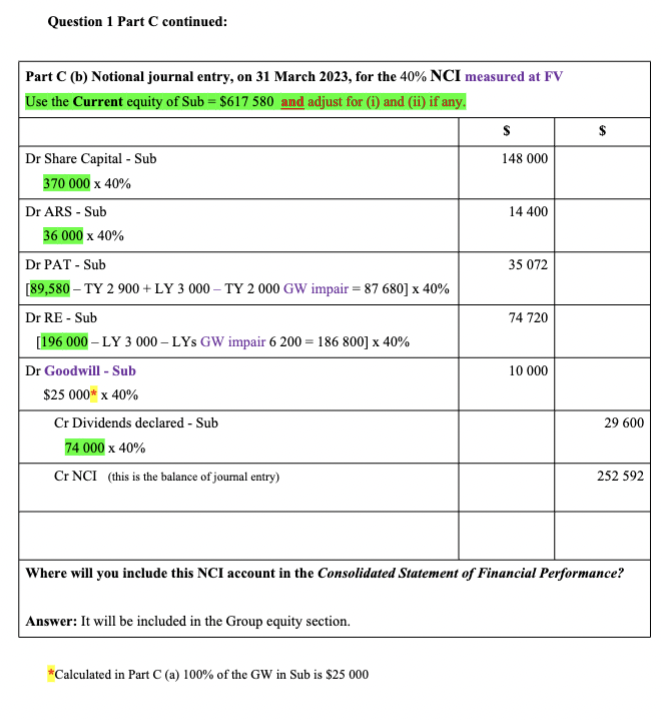

\begin{tabular}{|l|c|c|c|c|r|} \hline Dividend payable to Parent Ltd & - & 30000 & (vii) 30000 & & - \\ \hline Various liabilities & 456624 & 250400 & & & 707024 \\ \hline Loan payable to Parent Ltd & - & 70000 & (vii) 70000 & & - \\ \hline Total liabilities & 456624 & 350400 & & & 707024 \\ \hline Total equity and liabilities & $1245930 & $967980 & & & $1507810 \\ \hline Inventory & 82000 & 53600 & & (vi) 2900 & 132700 \\ \hline Dividend receivable & 30000 & - & & (vii) 30000 & - \\ \hline Various other assets & 443930 & 914380 & & & 1358310 \\ \hline Loan receivable from Sub Ltd & 70000 & - & & (vii) 70000 & - \\ \hline Investment in Sub Ltd & 620000 & - & & (iii) 620000 & - \\ \hline Goodwill & - & - & (iii) 25000 & (iii) 8200 & 16800 \\ \hline Total assets & $1245930 & $967980 & 816150 & 816150 & $1507810 \\ \hline \end{tabular} \begin{tabular}{|l|l|c|c|} \hline (vii) & Dr Loan payable to Parent Ltd - Sub & 70000 & \\ \hline & Cr Loan receivable from Sub - Parent & & 70000 \\ \hline & & & \\ \hline & This notional JE reverses the real JEs below: & 3150 & \\ \hline & Dr Interest income - Parent ** & & 3150 \\ \hline & Ct Interest expense - Sub ** & & \\ \hline & ($700004.5%) & 30000 & \\ \hline & This notional JE reverses the real JEs below: & & 30000 \\ \hline & Dr Dividend payable to Parent - Sub & & \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|} \hline \multirow[t]{3}{*}{ ** } & REAL Parent JE: & & \\ \hline & Dr Cash & 3150 & \\ \hline & Cr Interest Income & & 3150 \\ \hline \multirow[t]{3}{*}{ ** } & REAL Sub JE: & & \\ \hline & Dr Interest Expense & 3150 & \\ \hline & Cr Cash & & 3150 \\ \hline \multirow[t]{5}{*}{ ** } & Parent: & & \\ \hline & Dr Dividend receivable & 74000 & \\ \hline & Cr Dividend income (reversed in notional JE (v)) & & 74000 \\ \hline & Cr Cash & 44000 & \\ \hline & Cr Dividend receivable & & 44000 \\ \hline \multicolumn{4}{|c|}{ Dr Dividend receivable 74000 and Cr Dividend receivable 44000= Div Rec bal left of $30000Dr. } \\ \hline & \multicolumn{3}{|c|}{ You can see this in the GL bal column of the Sub } \\ \hline & Use the same approach for the Sub's real JEs. & & \\ \hline \end{tabular} Current equity of Sub =617580 for Question 1PartC (b) on page 7 \begin{tabular}{|c|c|c|c|} \hline & Question 1 Part C (a) Notional Journal Entries: & & \\ \hline (i) & Not required & & \\ \hline (ii) & Not required & & \\ \hline \multirow[t]{9}{*}{ (iii) } & At date of acq: BV equity =FV equity =$595000 & & \\ \hline & Dr Share capital - Sub 370000100% & 370000 & \\ \hline & Dr REs - Sub 190000100% & 190000 & \\ \hline & Dr ARS - Sub 35000100% & 35000 & \\ \hline & Dr Goodwill - Sub (- Acquisition analysis) & 25000 & \\ \hline & Cr Investment in Sub - Parent & & 620000 \\ \hline & Dr Impairment expense - Sub & 2000 & \\ \hline & Dr REs - Sub (3200+3000) & 6200 & \\ \hline & Cr Goodwill - Sub & & 8200 \\ \hline (iv) & No NCI & & \\ \hline \multirow[t]{2}{*}{ (v) } & Dr Dividend income - Parent & 74000 & \\ \hline & Cr Dividend declared - Sub & & 74000 \\ \hline (vi) & Upward sales: & & \\ \hline \multirow[t]{2}{*}{ LY } & Dr REs - Sub (Sales 8000COGS5000= Profit 3000 ) & 3000 & \\ \hline & Cr COGS - Parent* & & 3000 \\ \hline \multicolumn{4}{|c|}{ *Overstated LY closing inventory becomes Overstated TY opening inventory becomes TY overstated COGS as assumed sol } \\ \hline \multirow[t]{3}{*}{ TY } & Dr Sales - Sub & 7800 & \\ \hline & Cr COGS - Sub (Sales 7800 - profit 2900= COGS 4900 ) & & 4900 \\ \hline & Cr Inventory - Parent (Parent did not sell) & & 2900 \\ \hline \end{tabular} Inswer: It will be included in the Group equity section. Calculated in Part C (a) 100% of