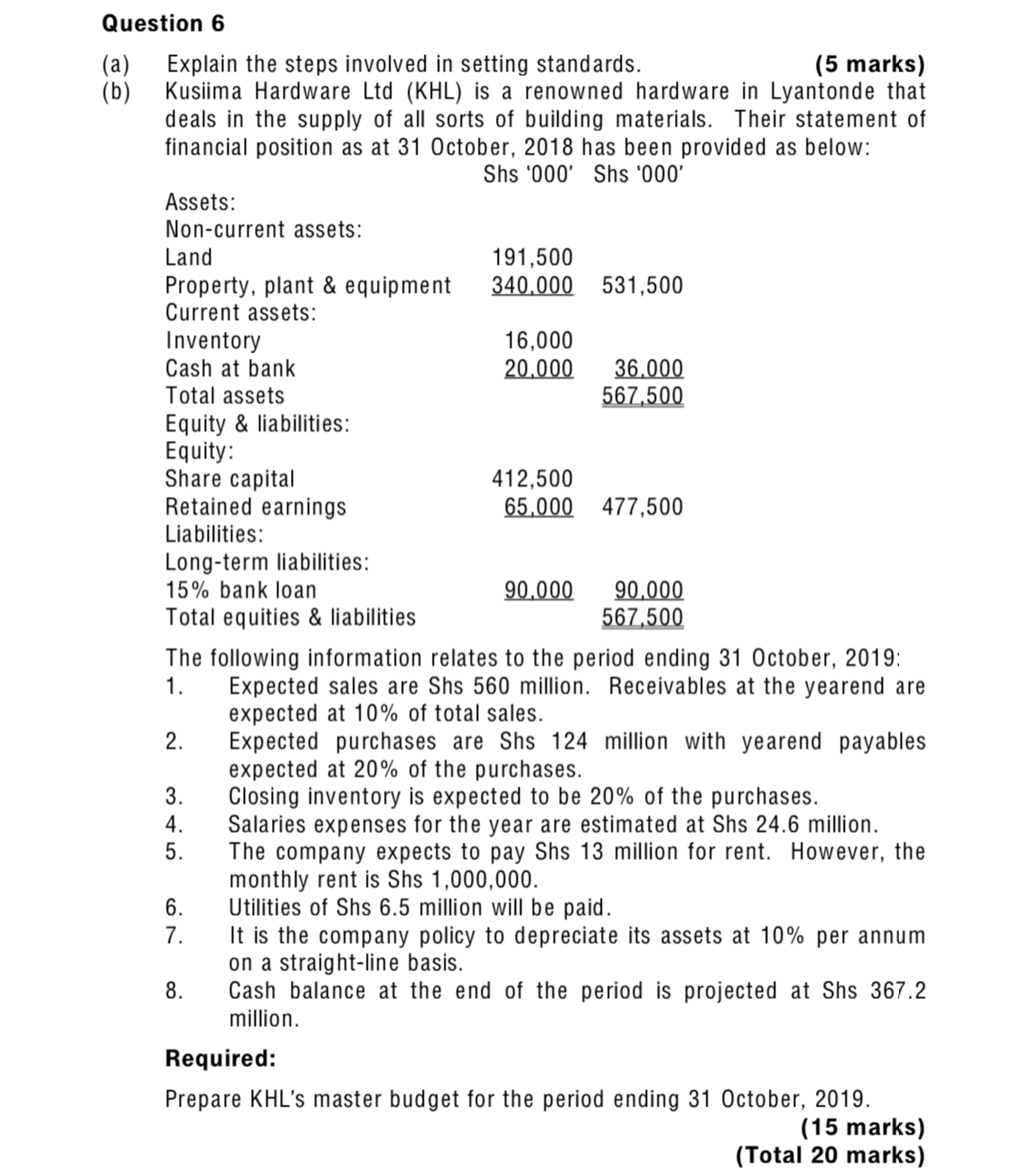

Question 2 (a) Distinguish between the following terms: (i) sunk costs and opportunity costs. (ii) periodic and perpetual inventory systems. (b) Rukundo Enterprises deals in the production of milk related products. Their purchases and issues of raw materials for the month of October 2018 were as follows: Raw material inventory as at 30 September, 2018 was 4,000 litres valued at Shs 2,500 per litre. Required: Using first in first out method determine the value of inventory as at 31 October, 2018. (10 marks) (c) Rukundo Enterprises employs four sales agents who earn a basic weekly allowance of Shs 50,000 and a sales commission that differs depending on the quantity sold. For one of its main products yogurt, the monthly sales commission structure has been provided as follows: Sachets sold 0 - 40,000 40,001 - 50,000 Above 50,000 Rate per sachet (Shs) 10 25 50 During the month of October 2018 the following sales were made by the respective salesmen. (2 marks) (2 marks) Name Alex Bob Andrew Ahmed Sachets sold 48,000 55,000 38,000 50,000

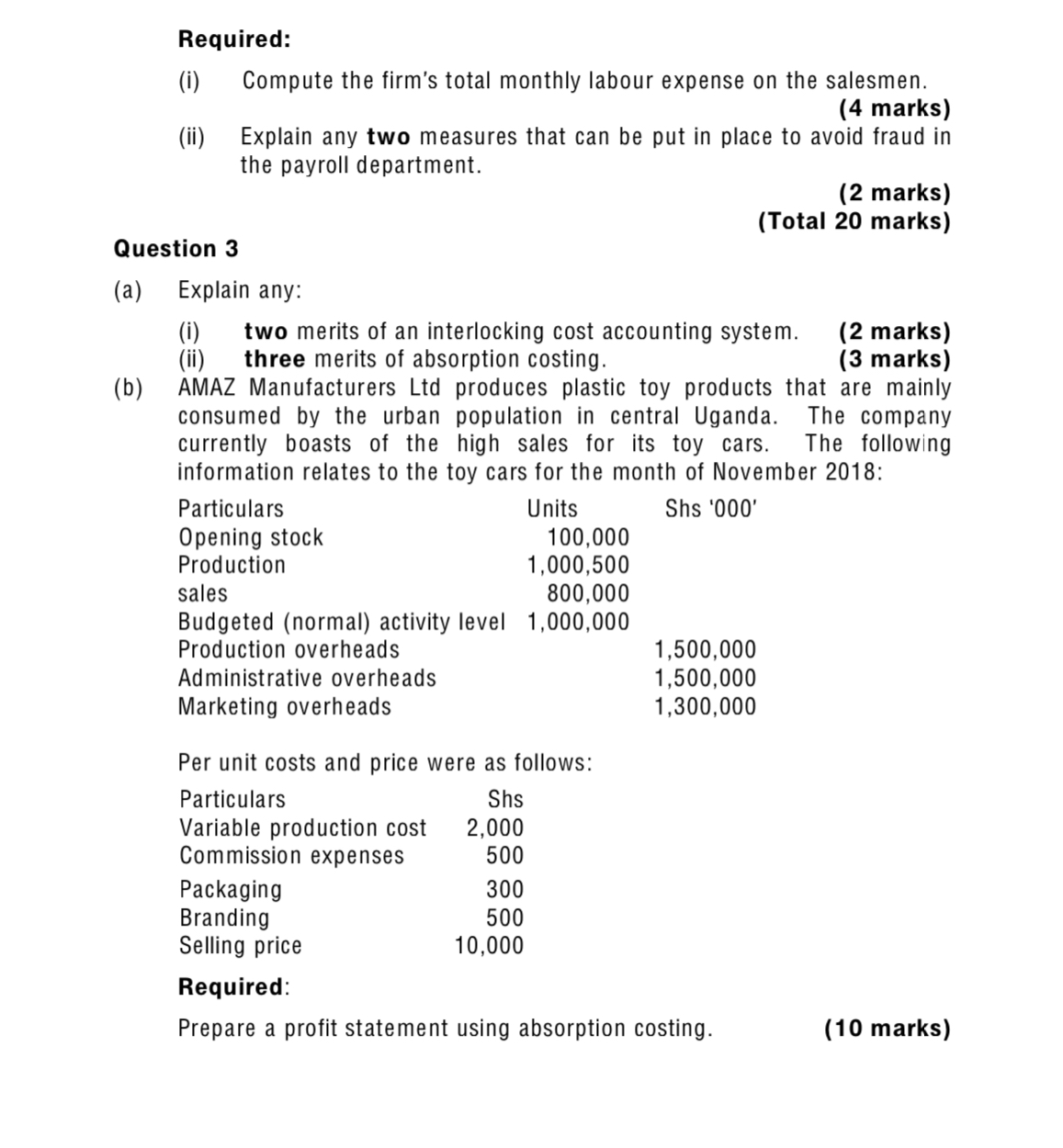

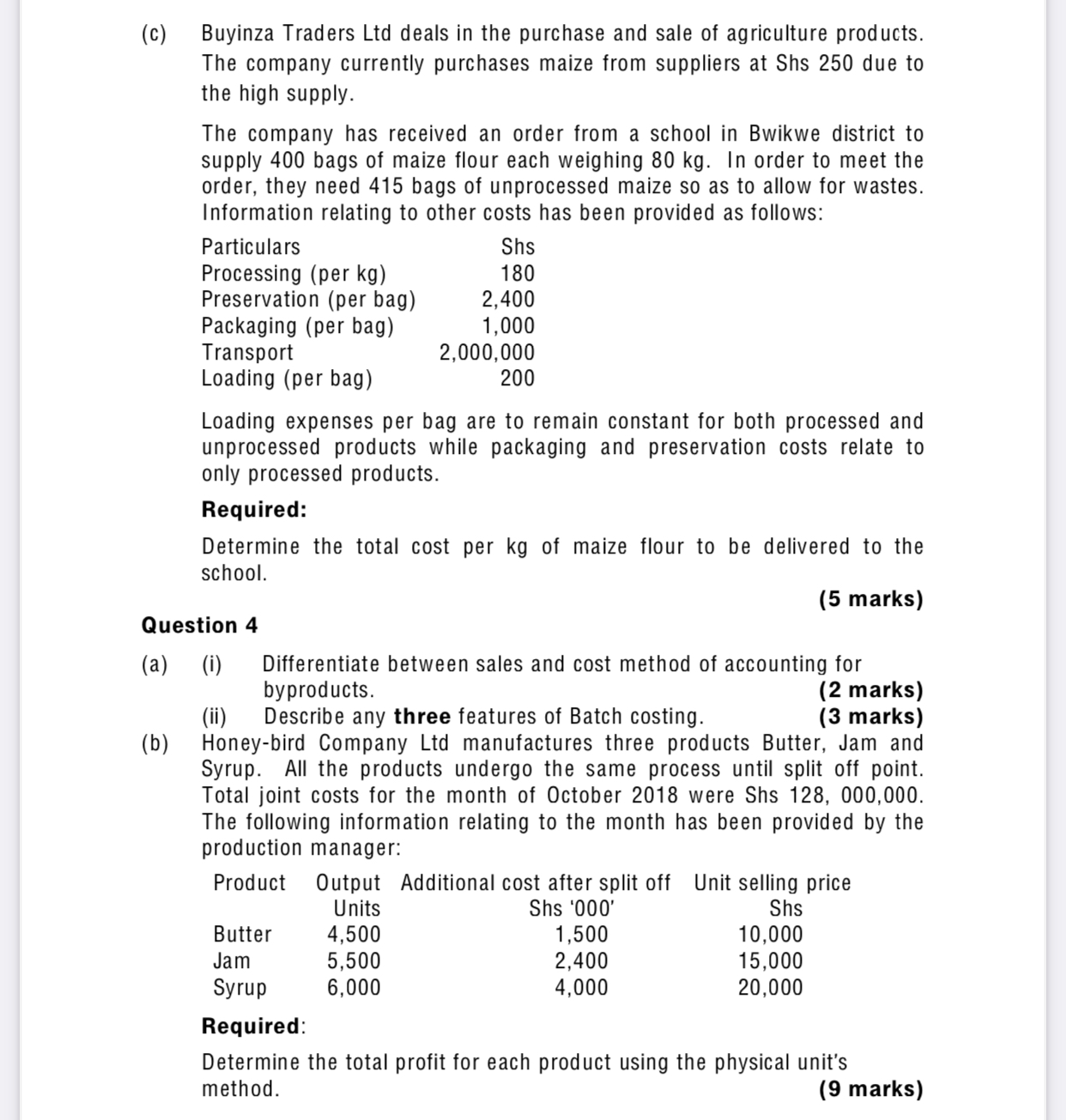

Required: (i) Compute the firm's total monthly labour expense on the salesmen. (4 marks) (ii) Explain any two measures that can be put in place to avoid fraud in the payroll department. (2 marks) (Total 20 marks) Question 3 (a) ('3) Explain any: (i) two merits of an interlocking cost accounting system. (2 marks) (ii) three merits of absorption costing. (3 marks) AMAZ Manufacturers Ltd produces plastic toy products that are mainly consumed by the urban population in central Uganda. The company currently boasts of the high sales for its toy cars. The