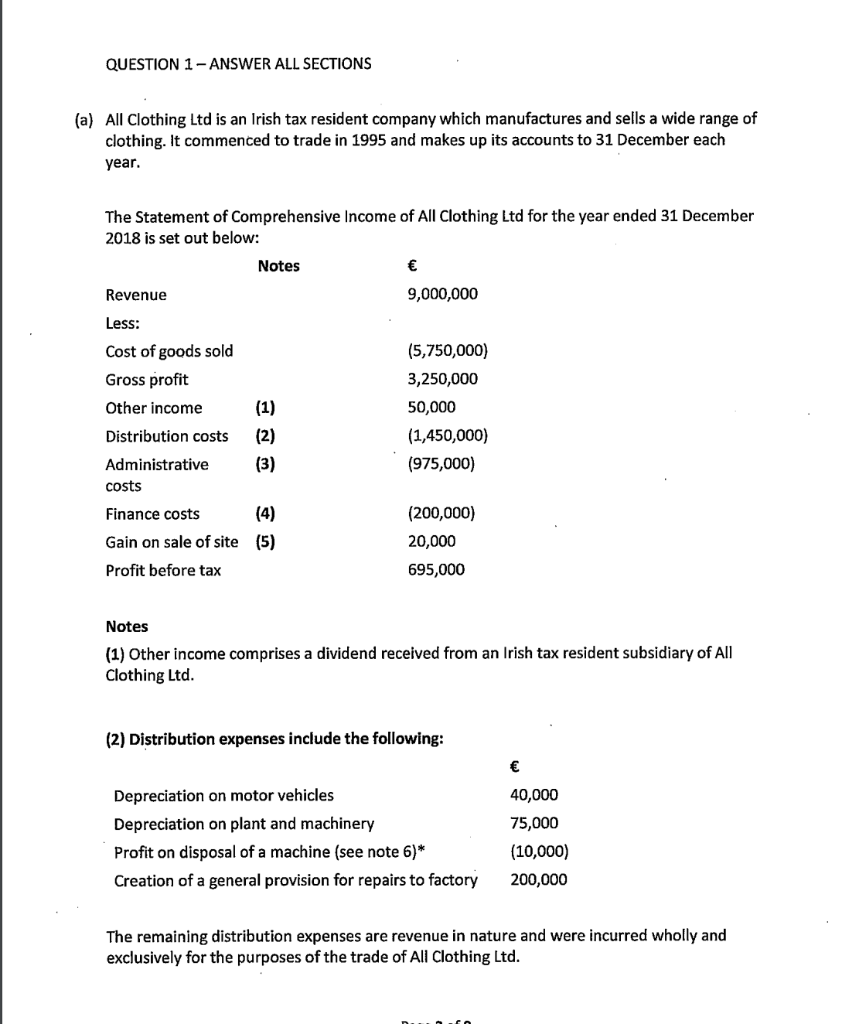

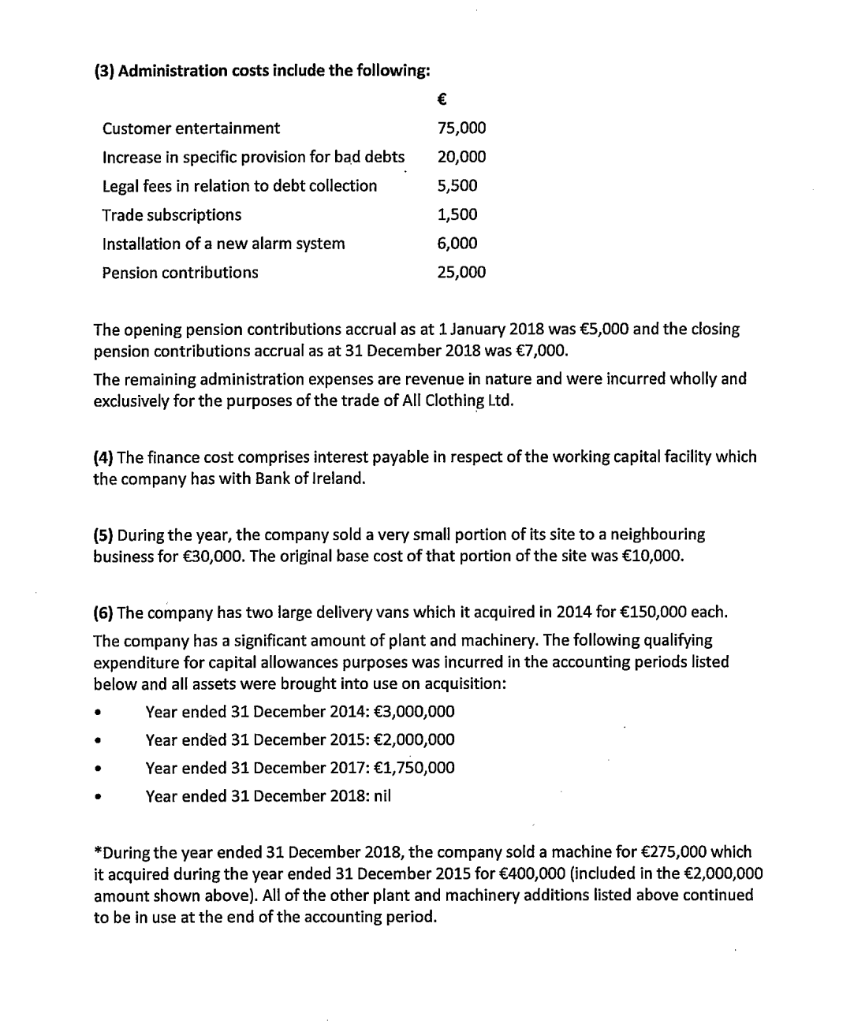

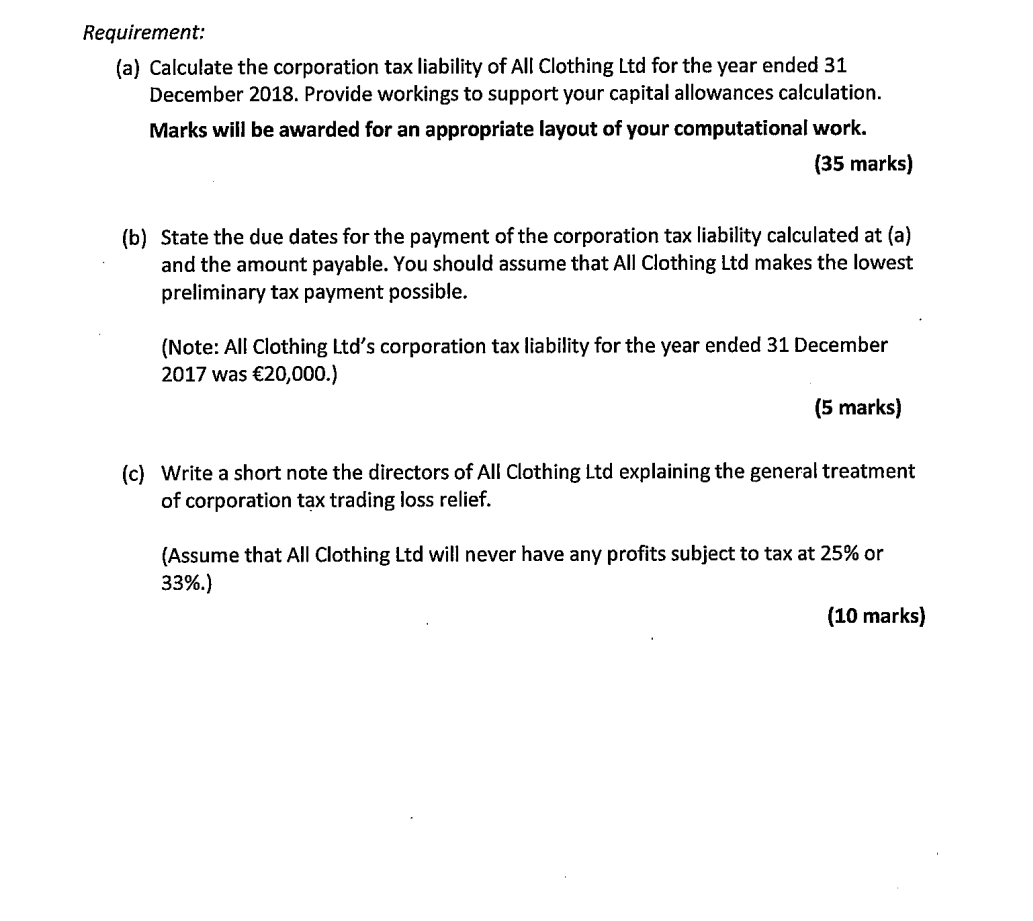

QUESTION 1-ANSWER ALL SECTIONS (a) All Clothing Ltd is an Irish tax resident company which manufactures and sells a wide range of clothing. It commenced to trade in 1995 and makes up its accounts to 31 December each year. The Statement of Comprehensive Income of All Clothing Ltd for the year ended 31 December 2018 is set out below: Notes Revenue 9,000,000 Less: Cost of goods sold (5,750,000) Gross profit 3,250,000 Other income (1) 50,000 Distribution costs (2) (1,450,000) Administrative (3) (975,000) costs Finance costs (4) (200,000) Gain on sale of site (5) 20,000 Profit before tax 695,000 Notes (1) Other income comprises a dividend received from an Irish tax resident subsidiary of All Clothing Ltd. (2) Distribution expenses include the following: Depreciation on motor vehicles 40,000 Depreciation on plant and machinery 75,000 Profit on disposal of a machine (see note 6)* (10,000) Creation of a general provision for repairs to factory 200,000 The remaining distribution expenses are revenue in nature and were incurred wholly and exclusively for the purposes of the trade of All Clothing Ltd. (3) Administration costs include the following: Customer entertainment 75,000 Increase in specific provision for bad debts 20,000 Legal fees in relation to debt collection 5,500 Trade subscriptions 1,500 Installation of a new alarm system 6,000 Pension contributions 25,000 The opening pension contributions accrual as at 1 January 2018 was 5,000 and the closing pension contributions accrual as at 31 December 2018 was 7,000. The remaining administration expenses are revenue in nature and were incurred wholly and exclusively for the purposes of the trade of All Clothing Ltd. (4) The finance cost comprises interest payable in respect of the working capital facility which the company has with Bank of Ireland. (5) During the year, the company sold a very small portion of its site to a neighbouring business for 30,000. The original base cost of that portion of the site was 10,000. (6) The company has two large delivery vans which it acquired in 2014 for 150,000 each. The company has a significant amount of plant and machinery. The following qualifying expenditure for capital allowances purposes was incurred in the accounting periods listed below and all assets were brought into use on acquisition: . Year ended 31 December 2014: 3,000,000 Year ended 31 December 2015: 2,000,000 Year ended 31 December 2017: 1,750,000 Year ended 31 December 2018: nil *During the year ended 31 December 2018, the company sold a machine for 275,000 which acquired during the year ended 31 December 2015 for 400,000 (included in the 2,000,000 amount shown above). All of the other plant and machinery additions listed above continued to be in use at the end of the accounting period. Requirement: (a) Calculate the corporation tax liability of All Clothing Ltd for the year ended 31 December 2018. Provide workings to support your capital allowances calculation. Marks will be awarded for an appropriate layout of your computational work. (35 marks) (b) State the due dates for the payment of the corporation tax liability calculated at (a) and the amount payable. You should assume that All Clothing Ltd makes the lowest preliminary tax payment possible. (Note: All Clothing Ltd's corporation tax liability for the year ended 31 December 2017 was 20,000.) (5 marks) (c) Write a short note the directors of All Clothing Ltd explaining the general treatment of corporation tax trading loss relief. (Assume that All Clothing Ltd will never have any profits subject to tax at 25% or 33%.) (10 marks) QUESTION 1-ANSWER ALL SECTIONS (a) All Clothing Ltd is an Irish tax resident company which manufactures and sells a wide range of clothing. It commenced to trade in 1995 and makes up its accounts to 31 December each year. The Statement of Comprehensive Income of All Clothing Ltd for the year ended 31 December 2018 is set out below: Notes Revenue 9,000,000 Less: Cost of goods sold (5,750,000) Gross profit 3,250,000 Other income (1) 50,000 Distribution costs (2) (1,450,000) Administrative (3) (975,000) costs Finance costs (4) (200,000) Gain on sale of site (5) 20,000 Profit before tax 695,000 Notes (1) Other income comprises a dividend received from an Irish tax resident subsidiary of All Clothing Ltd. (2) Distribution expenses include the following: Depreciation on motor vehicles 40,000 Depreciation on plant and machinery 75,000 Profit on disposal of a machine (see note 6)* (10,000) Creation of a general provision for repairs to factory 200,000 The remaining distribution expenses are revenue in nature and were incurred wholly and exclusively for the purposes of the trade of All Clothing Ltd. (3) Administration costs include the following: