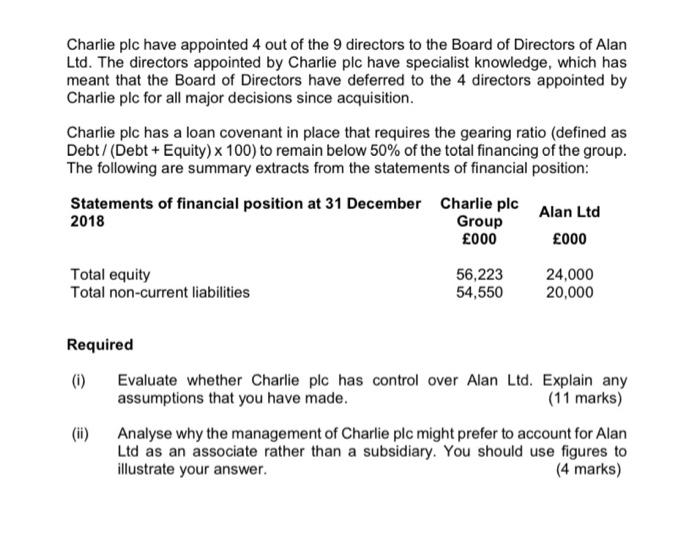

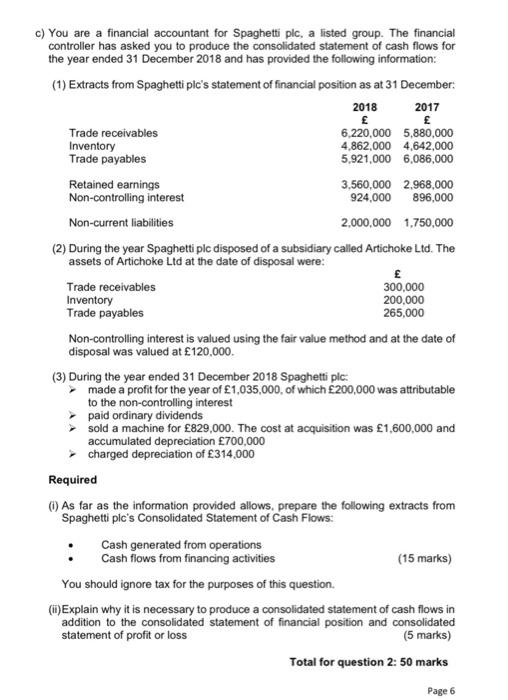

Question 2 a) Young plc owns a number of subsidiary companies. During the year Young ple has undertaken the following transactions which have not yet been accounted for in full (1) On 1 July 2018 Young pic purchased 40% of Daquiti Lid's ordinary shares for a cash payment of 350,000. This investment gave Young plc significant influence over Daquiri Ltd. Daquiri Lid made a profit of 126,000 for the year ended 31 December 2018, The only accounting entries that have been posted are debit investments in the statement of financial position and credit bank. Young pic has not yet accounted for any further entries in relation to Daquiri Ltd in its consolidated financial statements (2) On 1 August 2018 Young plc disposed of a subsidiary company, Singapore Ltd, in which it held a 70% ownership. The only accounting entries that have been posted are debit bank and credit investments in the statement of financial position. The directors of Young plc are unsure how to account for a disposal of a subsidiary company in either the individual company accounts or the consolidated financial statements. (3) On 1 January 2018 Young purchased 70% of Star GmbH (a company operating in Germany). The directors of young ple are unsure how to account for the investment in Star GmbH. The only accounting entries that have been made in relation to this acquisition are debit investments in the statement of financial position and credit bank. In particular the directors of Young plc do not know how to account for: Statement of profit or loss items Statement of financial position items Goodwill Required Explain the required IFRS financial reporting treatment of (1) to (3) above in relation to the consolidated financial statements of Young plc for the year ended 31 December 2018. Include all relevant calculations. You should also explain why the Specific treatment you identity is appropriate (15 marks) b) On 1 January 2018 Charlie plo acquired 40% of the ordinary share capital of Alan Lid. As part of the purchase agreement, the management of Alan Lid will continue to have responsibility for the day to day running of Alan Lid. However all major investing and financing activities of Alan Lid require agreement from Charlie plc. Additionally. Charlie pic was granted an option to purchase a further 20% of the share capital of Alan Lid at a price of 2 per share on 30 June 2019. The current market price of the shares in Alan Ltd is 3. Page 4 Charlie plc have appointed 4 out of the 9 directors to the Board of Directors of Alan Lid. The directors appointed by Charlie plc have specialist knowledge, which has meant that the Board of Directors have deferred to the 4 directors appointed by Charlie pic for all major decisions since acquisition Charlie plc have appointed 4 out of the 9 directors to the Board of Directors of Alan Ltd. The directors appointed by Charlie plc have specialist knowledge, which has meant that the Board of Directors have deferred to the 4 directors appointed by Charlie plc for all major decisions since acquisition. Charlie plc has a loan covenant in place that requires the gearing ratio (defined as Debt / (Debt + Equity) x 100) to remain below 50% of the total financing of the group. The following are summary extracts from the statements of financial position: Statements of financial position at 31 December Charlie plc 2018 Alan Ltd Group 000 000 Total equity Total non-current liabilities 56,223 54,550 24,000 20,000 Required (1) Evaluate whether Charlie plc has control over Alan Ltd. Explain any assumptions that you have made. (11 marks) Analyse why the management of Charlie plc might prefer to account for Alan Ltd as an associate rather than a subsidiary. You should use figures to illustrate your answer. (4 marks) c) You are a financial accountant for Spaghetti plc, a listed group. The financial controller has asked you to produce the consolidated statement of cash flows for the year ended 31 December 2018 and has provided the following information: (1) Extracts from Spaghetti plc's statement of financial position as at 31 December: 2018 2017 Trade receivables 6,220,000 5,880,000 Inventory 4,862,000 4,642,000 Trade payables 5.921,000 6,086,000 Retained earnings 3,560,000 2,968,000 Non-controlling interest 924,000 896,000 Non-current liabilities 2,000,000 1,750,000 (2) During the year Spaghetti plc disposed of a subsidiary called Artichoke Ltd. The assets of Artichoke Ltd at the date of disposal were: Trade receivables 300,000 Inventory 200,000 Trade payables 265,000 Non-controlling interest is valued using the fair value method and at the date of disposal was valued at 120,000. (3) During the year ended 31 December 2018 Spaghetti pic: made a profit for the year of 1,035,000, of which 200,000 was attributable to the non-controlling interest paid ordinary dividends sold a machine for 829,000. The cost at acquisition was 1,600,000 and accumulated depreciation 700,000 