Answered step by step

Verified Expert Solution

Question

1 Approved Answer

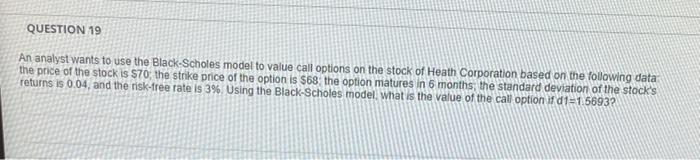

QUESTION 19 An analyst wants to use the Black-Scholes model to value call options on the stock of Heath Corporation based on the following data

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding ETF Options Profitable Strategies For Diversified Low Risk Investing

Authors: Kenneth R. Trester

1st Edition

007176030X, 0071760431, 9780071760430