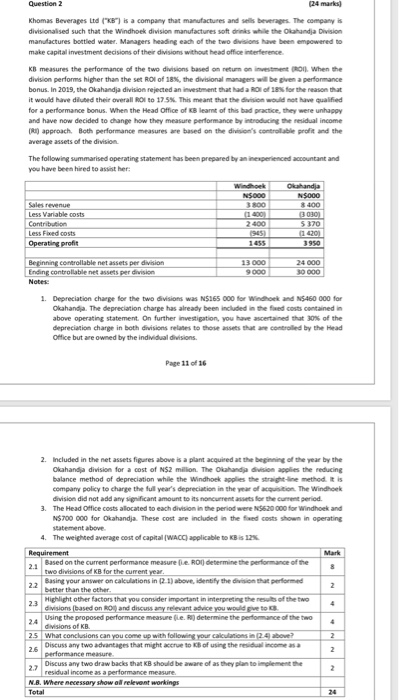

Question 2 (24 marks Khomas Beverages Ltd ("B") is a company that manufactures and sells beverages. The company is divisionalised such that the Windhoek division manufactures soft drinks while the Olahanda Division manufactures bottled water. Managers heading each of the two divisions have been empowered to make capital investment decisions of their divisions without head office interference. KB measures the performance of the two divisions based on return on investment Ron When the division performs higher than the set ROI of 18%, the divisional managers will be given a performance bonus. In 2019, the Okahandja division rejected an investment that had a Roof 12% for the reason that it would have diluted their overall Rol to 17.5%. This meant that the division would not have qualified for a performance bonus. When the Head Office of Bleart of this bad practice, they were unhappy and have now decided to change how they measure performance by introducing the residual income DR) approach. Both performance measures are based on the division's controllable profit and the average assets of the division The following summarised operating statement has been prepared by an inexperienced accountant and you have been hired to assist her: Windhoek Okahandja N5000 NS000 Sales revenue 3800 8400 Less Variable costs (1400 30303 Contribution 2400 5370 Less Fixed costs 1945) 14201 Operating profil 3950 Beginning controllable net assets per division 13 000 24 000 Ending controllable net assets per division 9000 30 000 Notes: 1. Depreciation charge for the two divisions was N$165 000 for Windhoek and N$460 000 for Okahandia. The depreciation charge has already been included in the feed costs contained in above operating statement. On further investigation, you have ascertained that 30% of the depreciation charge in both divisions relates to those assets that we controlled by the head Office but are owned by the individual divisions. Page 11 of 16 2. Included in the net assets figures above is a plant acquired at the beginning of the year by the Olahandija division for a cost of N$2 million. The Olahanda division applies the reducing balance method of depreciation while the Windhoek applies the straight-line method is company policy to change the full year's depreciation in the year of acquisition. The Windhoek division did not add any significant amount to its non current assets for the current period. 3. The Head Office costs allocated to each division in the period were 620 000 for Windhoek and N$ 700 000 for Okahandja. These cost are included in the feed costs shown in operating statement above. 4. The weighted average cost of capital (WACC) applicable to KBS 12% Requirement Mark 2.1 Based on the current performance measure le Roi determine the performance of the two divisions of KB for the current year. 8 2.2 Sasine your answer on calculations in (2:1) above, identify the courtsion that performed 2 23 Highlight other factors that you consider important in interpreting the role of the two Using the proposed performance measurele. Ru) determine the performance of the two 24 divisions of KB. 25 What conclusions can you come up with following your calculations in 24 above? 2 2.6 Discuss any two advantages that might accrue to of using the residual income as a performance measure 2.7 Discuss any two drawbacks that KB should be aware of as they plan to implement the residual income as a performance measure N.B. Where necessary show all relevant workings Total 4 2 Question 2 (24 marks Khomas Beverages Ltd ("B") is a company that manufactures and sells beverages. The company is divisionalised such that the Windhoek division manufactures soft drinks while the Olahanda Division manufactures bottled water. Managers heading each of the two divisions have been empowered to make capital investment decisions of their divisions without head office interference. KB measures the performance of the two divisions based on return on investment Ron When the division performs higher than the set ROI of 18%, the divisional managers will be given a performance bonus. In 2019, the Okahandja division rejected an investment that had a Roof 12% for the reason that it would have diluted their overall Rol to 17.5%. This meant that the division would not have qualified for a performance bonus. When the Head Office of Bleart of this bad practice, they were unhappy and have now decided to change how they measure performance by introducing the residual income DR) approach. Both performance measures are based on the division's controllable profit and the average assets of the division The following summarised operating statement has been prepared by an inexperienced accountant and you have been hired to assist her: Windhoek Okahandja N5000 NS000 Sales revenue 3800 8400 Less Variable costs (1400 30303 Contribution 2400 5370 Less Fixed costs 1945) 14201 Operating profil 3950 Beginning controllable net assets per division 13 000 24 000 Ending controllable net assets per division 9000 30 000 Notes: 1. Depreciation charge for the two divisions was N$165 000 for Windhoek and N$460 000 for Okahandia. The depreciation charge has already been included in the feed costs contained in above operating statement. On further investigation, you have ascertained that 30% of the depreciation charge in both divisions relates to those assets that we controlled by the head Office but are owned by the individual divisions. Page 11 of 16 2. Included in the net assets figures above is a plant acquired at the beginning of the year by the Olahandija division for a cost of N$2 million. The Olahanda division applies the reducing balance method of depreciation while the Windhoek applies the straight-line method is company policy to change the full year's depreciation in the year of acquisition. The Windhoek division did not add any significant amount to its non current assets for the current period. 3. The Head Office costs allocated to each division in the period were 620 000 for Windhoek and N$ 700 000 for Okahandja. These cost are included in the feed costs shown in operating statement above. 4. The weighted average cost of capital (WACC) applicable to KBS 12% Requirement Mark 2.1 Based on the current performance measure le Roi determine the performance of the two divisions of KB for the current year. 8 2.2 Sasine your answer on calculations in (2:1) above, identify the courtsion that performed 2 23 Highlight other factors that you consider important in interpreting the role of the two Using the proposed performance measurele. Ru) determine the performance of the two 24 divisions of KB. 25 What conclusions can you come up with following your calculations in 24 above? 2 2.6 Discuss any two advantages that might accrue to of using the residual income as a performance measure 2.7 Discuss any two drawbacks that KB should be aware of as they plan to implement the residual income as a performance measure N.B. Where necessary show all relevant workings Total 4 2