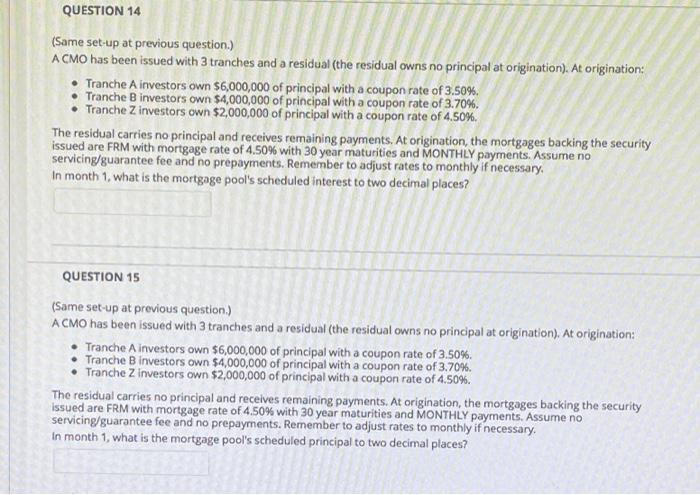

QUESTION 14 (Same set-up at previous question.) A CMO has been issued with 3 tranches and a residual (the residual owns no principal at origination). At origination: Tranche A investors own $6,000,000 of principal with a coupon rate of 3.50%. Tranche B investors own $4,000,000 of principal with a coupon rate of 3.70%. Tranche Zinvestors own $2,000,000 of principal with a coupon rate of 4.50%. The residual carries no principal and receives remaining payments. At origination, the mortgages backing the security issued are FRM with mortgage rate of 4.50% with 30 year maturities and MONTHLY payments. Assume no servicing/guarantee fee and no prepayments. Remember to adjust rates to monthly if necessary. In month 1, what is the mortgage pool's scheduled interest to two decimal places? QUESTION 15 (Same set-up at previous question.) ACMO has been issued with 3 tranches and a residual (the residual owns no principal at origination. At origination: Tranche A investors own $6,000,000 of principal with a coupon rate of 3.50%. Tranche B investors own $4,000,000 of principal with a coupon rate of 3.70%. Tranche 2 investors own $2,000,000 of principal with a coupon rate of 4.50%. The residual carries no principal and receives remaining payments. At origination, the mortgages backing the security Issued are FRM with mortgage rate of 4.50% with 30 year maturities and MONTHLY payments. Assume no servicing/guarantee fee and no prepayments. Remember to adjust rates to monthly if necessary. In month 1, what is the mortgage pool's scheduled principal to two decimal places? QUESTION 14 (Same set-up at previous question.) A CMO has been issued with 3 tranches and a residual (the residual owns no principal at origination). At origination: Tranche A investors own $6,000,000 of principal with a coupon rate of 3.50%. Tranche B investors own $4,000,000 of principal with a coupon rate of 3.70%. Tranche Zinvestors own $2,000,000 of principal with a coupon rate of 4.50%. The residual carries no principal and receives remaining payments. At origination, the mortgages backing the security issued are FRM with mortgage rate of 4.50% with 30 year maturities and MONTHLY payments. Assume no servicing/guarantee fee and no prepayments. Remember to adjust rates to monthly if necessary. In month 1, what is the mortgage pool's scheduled interest to two decimal places? QUESTION 15 (Same set-up at previous question.) ACMO has been issued with 3 tranches and a residual (the residual owns no principal at origination. At origination: Tranche A investors own $6,000,000 of principal with a coupon rate of 3.50%. Tranche B investors own $4,000,000 of principal with a coupon rate of 3.70%. Tranche 2 investors own $2,000,000 of principal with a coupon rate of 4.50%. The residual carries no principal and receives remaining payments. At origination, the mortgages backing the security Issued are FRM with mortgage rate of 4.50% with 30 year maturities and MONTHLY payments. Assume no servicing/guarantee fee and no prepayments. Remember to adjust rates to monthly if necessary. In month 1, what is the mortgage pool's scheduled principal to two decimal places