Answered step by step

Verified Expert Solution

Question

1 Approved Answer

QUESTION 17 ONLY DO 1-3 YEARS IGNORE THE 4TH 14. An entity must adjust its financial statement for an event that occurs after the end

QUESTION 17 ONLY DO 1-3 YEARS IGNORE THE 4TH

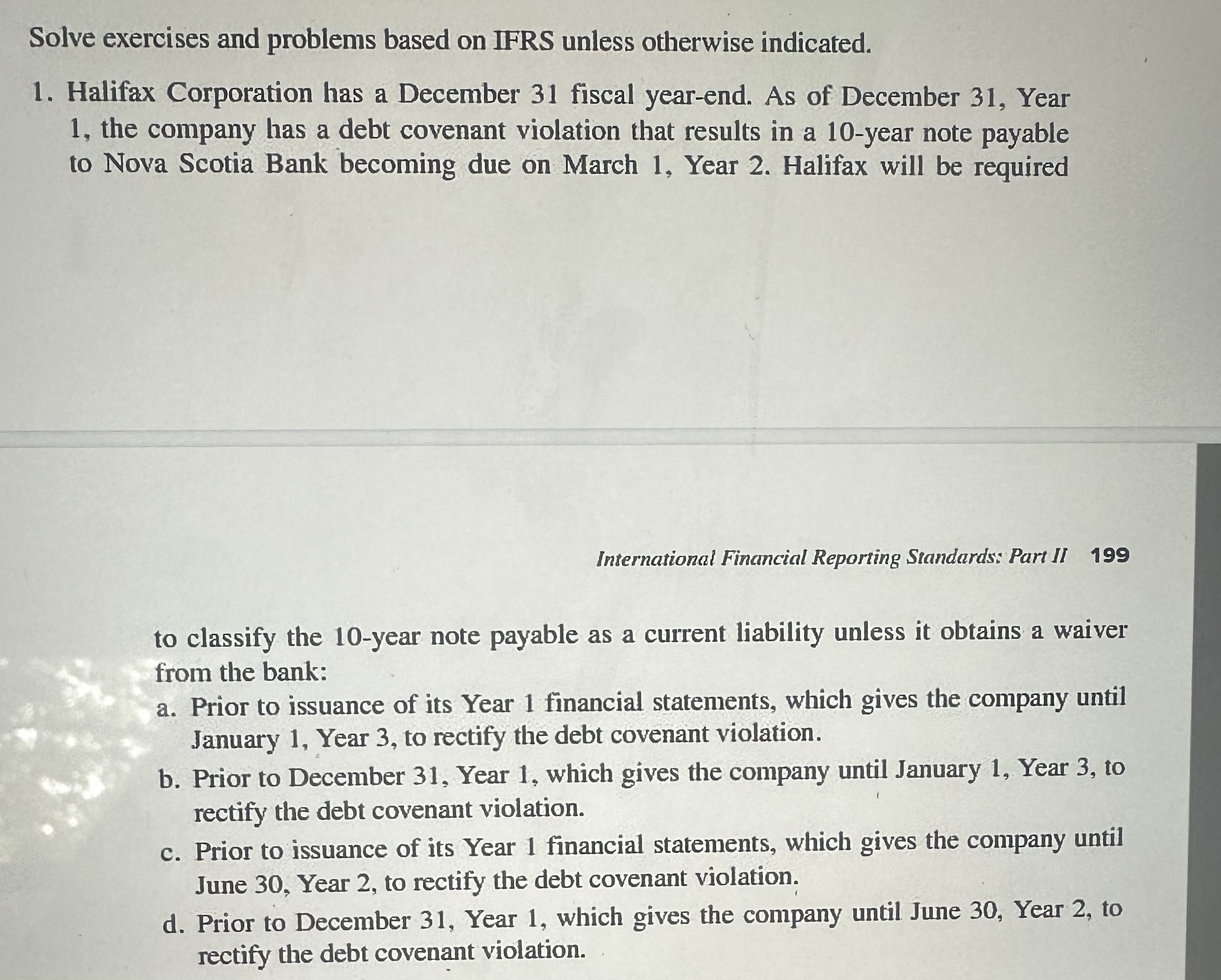

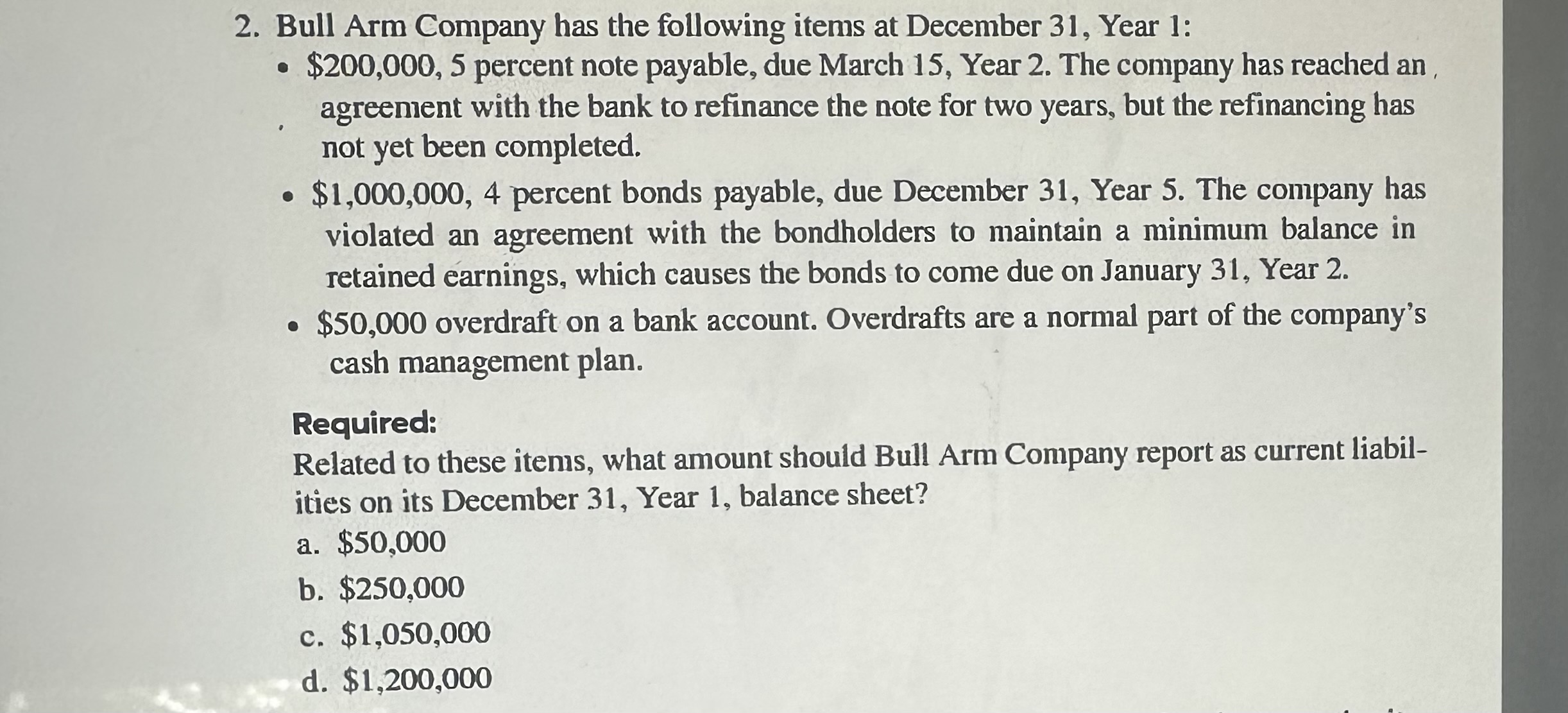

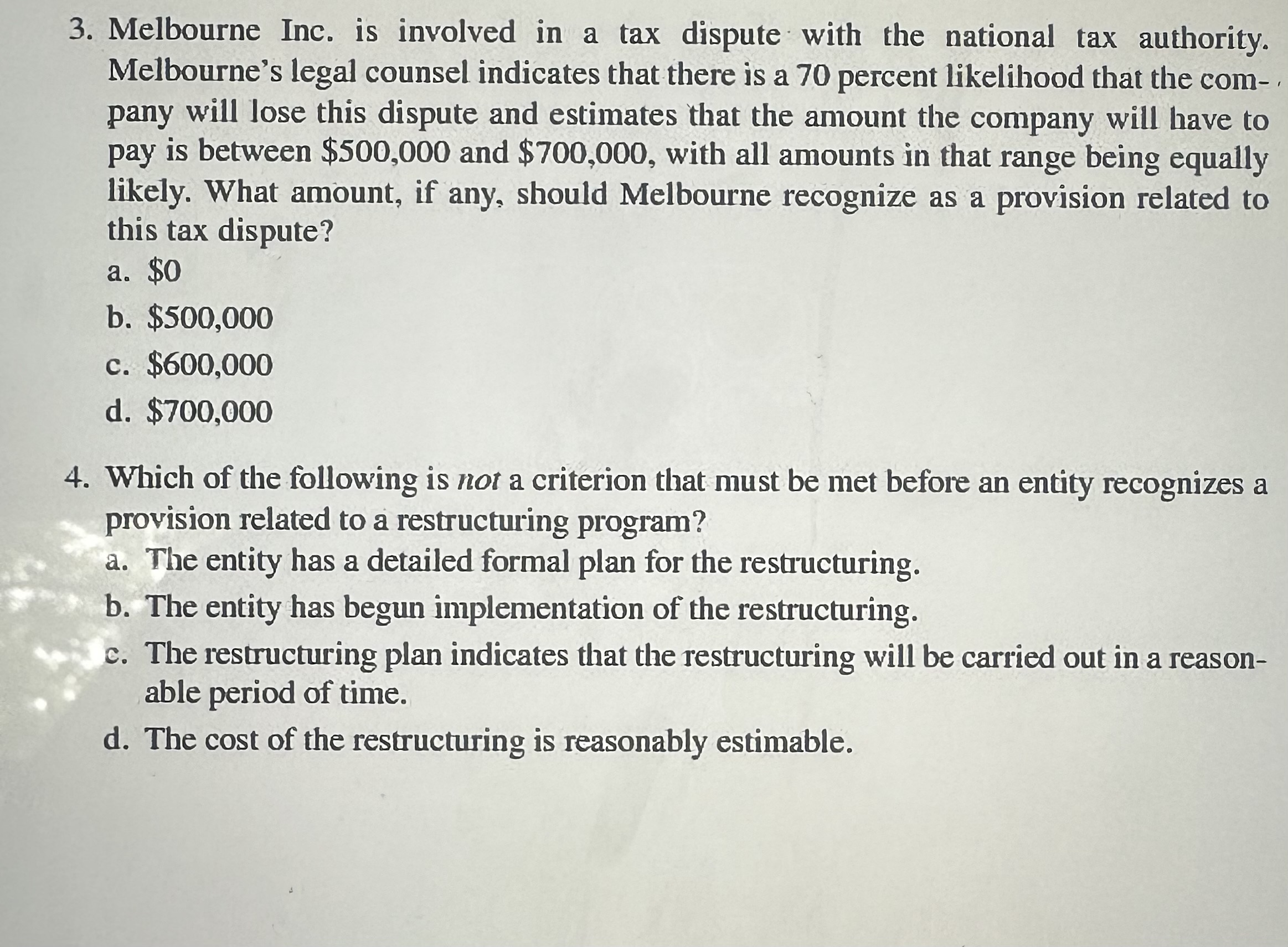

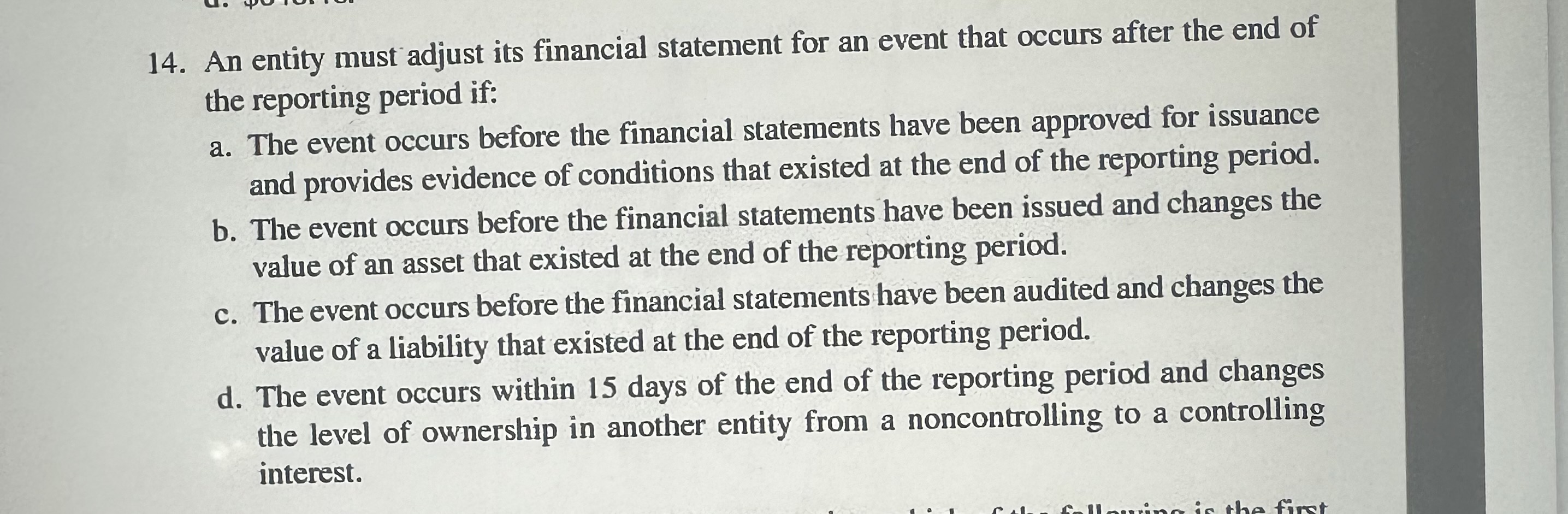

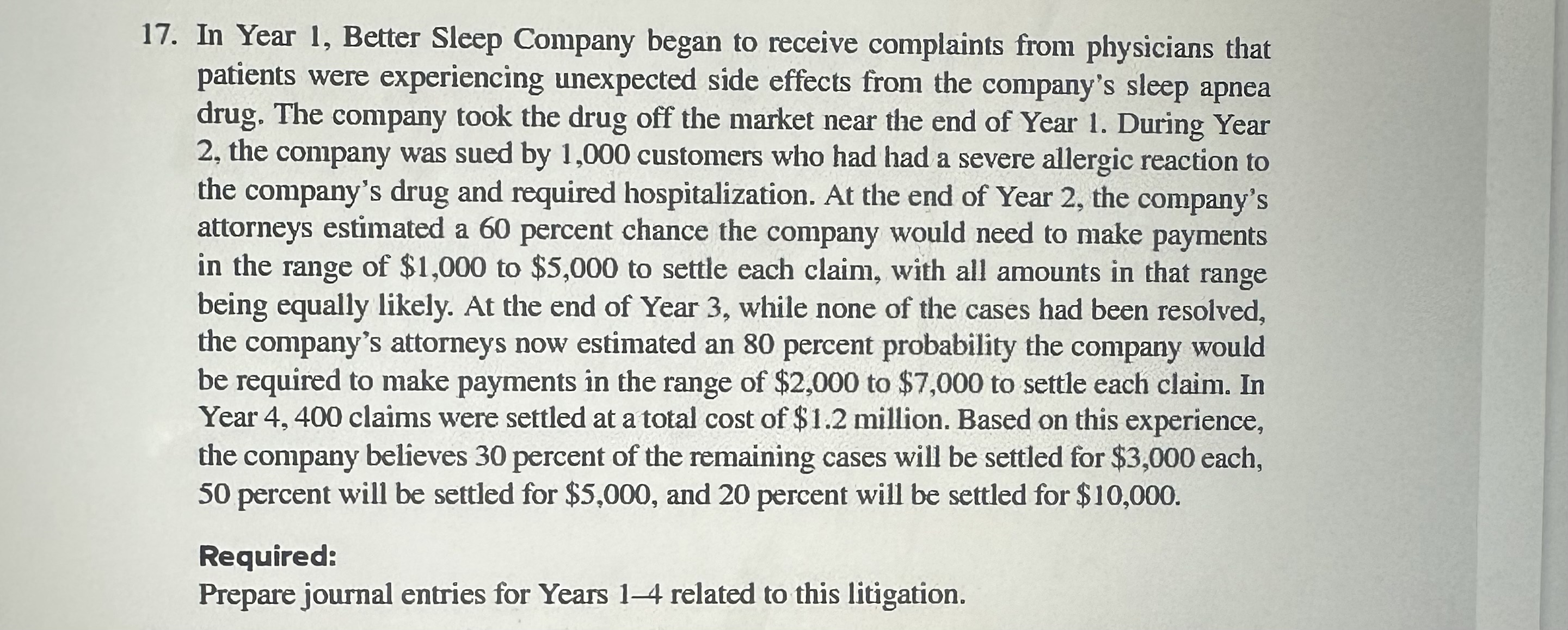

14. An entity must adjust its financial statement for an event that occurs after the end of the reporting period if: a. The event occurs before the financial statements have been approved for issuance and provides evidence of conditions that existed at the end of the reporting period. b. The event occurs before the financial statements have been issued and changes the value of an asset that existed at the end of the reporting period. c. The event occurs before the financial statements have been audited and changes the value of a liability that existed at the end of the reporting