Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Question 2 4 Consider a GNMA mortgage pool with principal of $ 1 6 million. The maturity is 1 5 years with a monthly mortgage

Question

Consider a GNMA mortgage pool with principal of $ million. The maturity is years with

a monthly mortgage payment of percent per year. Assume no prepayments.

a What is the monthly mortgage payment percent amortizing on the pool of

mortgages? Do not round intermediate calculations. Round your answer to decimal

places. eg No Commas

s

b If the GNMA insurance fee is basis points and the servicing fee is basis points, what

is the yield on the GNMA passthrough? Do not round intermediate calculations. Round

your answer to decimal places. eg No Commas

c What is the monthly payment on the GNMA in part bDo not round intermediate

calculations. Round your answer to decimal places. eg No Commas

s

d Calculate the first monthly servicing fee paid to the originating FlsDo not round

intermediate calculations. Round your answer to the nearest dollar amount. No Commas

e Calculate the first monthly insurance fee paid to GNMA. Do not round intermediate

calculations. Round your answer to the nearest dollar amount. No Commas

S Question

A bank has a negative repricing gap using a sixmonth maturity bucket. Which one of the

following statements is most correct if MMDAs money market deposit accounts are rate

sensitive liabilities?

If all interest rates are projected to increase, to limit a profit decline when this occurs, the bank could

encourage its retail deposit customers to switch from twoyear CDs at current rates to MMDAs.

If all interest rates are projected to increase, to limit a profit decline when this occurs, the bank could

encourage its retail deposit customers to switch from twoyear CDs at current rates to threemonth

CDs

If all interest rates are projected to decrease, to limit a profit decline when this occurs, the bank could

encourage its retail deposit customers to switch from MMDAs to twoyear CDs at current rates.

If all interest rates are projected to increase, to limit a profit decline when this occurs, the bank could

encourage its retail deposit customers to switch from MMDAs to twoyear CDs at current rates.

If all interest rates are projected to decrease, to limit a profit decline when this occurs, the bank could

encourage its retail deposit customers to switch from threemonth CDs to twoyear CDs at current

rates. Question

A bank has a positive duration gap. Which one of the following statements is most correct?

If all interest rates are projected to increase, to limit a net value decline before rates rise, the bank

should increase shortterm loans and decrease longterm loans.

If all interest rates are projected to increase, to limit a net value decline before rates rise, the bank

should increase longterm loans and decrease shortterm loans.

If all interest rates are projected to decrease, to limit a net value decline before rates fall, the bank

should increase longterm bonds issued by the bank and decrease shortterm bonds.

If all interest rates are projected to decrease, to limit a net value decline before rates fall, the bank

should increase longterm loans and decrease shortterm loans.

None of the options are correct.Question

A bank has a negative duration gap. Interest rates decline. Which one of the following best

describes the effects of the interest rate change?

The bank's market value of equity goes up because the market value of its assets goes up by more

than the market value of its liabilities goes down.

The bank's market value of equity goes down because the market value of its assets goes up by

more than the market value of its liabilities goes down.

The bank's market value of equity goes down because the market value of its liabilities increases by

more than the market value of its assets increases.

The bank's market value of equity is unchanged since the market value of its assets and liabilities

moves in the same direction.

The bank's market value of equity goes down because the market value of its assets goes down by

more than the market value of its liabilities goes down.Question

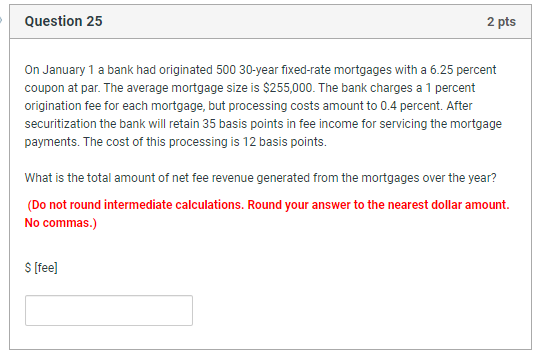

On January a bank had originated year fixedrate mortgages with a percent

coupon at par. The average mortgage size is $ The bank charges a percent

origination fee for each mortgage, but processing costs amount to percent. After

securitization the bank will retain basis points in fee income for servicing the mortgage

payments. The cost of this processing is basis points.

What is the total amount of net fee revenue generated from the mortgages over the year?

Do not round intermediate calculations. Round your answer to the nearest dollar amount.

No commas.

$ fee

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cases In Healthcare Finance

Authors: George H. Pink, Paula H. Song

7th Edition

1640553177, 978-1640553170