following information relates to the toy cars for the month of November 2018: Particulars Units Shs '000' Opening stock 100,000 Production 1.000.500 sales 800.000 Budgeted (normal) activity level 1.000.000 Production overheads 1,500.000 Administrative overheads 1,500.000 Marketing overheads 1.300.000 Per unit costs and price were as follows: Particulars Shs Variable production cost 2,000 Commission expenses 500 Packaging 300 Branding 500 Selling price 10.000 Required: Prepare a profit statement using absorption costing. (10 marks) (G) Buyinza Traders Ltd deals in the purchase and sale of agriculture products. The company currently purchases maize from suppliers at Shs 250 due to the high supply. The company has received an order from a school in Bwikwe district to supply 400 bags of maize flour each weighing 80 kg. In order to meet the order. they need 415 bags of unprocessed maize so as to allow for wastes. Information relating to other costs has been provided as TOIIOWSI Particulars Shs Processing (per kg) 180 Preservation (per bag) 2,400 Packaging (per bag) 1.000 Transport 2.000.000 Loading (per bag) 200 Loading expenses per bag are to remain constant for both processed and unprocessed products while packaging and preservation costs relate to only processed products. Required: Determine the total cost per kg of maize flour to be delivered to the school. (5 marks) Question 4 (a) (i) Differentiate between sales and cost method of accounting for byproducts. (2 marks) (ii) Describe any three features of Batch costing. (3 marks) ('3) Honey-bird Company Ltd manufactures three products Butter. Jam and Syrup. All the products undergo the same process until split off point. Total ioint costs for the month of October 2018 were Shs 128. 