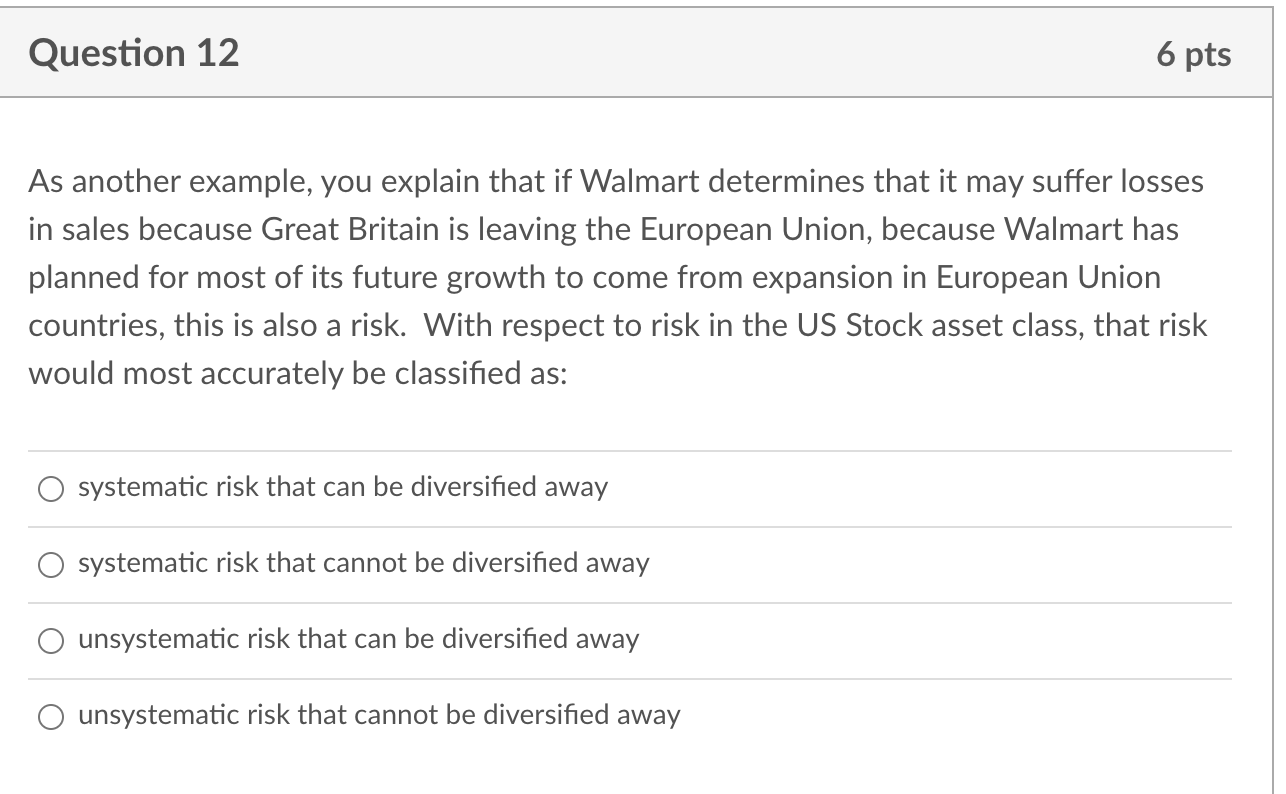

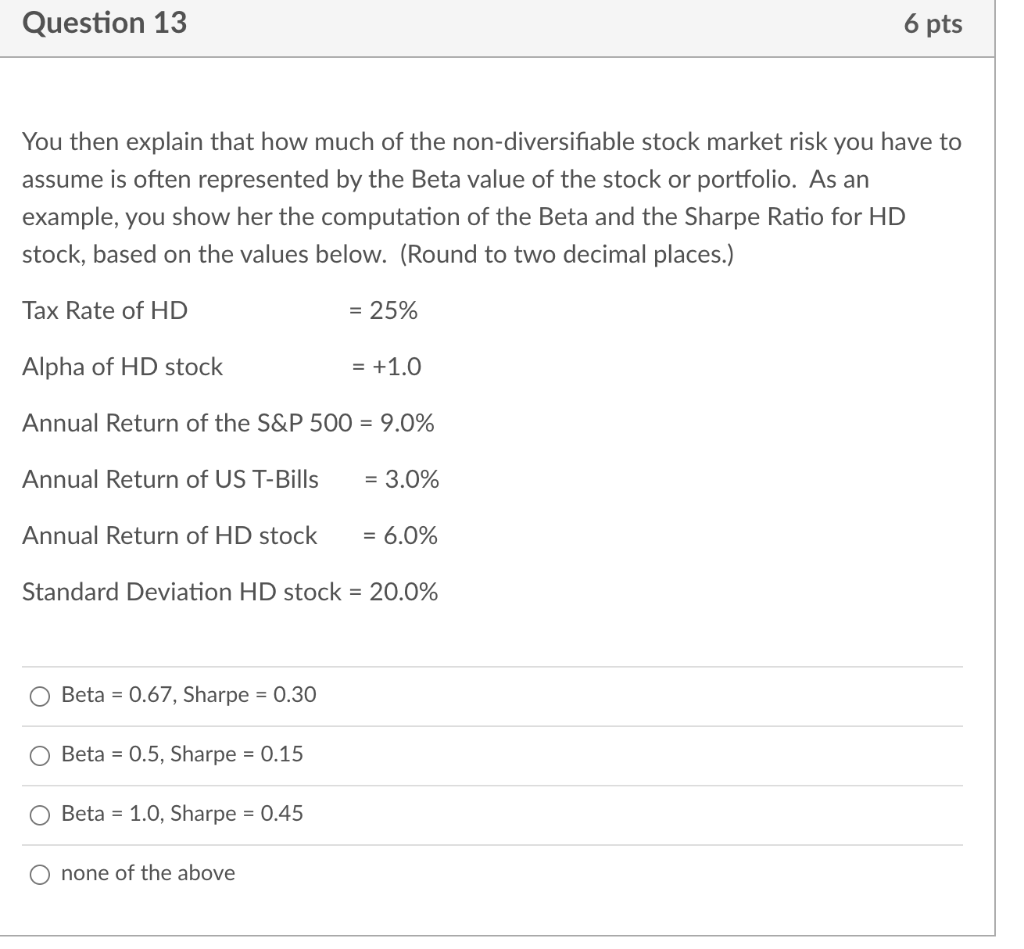

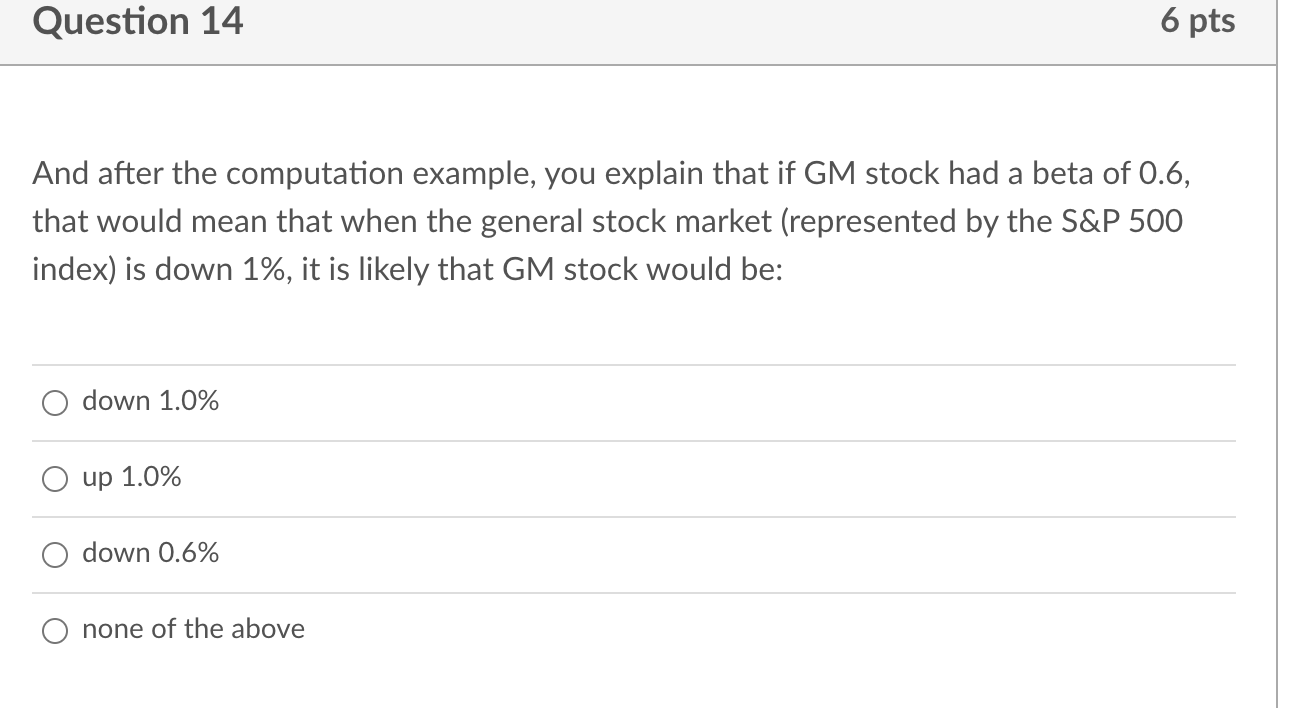

Question 12 6 pts As another example, you explain that if Walmart determines that it may suffer losses in sales because Great Britain is leaving the European Union, because Walmart has planned for most of its future growth to come from expansion in European Union countries, this is also a risk. With respect to risk in the US Stock asset class, that risk would most accurately be classified as: systematic risk that can be diversified away systematic risk that cannot be diversified away unsystematic risk that can be diversified away unsystematic risk that cannot be diversified away Question 13 6 pts You then explain that how much of the non-diversifiable stock market risk you have to assume is often represented by the Beta value of the stock or portfolio. As an example, you show her the