Customer entertainment 75,000 Increase in specific provision for bad debts 20,000 Legal fees in relation to debt collection 5,500 Trade subscriptions 1,500 Installation of a new alarm system 6,000 Pension contributions 25,000 The opening pension contributions accrual as at 1 January 2018 was 5,000 and the closing pension contributions accrual as at 31 December 2018 was 7,000. The remaining administration expenses are revenue in nature and were incurred wholly and exclusively for the purposes of the trade of All Clothing Ltd. (4) The finance cost comprises interest payable in respect of the working capital facility which the company has with Bank of Ireland. (5) During the year, the company sold a very small portion of its site to a neighbouring business for 30,000. The original base cost of that portion of the site was 10,000. (6) The company has two large delivery vans which it acquired in 2014 for 150,000 each. The company has a significant amount of plant and machinery. The following qualifying expenditure for capital allowances purposes was incurred in the accounting periods listed below and all assets were brought into use on acquisition: . Year ended 31 December 2014: 3,000,000 Year ended 31 December 2015: 2,000,000 Year ended 31 December 2017: 1,750,000 Year ended 31 December 2018: nil *During the year ended 31 December 2018, the company sold a machine for 275,000 which acquired during the year ended 31 December 2015 for 400,000 (included in the 2,000,000 amount shown above). All of the other plant and machinery additions listed above continued to be in use at the end of the accounting period. Requirement: (a) Calculate the corporation tax liability of All Clothing Ltd for the year ended 31 December 2018. Provide workings to support your capital allowances calculation. Marks will be awarded for an appropriate layout of your computational work. (35 marks) (b) State the due dates for the payment of the corporation tax liability calculated at (a) and the amount payable. You should assume that All Clothing Ltd makes the lowest preliminary tax payment possible. (Note: All Clothing Ltd's corporation tax liability for the year ended 31 December 2017 was 20,000.) (5 marks) (c) Write a short note the directors of All Clothing Ltd explaining the general treatment of corporation tax trading loss relief. (Assume that All Clothing Ltd will never have any profits subject to tax at 25% or 33%.) (10 marks)