Answered step by step

Verified Expert Solution

Question

1 Approved Answer

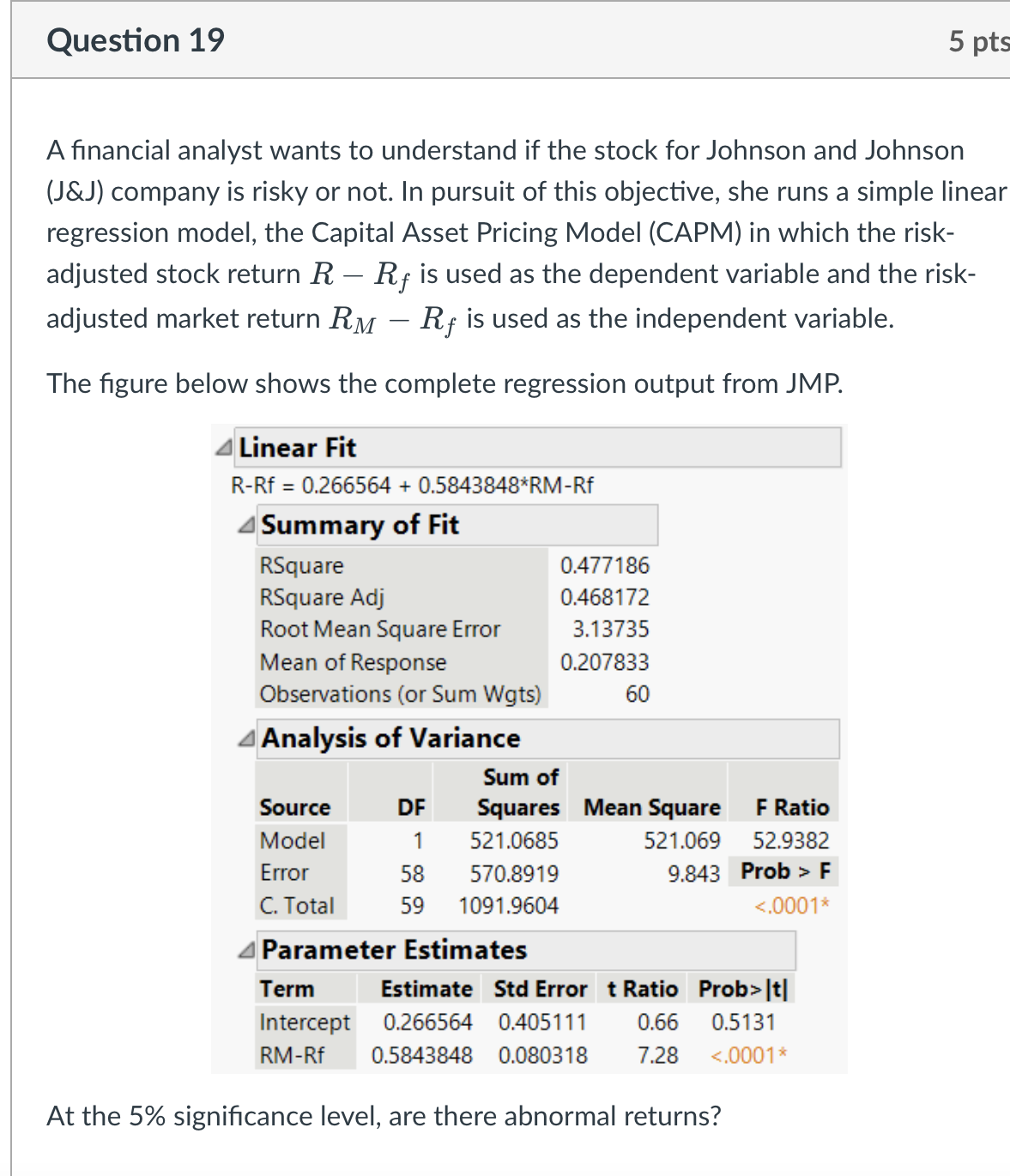

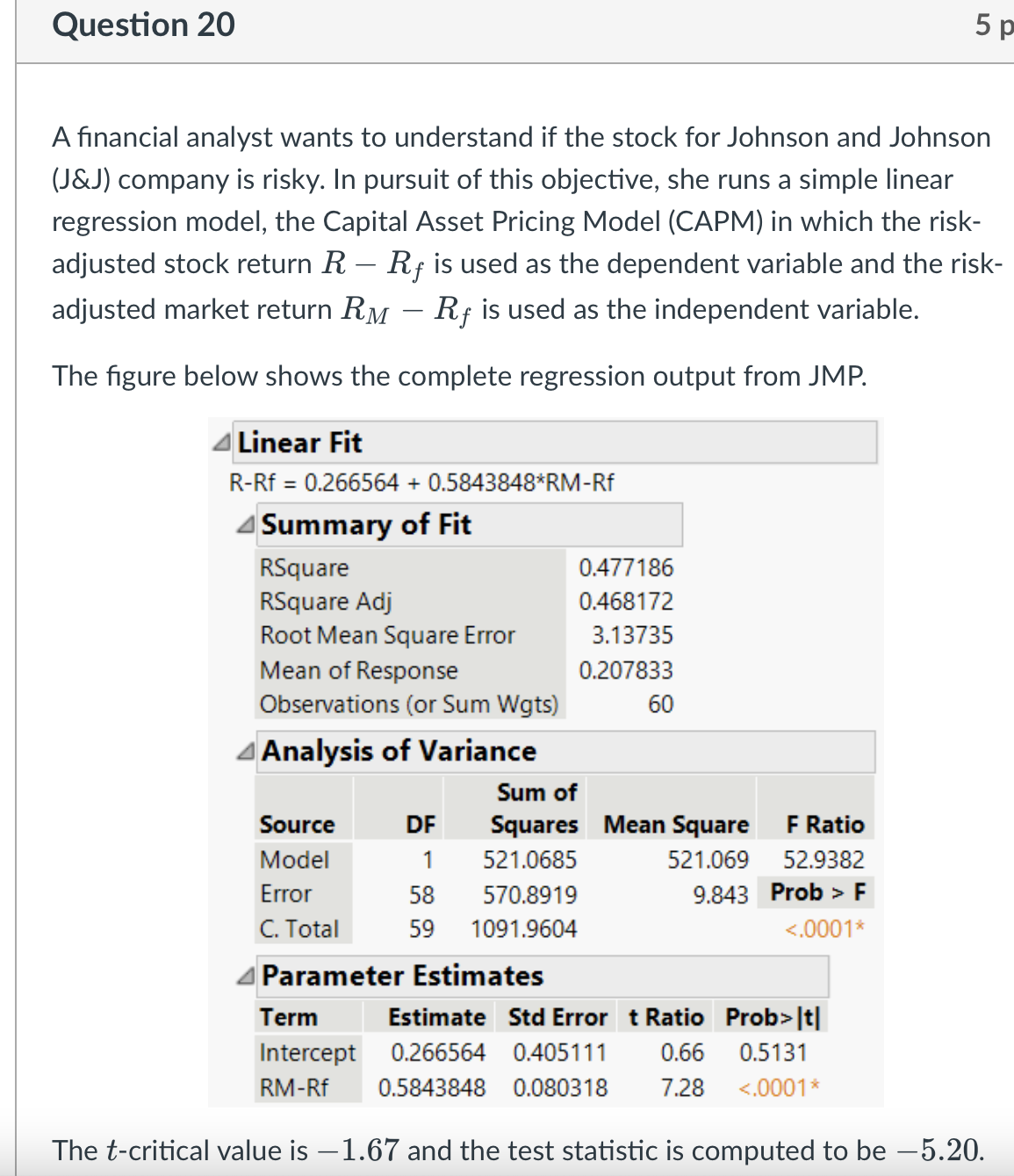

Question 19 5 pts A financial analyst wants to understand if the stock for Johnson and Johnson (J&J) company is risky or not. In pursuit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Calculus Single And Multivariable

Authors: Deborah Hughes Hallett, Andrew M Gleason, William G McCallum

8th Edition

1119783267, 9781119783268