Question

Question 1.1. A companys investments earn LIBOR minus 0.5%. Table1: Bid and offer rates in swap market and swap rates (percent per annum) Use Table

Question

1.1. A companys investments earn LIBOR minus 0.5%.

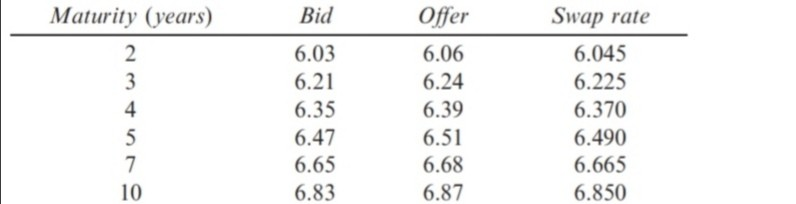

Table1: Bid and offer rates in swap market and swap rates (percent per annum)

Use Table 1 to explain how the company can use the quoted rates to convert the investments to (a) Three-year fixed rate investment (b) Five --year fixed-rate investments. (c) The company also borrowed money at 5.1% for seven years and wishes to convert this borrowing to a floating-rate liability by making use of the swap quotes in table 1, explain how this can be done.

Bid Maturity (years) 2 3 4 5 7 10 6.03 6.21 6.35 6.47 6.65 6.83 Offer 6.06 6.24 6.39 6.51 6.68 6.87 Swap rate 6.045 6.225 6.370 6.490 6.665 6.850 Bid Maturity (years) 2 3 4 5 7 10 6.03 6.21 6.35 6.47 6.65 6.83 Offer 6.06 6.24 6.39 6.51 6.68 6.87 Swap rate 6.045 6.225 6.370 6.490 6.665 6.850Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Executive Finance And Strategy

Authors: Ralph Tiffin

1st Edition

0749471506, 978-0749471507