Answered step by step

Verified Expert Solution

Question

1 Approved Answer

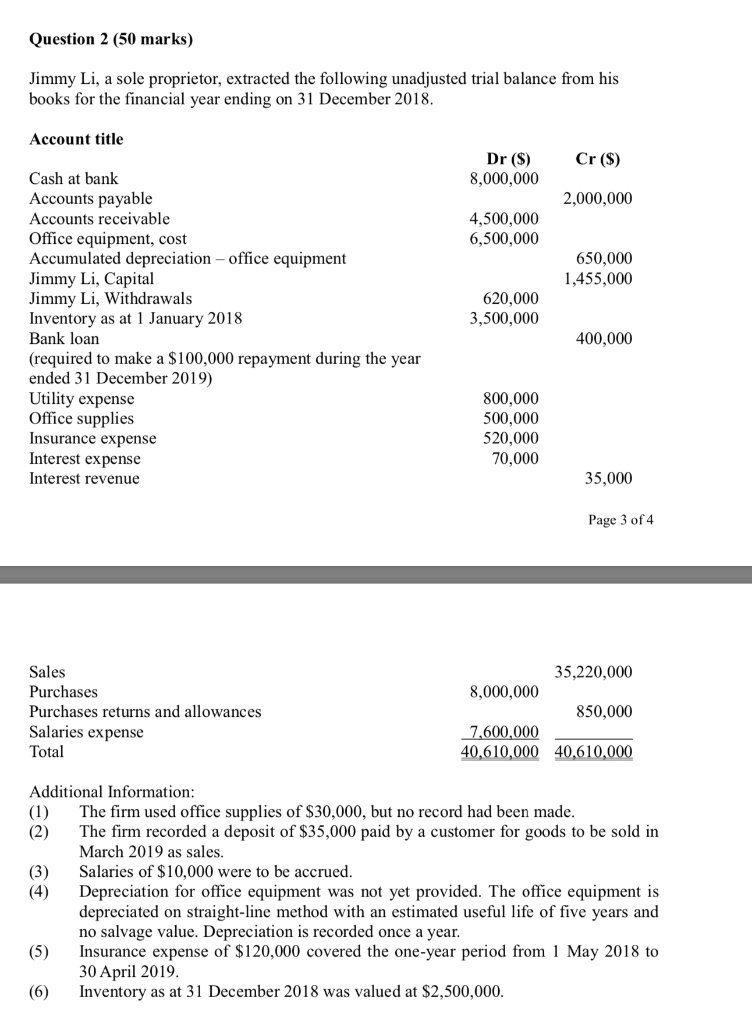

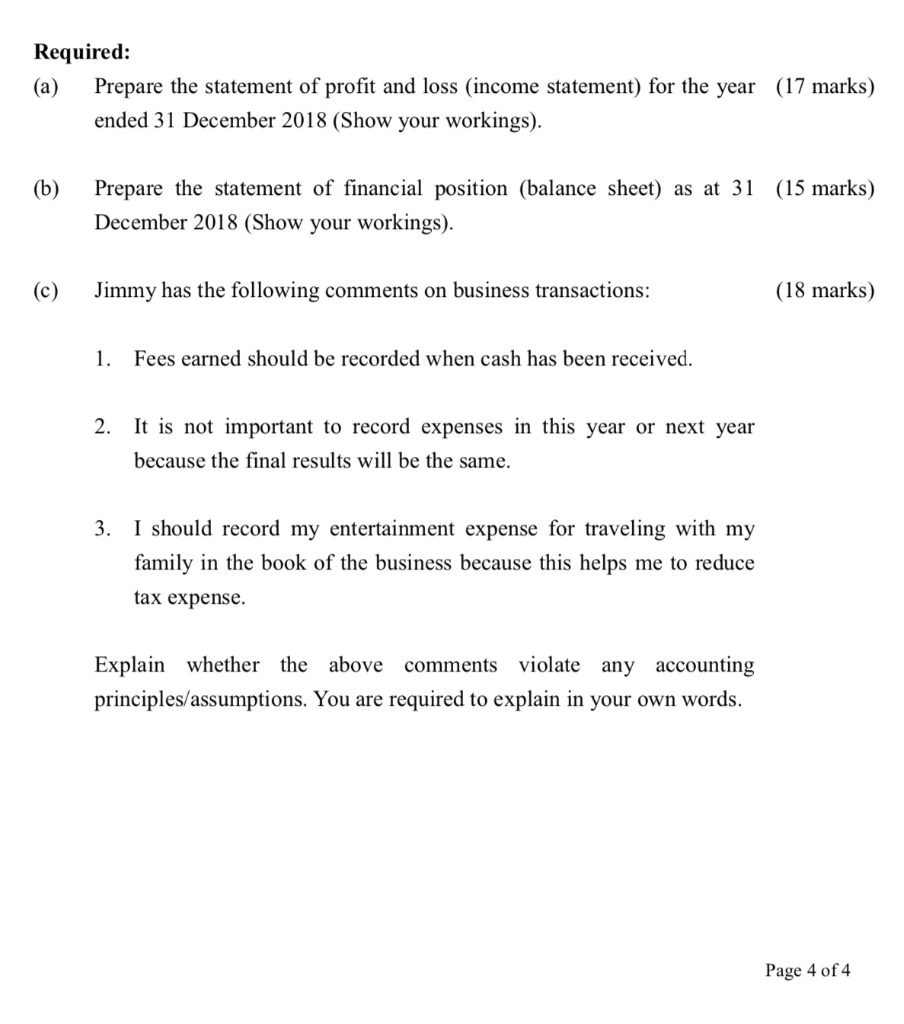

Question 2 (50 marks) Jimmy Li, a sole proprietor, extracted the following unadjusted trial balance from his books for the financial year ending on 31

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audits Of Public Companies Continued Concentration In Audit Market For Large Public Companies Does Not Call For Immediate Action

Authors: United States Government Accountability

1st Edition

1297008111, 978-1297008115