the GW in Sub is $25000 \begin{tabular}{|l|c|c|c|c|r|} \hline Dividend payable to Parent Ltd & - & 30000 & (vii) 30000 & & - \\ \hline Various liabilities & 456624 & 250400 & & & 707024 \\ \hline Loan payable to Parent Ltd & - & 70000 & (vii) 70000 & & - \\ \hline Total liabilities & 456624 & 350400 & & & 707024 \\ \hline Total equity and liabilities & $1245930 & $967980 & & & $1507810 \\ \hline Inventory & 82000 & 53600 & & (vi) 2900 & 132700 \\ \hline Dividend receivable & 30000 & - & & (vii) 30000 & - \\ \hline Various other assets & 443930 & 914380 & & & 1358310 \\ \hline Loan receivable from Sub Ltd & 70000 & - & & (vii) 70000 & - \\ \hline Investment in Sub Ltd & 620000 & - & & (iii) 620000 & - \\ \hline Goodwill & - & - & (iii) 25000 & (iii) 8200 & 16800 \\ \hline Total assets & $1245930 & $967980 & 816150 & 816150 & $1507810 \\ \hline \end{tabular} \begin{tabular}{|l|l|c|c|} \hline (vii) & Dr Loan payable to Parent Ltd - Sub & 70000 & \\ \hline & Cr Loan receivable from Sub - Parent & & 70000 \\ \hline & & & \\ \hline & This notional JE reverses the real JEs below: & 3150 & \\ \hline & Dr Interest income - Parent ** & & 3150 \\ \hline & Ct Interest expense - Sub ** & & \\ \hline & ($700004.5%) & 30000 & \\ \hline & This notional JE reverses the real JEs below: & & 30000 \\ \hline & Dr Dividend payable to Parent - Sub & & \\ \hline \end{tabular} \begin{tabular}{|c|c|c|c|} \hline \multirow[t]{3}{*}{ ** } & REAL Parent JE: & & \\ \hline & Dr Cash & 3150 & \\ \hline & Cr Interest Income & & 3150 \\ \hline \multirow[t]{3}{*}{ ** } & REAL Sub JE: & & \\ \hline & Dr Interest Expense & 3150 & \\ \hline & Cr Cash & & 3150 \\ \hline \multirow[t]{5}{*}{ ** } & Parent: & & \\ \hline & Dr Dividend receivable & 74000 & \\ \hline & Cr Dividend income (reversed in notional JE (v)) & & 74000 \\ \hline & Cr Cash & 44000 & \\ \hline & Cr Dividend receivable & & 44000 \\ \hline \multicolumn{4}{|c|}{ Dr Dividend receivable 74000 and Cr Dividend receivable 44000= Div Rec bal left of $30000Dr. } \\ \hline & \multicolumn{3}{|c|}{ You can see this in the GL bal column of the Sub } \\ \hline & Use the same approach for the Sub's real JEs. & & \\ \hline \end{tabular} Current equity of Sub =617580 for Question 1PartC (b) on page 7 \begin{tabular}{|c|c|c|c|} \hline & Question 1 Part C (a) Notional Journal Entries: & & \\ \hline (i) & Not required & & \\ \hline (ii) & Not required & & \\ \hline \multirow[t]{9}{*}{ (iii) } & At date of acq: BV equity =FV equity =$595000 & & \\ \hline & Dr Share capital - Sub 370000100% & 370000 & \\ \hline & Dr REs - Sub 190000100% & 190000 & \\ \hline & Dr ARS - Sub 35000100% & 35000 & \\ \hline & Dr Goodwill - Sub (- Acquisition analysis) & 25000 & \\ \hline & Cr Investment in Sub - Parent & & 620000 \\ \hline & Dr Impairment expense - Sub & 2000 & \\ \hline & Dr REs - Sub (3200+3000) & 6200 & \\ \hline & Cr Goodwill - Sub & & 8200 \\ \hline (iv) & No NCI & & \\ \hline \multirow[t]{2}{*}{ (v) } & Dr Dividend income - Parent & 74000 & \\ \hline & Cr Dividend declared - Sub & & 74000 \\ \hline (vi) & Upward sales: & & \\ \hline \multirow[t]{2}{*}{ LY } & Dr REs - Sub (Sales 8000COGS5000= Profit 3000 ) & 3000 & \\ \hline & Cr COGS - Parent* & & 3000 \\ \hline \multicolumn{4}{|c|}{ *Overstated LY closing inventory becomes Overstated TY opening inventory becomes TY overstated COGS as assumed sol } \\ \hline \multirow[t]{3}{*}{ TY } & Dr Sales - Sub & 7800 & \\ \hline & Cr COGS - Sub (Sales 7800 - profit 2900= COGS 4900 ) & & 4900 \\ \hline & Cr Inventory - Parent (Parent did not sell) & & 2900 \\ \hline \end{tabular} Inswer: It will be included in the Group equity section. Calculated in Part C (a) 100% of the GW in Sub is $25000