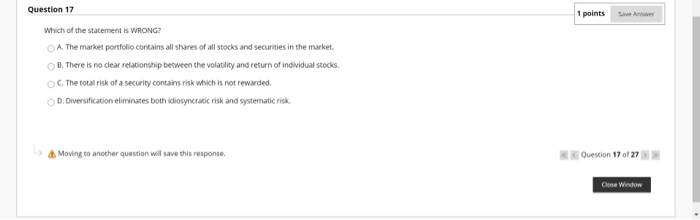

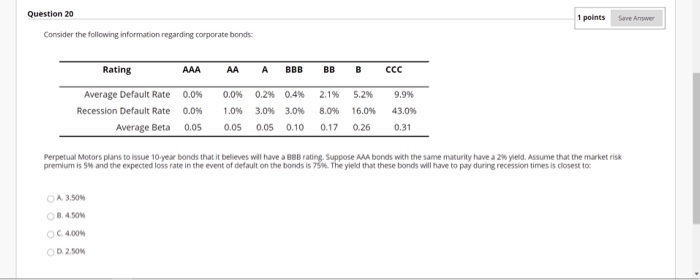

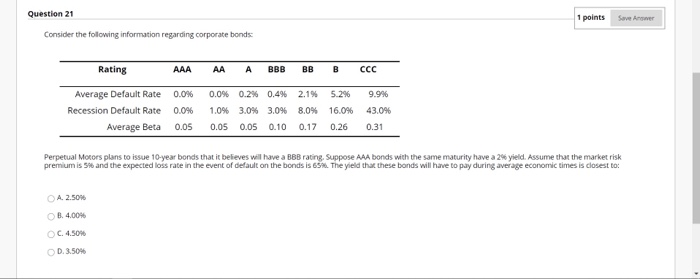

Question 17 1 points Which of the statement is WRONG? A. The market portfolio contains all shares of all stocks and securities in the market. B. There is no clear relationship between the volatility and return of individual stocks. OC. The total risk of a security contains risk which is not rewarded. D. Diversification eliminates both idiosyncratic risk and systematic risk 4 Moving to another question will save this response. I Question 17 of 27 Close Window Question 18 1 points Save As Assume that the S&P 500 currently has a dividend yield of 3 and that on average, the dividends of S&P 500 firms have increased by about 5% per year. If the risk-free interest rate is 4 then your estimate for the future market risk premium is: A 64 B. C. 45 D. Question 19 1 points Save Answer Colt Systems will have EBIT this coming year of $18 million. It will also spend $7 million on total capital expenditures and increases in net working capital and have $4 million in depreciation expenses. Colt is currently an all-equity firm with a corporate tax rate of 30% and a cost of capital of 119. Cole's free cash flows are expected to grow by 9.5% per year, what is the market value of its equity today? A $1,573.33 milion B. $1,000 million OC 51,106,67 milion D. 5640 milion Question 20 1 points Save Answer Consider the following information regarding corporate bonds: Rating AAA AA BBB BB B CCC 5.2% Average Default Rate 0.0% Recession Default Rate 0.0% Average Beta 0.05 0.0% 0.2% 0.4% 1.0% 30% 3.0% 0.05 0.05 0.10 2.1% 8.0% 16.0% 0.26 9.9% 43.0 0.31 0.17 Perpetual Motors plans to issue 10 year bonds that it believes will have a BBB rating. Suppose AAA bonds with the same maturity have a 25 yield. Assume that the market risk premium is 5 and the expected loss rate in the event of default on the bonds is 79. The yield that these bonds will have to pay during recession times is closest to A 3.50 C 4.00 02.50 Question 21 1 points Save Answer Consider the following information regarding corporate bonds Rating AAA AA BBB BB B CCC 0.0% 9.9% Average Default Rate Recession Default Rate Average Beta 0.0% 0.05 0.0% 0.2% 0.4% 2.1% 5.2% 1.0% 3.0% 3.0% 8.0% 16.0% 0.05 0.05 0.10 0.17 0.26 43.0% 0.31 Perpetual Motors plans to issue 10-year bonds that it believes will have a BBB rating. Suppose AAA bonds with the same maturity have a 2% yield. Assume that the market risk premium is 58 and the expected loss rate in the event of default on the bonds is 65%. The yield that these bonds will have to pay during average economic times is closest to A 2.50 OB. 4.00% C. 4.50% D. 3.50%