000.000. The following information relating to the month has been provided by the production manager: Product Output Additional cost after split off Unit selling price Units Shs '000' Shs Butter 4.500 1.500 10.000 Jam 5.500 2.400 15.000 Syrup 6.000 4.000 20.000 Required: Determine the total profit for each product using the physical unit's method. (9 marks) Nsanziiro Carpentry Workshop deals in the production and sale of different types of furniture to different customers based on customer specifications. The workshop has received an order to supply 300 desks from Salaama Secondary school. Information regarding the expected costs for the order has been provided as follows: Direct materials: Quantity Unit price (Shs) Timber (metres) 500 30.000 Nails (kg) 600 5.000 Vanish (litres) 40 15.000 Direct labour (hours): Department A 300 6.500 Department B 150 3.500 Variable overheads (per direct hour): DepartmentA 1.500 Department B 2.000 Fixed overheads are expected to be Shs 1.200.000. Required: Determine the price of each desk if the firm targets a profit of 20% on cost. (6 marks) (Total 20 marks) Question 5 (a) (i) Distinguish between the terms 'angle of incidence' and 'margin of safety' as used in cost-volume-profit analysis (2 marks) (ii) Explain any three merits of activity-based costing. (3 marks) (b) Fizzy Textiles Uganda Ltd (FTUL) is a renowned textiles plant in Jinja producing bed sheets. FTUL is looking for ways of cutting down costs of running the business. It's weighing options of outsourcing the production or continues making the bed sheets internally. Laala Salaama Textiles Ltd (LSTL) in Busia has offered to supply 1.000.000 pairs of Nile Bedsheets to the FTUL on a