Answered step by step

Verified Expert Solution

Question

1 Approved Answer

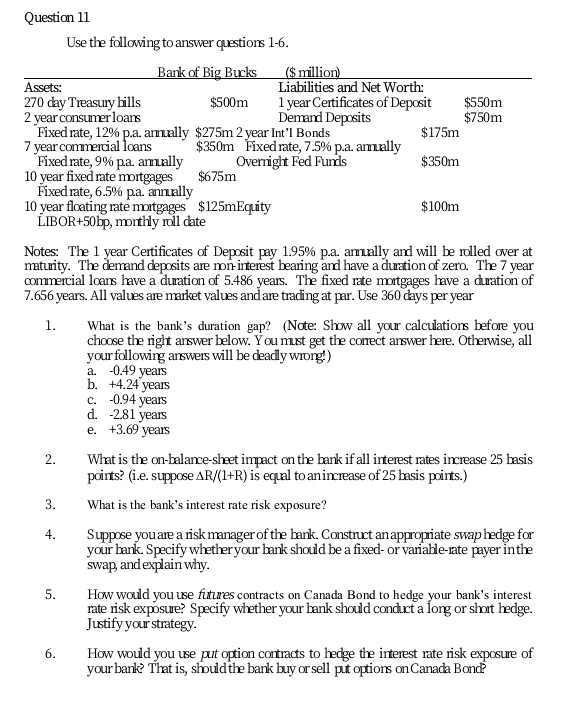

Question 11 Use the following to answer questions 1-6. Bank of Big Bucks ($ million) Assets: Liabilities and Net Worth: 270 day Treasury bills $500m

Question 11 Use the following to answer questions 1-6. Bank of Big Bucks ($ million) Assets: Liabilities and Net Worth: 270 day Treasury bills $500m 1 year Certificates of Deposit $550m 2 year consumer loans Demand Deposits $750m Fixed rate, 12% p.a. arnally $275m 2 year Int'l Bonds $175m 7 year commercial loans $350m Fixed rate, 7.5% p.a. arnally Fixed rate, 9% pa. amially Overnight Fed Funds $350m 10 year fixed rate mortgages $675m Fixed rate, 6.5% pa. annally 10 year floating rate mortgages $125mEquity $100m LIBOR+50 bp, monthly roll date Notes: The 1 year Certificates of Deposit pay 1.95% p.a. amelly and will be rolled over at maturity. The demand deposits are non-interest bearing and have a duration of zero. The 7 year commercial loans have a duration of 5.486 years. The fixed rate mortgages have a duration of 7.656 years. All values are market values and are trading at par. Use 360 days per year 1. What is the bank's duration gap? (Note: Show all your calculations before you choose the right answer below. You must get the correct answer here. Otherwise, all your following answers will be deady wrong!) a. -0.49 years b. +4.24 years c. -0.94 years d. -281 years e. +3.69 years 2. What is the on-balance-sheet impact on the bank if all interest rates increase 25 basis points? (i.e. suppose AR/(1+R) is equal to an increase of 25 basis points.) 3. What is the bank's interest rate risk exposure? Suppose you are a risk manager of the bank. Construct an appropriate swap hedge for your bank. Specify whether your bank should be a fixed- or variable-rate payer in the swap, and explain why. 5. How would you use futures contracts on Canada Bond to hedge your bank's interest rate risk exposure? Specify whether your bank should conduct a long or short hedge. Justify your strategy. 6. How would you use put option contracts to hedge the interest rate risk exposure of your bank? That is, should the bank buy or sell put options on Canada Bond 4. Question 11 Use the following to answer questions 1-6. Bank of Big Bucks ($ million) Assets: Liabilities and Net Worth: 270 day Treasury bills $500m 1 year Certificates of Deposit $550m 2 year consumer loans Demand Deposits $750m Fixed rate, 12% p.a. arnally $275m 2 year Int'l Bonds $175m 7 year commercial loans $350m Fixed rate, 7.5% p.a. arnally Fixed rate, 9% pa. amially Overnight Fed Funds $350m 10 year fixed rate mortgages $675m Fixed rate, 6.5% pa. annally 10 year floating rate mortgages $125mEquity $100m LIBOR+50 bp, monthly roll date Notes: The 1 year Certificates of Deposit pay 1.95% p.a. amelly and will be rolled over at maturity. The demand deposits are non-interest bearing and have a duration of zero. The 7 year commercial loans have a duration of 5.486 years. The fixed rate mortgages have a duration of 7.656 years. All values are market values and are trading at par. Use 360 days per year 1. What is the bank's duration gap? (Note: Show all your calculations before you choose the right answer below. You must get the correct answer here. Otherwise, all your following answers will be deady wrong!) a. -0.49 years b. +4.24 years c. -0.94 years d. -281 years e. +3.69 years 2. What is the on-balance-sheet impact on the bank if all interest rates increase 25 basis points? (i.e. suppose AR/(1+R) is equal to an increase of 25 basis points.) 3. What is the bank's interest rate risk exposure? Suppose you are a risk manager of the bank. Construct an appropriate swap hedge for your bank. Specify whether your bank should be a fixed- or variable-rate payer in the swap, and explain why. 5. How would you use futures contracts on Canada Bond to hedge your bank's interest rate risk exposure? Specify whether your bank should conduct a long or short hedge. Justify your strategy. 6. How would you use put option contracts to hedge the interest rate risk exposure of your bank? That is, should the bank buy or sell put options on Canada Bond 4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Winning The Losers Game Timeless Strategies For Successful Investing

Authors: Charles D. Ellis

5th Edition

0071545492,0071545506