computation of the Beta and the Sharpe Ratio for HD stock, based on the values below. (Round to two decimal places.) Tax Rate of HD = 25% Alpha of HD stock = +1.0 Annual Return of the S&P 500 = 9.0% Annual Return of US T-Bills = 3.0% Annual Return of HD stock = 6.0% Standard Deviation HD stock = 20.0% O Beta = 0.67, Sharpe = 0.30 Beta = 0.5, Sharpe = 0.15 Beta = 1.0, Sharpe = 0.45 of the above Question 14 6 pts And after the computation example, you explain that if GM stock had a beta of 0.6, that would mean that when the general stock market (represented by the S&P 500 index) is down 1%, it is likely that GM stock would be: down 1.0% up 1.0% down 0.6% none of the above Question 15 6 pts You then add that if there is additional stock market return, and risk, beyond the beta measurement, we say the stock or portfolio has an "alpha." As an example, if Treasury Bills are earning 1%, and if WM stock has an Alpha of +1.5% and a Beta of 1.0, and the general stock market (the S&P 500 index) goes up from a 10% return to an 11% return, which of the following statements is most accurate? WM will go up 1.5% WM will go up 1.5 times more than the index WM will outperform the index return by 1.5% O WM return will always equal the index return Question 16 7 pts This leads to the description of the 6 basic risk categories, and the first category that you address is risk that is summarized by the word "correlation." To show the actual computation of correlation between two companies she is familiar with, you perform the following in Excel: Compute using the exam spreadsheet, on tab "C" ("Lowes and Home Depot 2018- 2019") the CORRELATION COEFFICIENT of the monthly HPRs for Lowes and Home Depot for all of the months listed. Round to two decimal places. The exam spreadsheet is on the opening page of the exam. 0.88 O 0.65 O 0.91 O 0.83