monthly basis at a cost of Shs 45.000 per pair. FTUL currently incurs the following costs on a monthly basis: Particulars Shs'000' Direct materials 3.000.000 Direct labour 3.500.000 Variable production overheads 4.750.000 Quality inspection overheads 5.000.000 Equipment servicing overheads 6.500.000 Fixed production overheads 5.500.000 Supervisory overheads 11,250,000 (c) FTUL produces and sells 1,000,000 pairs of bed sheets monthly. If a decision is taken to buy from LSTL, FTUL will save all variable production overheads. Equipment servicing overheads and fixed production overheads will be saved by 95%, supervisory overheads will be saved by 50% while quality inspection overheads will still be incurred in full. There will not be any other opportunity costs as a result of making a make or buy decision. Required: With appropriate computations, advise the company on whether to buy from the supplier or continue making the bedsheets. (9 marks) Footseps Furniture Limited deals in the production and sale of furniture products. The company runs three independent branches and the performance for each of the branches for the quarter ending 31 October, 2018 is provided below: Branches Kampala Kawempe Mukono Total Shs'000' Shs'000' Shs'000' Shs'000' Sales 45,000 54,000 48,000 147,000 Variable costs: Direct materials (15,000) (30,000) (22,000) (67,000) Direct labour (7,000) (11,000) (8,000) (26,000) Variable overheads 5,000) 30001 [10001 (12,000] Contribution 18,000 4,000 15,000 37,000 Fixed overheads L5.._1.0.0.1 (5.3.0.0.). L5...0_0_0.l (16.5.03). Profit! (IOSS) M M M M Management is concerned about the poor performance of Kawempe branch and is considering closing it so as to concentrate on the two profitable