period. d. The event occurs within 15 days of the end of the reporting period and changes the level of ownership in another entity from a noncontrolling to a controlling interest. 3. Melbourne Inc is involved in a tax dispute with the national tax authority. Melbourne's legal counsel indicates that there is a 70 percent likelihood that the company will lose this dispute and estimates that the amount the company will have to pay is between $500,000 and $700,000, with all amounts in that range being equally likely. What amount, if any, should Melbourne recognize as a provision related to this tax dispute? a. $0 b. $500,000 c. $600,000 d. $700,000 4. Which of the following is not a criterion that must be met before an entity recognizes a provision related to a restructuring program? a. The entity has a detailed formal plan for the restructuring. b. The entity has begun implementation of the restructuring. c. The restructuring plan indicates that the restructuring will be carried out in a reasonable period of time. d. The cost of the restructuring is reasonably estimable. Solve exercises and problems based on IFRS unless otherwise indicated. 1. Halifax Corporation has a December 31 fiscal year-end. As of December 31, Year 1 , the company has a debt covenant violation that results in a 10 -year note payable to Nova Scotia Bank becoming due on March 1, Year 2. Halifax will be required International Financial Reporting Standards: Part II 199 to classify the 10-year note payable as a current liability unless it obtains a waiver from the bank: a. Prior to issuance of its Year 1 financial statements, which gives the company until January 1 , Year 3, to rectify the debt covenant violation. b. Prior to December 31, Year 1, which gives the company until January 1, Year 3, to rectify the debt covenant violation. c. Prior to issuance of its Year 1 financial statements, which gives the company until June 30, Year 2, to rectify the debt covenant violation. d. Prior to December 31, Year 1, which gives the company until June 30, Year 2, to rectify the debt covenant violation. 