Answered step by step

Verified Expert Solution

Question

1 Approved Answer

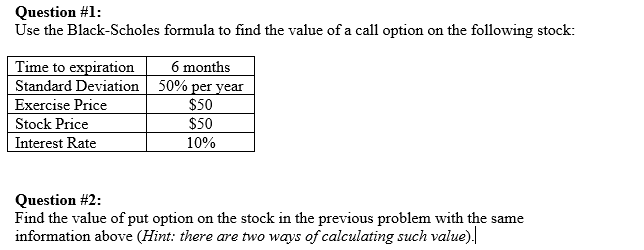

Question #1: Use the Black-Scholes formula to find the value of a call option on the following stock: Time to expiration 6 months Standard Deviation

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Private Equity Edge How Private Equity Players And The Worlds Top Companies Build Value And Wealth

Authors: Arthur B. Laffer,William J. Hass, Shepherd G. Pryor

1st Edition

0071590781,0071642927