ones. Closing Kawempe branch will lead to a saving of Shs 1, 800,000 of the fixed overheads since they are directly attributable to the branch Required: Advise management on whether they should close Kawempe branch. (6 marks) (Total 20 marks) Question 6 (a) Explain the steps involved in setting standards. (5 marks) (b) Kusiima Hardware Lid (KHL) is a renowned hardware in Lyantonde that deals in the supply of all sorts of building materials. Their statement of financial position as at 31 October, 2018 has been provided as below: Shs '000' Shs '000' Assets: Non-current assets: Land 191,500 Property, plant & equipment 340,000 531,500 Current assets: Inventory 16,000 Cash at bank 20,000 36,000 Total assets 567.500 Equity & liabilities: Equity: Share capital 412,500 Retained earnings 65,000 477,500 Liabilities Long-term liabilities: 15% bank loan 90,000 90,000 Total equities & liabilities 567,500 The following information relates to the period ending 31 October, 2019: 1 . Expected sales are Shs 560 million. Receivables at the yearend are expected at 10% of total sales. 2. Expected purchases are Shs 124 million with yearend payables expected at 20% of the purchases. 3. Closing inventory is expected to be 20% of the purchases. 4. Salaries expenses for the year are estimated at Shs 24.6 million. 5 . The company expects to pay Shs 13 million for rent. However, the monthly rent is Shs 1,000,000. 6. Utilities of Shs 6.5 million will be paid. 7 . It is the company policy to depreciate its assets at 10% per annum on a straight-line basis. 8. Cash balance at the end of the period is projected at Shs 367.2 million. Required: Prepare KHL's master budget for the period ending 31 October, 2019. (15 marks) (Total 20 marks)