Answered step by step

Verified Expert Solution

Question

1 Approved Answer

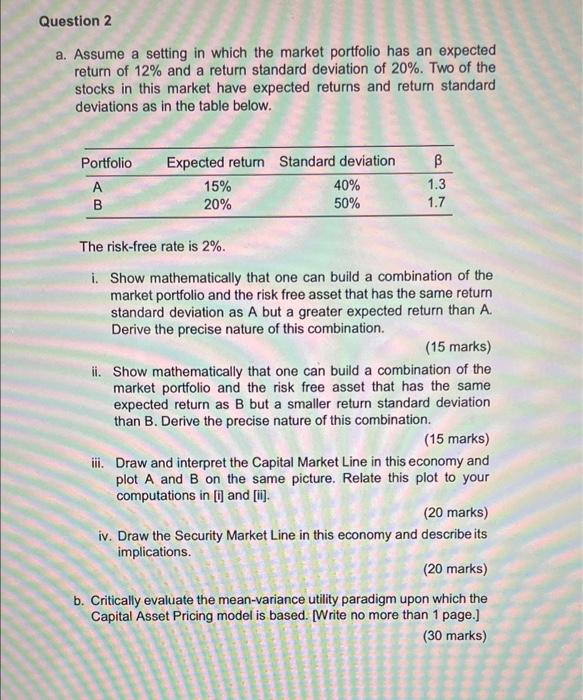

Question 2 a. Assume a setting in which the market portfolio has an expected return of 12% and a return standard deviation of 20%. Two

Question 2 a. Assume a setting in which the market portfolio has an expected return of 12% and a return standard deviation of 20%. Two of the stocks in this market have expected returns and return standard deviations as in the table below. Portfolio Expected return Standard deviation A 40% 1.3 15% 20% B 50% 1.7 The risk-free rate is 2%. i. Show mathematically that one can build a combination of the market portfolio and the risk free asset that has the same return standard deviation as A but a greater expected return than A. Derive the precise nature of this combination. (15 marks) ii. Show mathematically that one can build a combination of the market portfolio and the risk free asset that has the same expected return as B but a smaller return standard deviation than B. Derive the precise nature of this combination. (15 marks) iii. Draw and interpret the Capital Market Line in this economy and plot A and B on the same picture. Relate this plot to your computations in [i] and [ii]. (20 marks) iv. Draw the Security Market Line in this economy and describe its implications. (20 marks) b. Critically evaluate the mean-variance utility paradigm upon which the Capital Asset Pricing model is based. [Write no more than 1 page.] (30 marks) www Question 2 a. Assume a setting in which the market portfolio has an expected return of 12% and a return standard deviation of 20%. Two of the stocks in this market have expected returns and return standard deviations as in the table below. Portfolio Expected return Standard deviation A 40% 1.3 15% 20% B 50% 1.7 The risk-free rate is 2%. i. Show mathematically that one can build a combination of the market portfolio and the risk free asset that has the same return standard deviation as A but a greater expected return than A. Derive the precise nature of this combination. (15 marks) ii. Show mathematically that one can build a combination of the market portfolio and the risk free asset that has the same expected return as B but a smaller return standard deviation than B. Derive the precise nature of this combination. (15 marks) iii. Draw and interpret the Capital Market Line in this economy and plot A and B on the same picture. Relate this plot to your computations in [i] and [ii]. (20 marks) iv. Draw the Security Market Line in this economy and describe its implications. (20 marks) b. Critically evaluate the mean-variance utility paradigm upon which the Capital Asset Pricing model is based. [Write no more than 1 page.] (30 marks) www

Question 2 a. Assume a setting in which the market portfolio has an expected return of 12% and a return standard deviation of 20%. Two of the stocks in this market have expected returns and return standard deviations as in the table below. Portfolio Expected return Standard deviation A 40% 1.3 15% 20% B 50% 1.7 The risk-free rate is 2%. i. Show mathematically that one can build a combination of the market portfolio and the risk free asset that has the same return standard deviation as A but a greater expected return than A. Derive the precise nature of this combination. (15 marks) ii. Show mathematically that one can build a combination of the market portfolio and the risk free asset that has the same expected return as B but a smaller return standard deviation than B. Derive the precise nature of this combination. (15 marks) iii. Draw and interpret the Capital Market Line in this economy and plot A and B on the same picture. Relate this plot to your computations in [i] and [ii]. (20 marks) iv. Draw the Security Market Line in this economy and describe its implications. (20 marks) b. Critically evaluate the mean-variance utility paradigm upon which the Capital Asset Pricing model is based. [Write no more than 1 page.] (30 marks) www Question 2 a. Assume a setting in which the market portfolio has an expected return of 12% and a return standard deviation of 20%. Two of the stocks in this market have expected returns and return standard deviations as in the table below. Portfolio Expected return Standard deviation A 40% 1.3 15% 20% B 50% 1.7 The risk-free rate is 2%. i. Show mathematically that one can build a combination of the market portfolio and the risk free asset that has the same return standard deviation as A but a greater expected return than A. Derive the precise nature of this combination. (15 marks) ii. Show mathematically that one can build a combination of the market portfolio and the risk free asset that has the same expected return as B but a smaller return standard deviation than B. Derive the precise nature of this combination. (15 marks) iii. Draw and interpret the Capital Market Line in this economy and plot A and B on the same picture. Relate this plot to your computations in [i] and [ii]. (20 marks) iv. Draw the Security Market Line in this economy and describe its implications. (20 marks) b. Critically evaluate the mean-variance utility paradigm upon which the Capital Asset Pricing model is based. [Write no more than 1 page.] (30 marks) www

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started