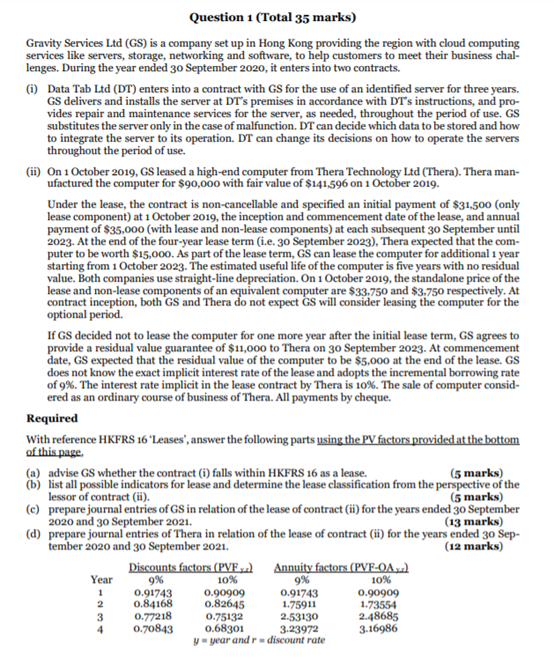

Question 1 (Total 35 marks) Gravity Services Ltd (GS) is a company set up in Hong Kong providing the region with cloud computing services like servers, storage, networking and software, to help customers to meet their business chal- lenges. During the year ended 30 September 2020, it enters into two contracts. (1) Data Tab Ltd (DT) enters into a contract with GS for the use of an identified server for three years. GS delivers and installs the server at DT's premises in accordance with DT's instructions, and pro- vides repair and maintenance services for the server, as needed, throughout the period of use. GS substitutes the server only in the case of malfunction. DT can decide which data to be stored and how to integrate the server to its operation. DT can change its decisions on how to operate the servers throughout the period of use. (ii) On 1 October 2019, GS leased a high-end computer from Thera Technology Ltd (Thera). Thera man- ufactured the computer for $90,000 with fair value of $141,596 on 1 October 2019. Under the lease, the contract is non-cancellable and specified an initial payment of $31,500 (only lease component) at 1 October 2019, the inception and commencement date of the lease, and annual payment of $35.000 (with lease and non-lease components) at each subsequent 30 September until 2023. At the end of the four-year lease term (i.e. 30 September 2023), Thera expected that the com- puter to be worth $15,000. As part of the lease term, GS can lease the computer for additional 1 year starting from 1 October 2023. The estimated useful life of the computer is five years with no residual value. Both companies use straight-line depreciation. On 1 October 2019, the standalone price of the lease and non-lease components of an equivalent computer are $33.750 and $3,750 respectively. At contract inception, both GS and Thera do not expect GS will consider leasing the computer for the optional period. If GS decided not to lease the computer for one more year after the initial lease term, GS agrees to provide a residual value guarantee of $11,000 to Thera on 30 September 2023. At commencement date, GS expected that the residual value of the computer to be $5,000 at the end of the lease. GS does not know the exact implicit interest rate of the lease and adopts the incremental borrowing rate of 9%. The interest rate implicit in the lease contract by Thera is 10%. The sale of computer consid- ered as an ordinary course of business of Thera. All payments by cheque. Required With reference HKFRS 16 'Leases", answer the following parts using the PV factors provided at the bottom of this page (a) advise GS whether the contract (i) falls within HKFRS 16 as a lease. (5 marks) (b) list all possible indicators for lease and determine the lease classification from the perspective of the lessor of contract (ii). (5 marks) (c) prepare journal entries of GS in relation of the lease of contract (ii) for the years ended 30 September 2020 and 30 September 2021. (13 marks) (d) prepare journal entries of Thera in relation of the lease of contract (ii) for the years ended 30 Sep- tember 2020 and 30 September 2021. (12 marks) Discounts factors (PVF x2) Annuity factors (PVF-OA) Year 9% 10% 10% 0.91743 0.90909 0.91743 0.90909 0.84168 0.82645 1.75911 1.73554 0.77218 0.75132 2.53130 2.48685 4 0.70843 0.68301 3.23972 3.16986 year and r discount rate 9% 1 3 Question 1 (Total 35 marks) Gravity Services Ltd (GS) is a company set up in Hong Kong providing the region with cloud computing services like servers, storage, networking and software, to help customers to meet their business chal- lenges. During the year ended 30 September 2020, it enters into two contracts. (1) Data Tab Ltd (DT) enters into a contract with GS for the use of an identified server for three years. GS delivers and installs the server at DT's premises in accordance with DT's instructions, and pro- vides repair and maintenance services for the server, as needed, throughout the period of use. GS substitutes the server only in the case of malfunction. DT can decide which data to be stored and how to integrate the server to its operation. DT can change its decisions on how to operate the servers throughout the period of use. (ii) On 1 October 2019, GS leased a high-end computer from Thera Technology Ltd (Thera). Thera man- ufactured the computer for $90,000 with fair value of $141,596 on 1 October 2019. Under the lease, the contract is non-cancellable and specified an initial payment of $31,500 (only lease component) at 1 October 2019, the inception and commencement date of the lease, and annual payment of $35.000 (with lease and non-lease components) at each subsequent 30 September until 2023. At the end of the four-year lease term (i.e. 30 September 2023), Thera expected that the com- puter to be worth $15,000. As part of the lease term, GS can lease the computer for additional 1 year starting from 1 October 2023. The estimated useful life of the computer is five years with no residual value. Both companies use straight-line depreciation. On 1 October 2019, the standalone price of the lease and non-lease components of an equivalent computer are $33.750 and $3,750 respectively. At contract inception, both GS and Thera do not expect GS will consider leasing the computer for the optional period. If GS decided not to lease the computer for one more year after the initial lease term, GS agrees to provide a residual value guarantee of $11,000 to Thera on 30 September 2023. At commencement date, GS expected that the residual value of the computer to be $5,000 at the end of the lease. GS does not know the exact implicit interest rate of the lease and adopts the incremental borrowing rate of 9%. The interest rate implicit in the lease contract by Thera is 10%. The sale of computer consid- ered as an ordinary course of business of Thera. All payments by cheque. Required With reference HKFRS 16 'Leases", answer the following parts using the PV factors provided at the bottom of this page (a) advise GS whether the contract (i) falls within HKFRS 16 as a lease. (5 marks) (b) list all possible indicators for lease and determine the lease classification from the perspective of the lessor of contract (ii). (5 marks) (c) prepare journal entries of GS in relation of the lease of contract (ii) for the years ended 30 September 2020 and 30 September 2021. (13 marks) (d) prepare journal entries of Thera in relation of the lease of contract (ii) for the years ended 30 Sep- tember 2020 and 30 September 2021. (12 marks) Discounts factors (PVF x2) Annuity factors (PVF-OA) Year 9% 10% 10% 0.91743 0.90909 0.91743 0.90909 0.84168 0.82645 1.75911 1.73554 0.77218 0.75132 2.53130 2.48685 4 0.70843 0.68301 3.23972 3.16986 year and r discount rate 9% 1 3