Answered step by step

Verified Expert Solution

Question

1 Approved Answer

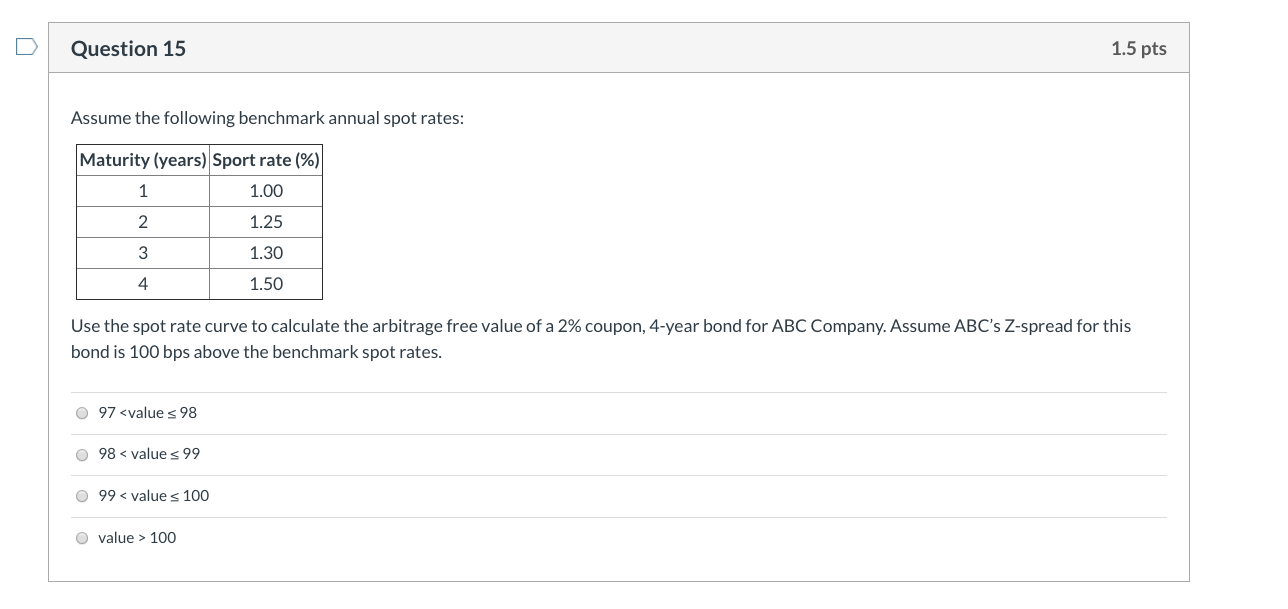

Question 15 1.5 pts Assume the following benchmark annual spot rates: Maturity (years) Sport rate (%) 1.00 1 2 1.25 3 1.30 4 1.50 Use

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dynamic Asset Allocation With Forwards And Futures

Authors: Abraham Lioui , Patrice Poncet

1st Edition

0387241078,038724106X