7. In Year 1, Better Sleep Company began to receive complaints from physicians that patients were experiencing unexpected side effects from the company's sleep apnea drug. The company took the drug off the market near the end of Year 1. During Year 2 , the company was sued by 1,000 customers who had had a severe allergic reaction to the company's drug and required hospitalization. At the end of Year 2, the company's attorneys estimated a 60 percent chance the company would need to make payments in the range of $1,000 to $5,000 to settle each claim, with all amounts in that range being equally likely. At the end of Year 3 , while none of the cases had been resolved, the company's attorneys now estimated an 80 percent probability the company would be required to make payments in the range of $2,000 to $7,000 to settle each claim. In Year 4, 400 claims were settled at a total cost of $1.2 million. Based on this experience, the company believes 30 percent of the remaining cases will be settled for $3,000 each, 50 percent will be settled for $5,000, and 20 percent will be settled for $10,000. Required: Prepare journal entries for Years 1-4 related to this litigation. 2. Bull Arm Company has the following items at December 31 , Year 1: - $200,000,5 percent note payable, due March 15, Year 2. The company has reached an, agreement with the bank to refinance the note for two years, but the refinancing has not yet been completed. - $1,000,000,4 percent bonds payable, due December 31, Year 5. The company has violated an agreement with the bondholders to maintain a minimum balance in retained arnings, which causes the bonds to come due on January 31 , Year 2. - $50,000 overdraft on a bank account. Overdrafts are a normal part of the company's cash management plan. Required: Related to these items, what amount should Bull Arm Company report as current liabilities on its December 31, Year 1, balance sheet? a. $50,000 b. $250,000 c. $1,050,000 d. $1,200,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Accounting Principles Volume 2

Authors: John Wild, Ken Shaw, Barbara Chiappetta

21st Edition

0077716663, 978-0077716660