charged depreciation of 314,000 Required As far as the information provided allows, prepare the following extracts from Spaghetti ple's Consolidated Statement of Cash Flows: Cash generated from operations Cash flows from financing activities (15 marks) You should ignore tax for the purposes of this question. (1) Explain why it is necessary to produce a consolidated statement of cash flows in addition to the consolidated statement of financial position and consolidated statement of profit or loss (5 marks) Total for question 2: 50 marks Page 6 Question 2 a) Young plc owns a number of subsidiary companies. During the year Young ple has undertaken the following transactions which have not yet been accounted for in full (1) On 1 July 2018 Young pic purchased 40% of Daquiti Lid's ordinary shares for a cash payment of 350,000. This investment gave Young plc significant influence over Daquiri Ltd. Daquiri Lid made a profit of 126,000 for the year ended 31 December 2018, The only accounting entries that have been posted are debit investments in the statement of financial position and credit bank. Young pic has not yet accounted for any further entries in relation to Daquiri Ltd in its consolidated financial statements (2) On 1 August 2018 Young plc disposed of a subsidiary company, Singapore Ltd, in which it held a 70% ownership. The only accounting entries that have been posted are debit bank and credit investments in the statement of financial position. The directors of Young plc are unsure how to account for a disposal of a subsidiary company in either the individual company accounts or the consolidated financial statements. (3) On 1 January 2018 Young purchased 70% of Star GmbH (a company operating in Germany). The directors of young ple are unsure how to account for the investment in Star GmbH. The only accounting entries that have been made in relation to this acquisition are debit investments in the statement of financial position and credit bank. In particular the directors of Young plc do not know how to account for: Statement of profit or loss items Statement of financial position items Goodwill Required Explain the required IFRS financial reporting treatment of (1) to (3) above in relation to the consolidated financial statements of Young plc for the year ended 31 December 2018. Include all relevant calculations. You should also explain why the Specific treatment you identity is appropriate (15 marks) b) On 1 January 2018 Charlie plo acquired 40% of the ordinary share capital of Alan Lid. As part of the purchase agreement, the management of Alan Lid will continue to have responsibility for the day to day running of Alan Lid. However all major investing and financing activities of Alan Lid require agreement from Charlie plc. Additionally. Charlie pic was granted an option to purchase a further 20% of the share capital of Alan Lid at a price of 2 per share on 30 June 2019. The current market price of the shares in Alan Ltd is 3. Page 4 Charlie plc have appointed 4 out of the 9 directors to the Board of Directors of Alan Lid. The directors appointed by Charlie plc have specialist knowledge, which has meant that the Board of Directors have deferred to the 4 directors appointed by Charlie pic for all major decisions since acquisition Charlie plc have appointed 4 out of the 9 directors to the Board of Directors of Alan Ltd. The directors appointed by Charlie plc have specialist knowledge, which has meant that the Board of Directors have deferred to the 4 directors appointed by Charlie plc for all major decisions since acquisition. Charlie plc has a loan covenant in place that requires the gearing ratio (defined as Debt / (Debt + Equity) x 100) to remain below 50% of the total financing of the group. The following are summary extracts from the statements of financial position: Statements of financial position at 31 December Charlie plc 2018 Alan Ltd Group 000 000 Total equity Total non-current liabilities 56,223 54,550 24,000 20,000 Required (1) Evaluate whether Charlie plc has control over Alan Ltd. Explain any assumptions that you have made. (11 marks) Analyse why the management of Charlie plc might prefer to account for Alan Ltd as an associate rather than a subsidiary. You should use figures to illustrate your answer. (4 marks) c) You are a financial accountant for Spaghetti plc, a listed group. The financial controller has asked you to produce the consolidated statement of cash flows for the year ended 31 December 2018 and has provided the following information: (1) Extracts from Spaghetti plc's statement of financial position as at 31 December: 2018 2017 Trade receivables 6,220,000 5,880,000 Inventory 4,862,000 4,642,000 Trade payables 5.921,000 6,086,000 Retained earnings 3,560,000 2,968,000 Non-controlling interest 924,000 896,000 Non-current liabilities 2,000,000 1,750,000 (2) During the year Spaghetti plc disposed of a subsidiary called Artichoke Ltd. The assets of Artichoke Ltd at the date of disposal were: Trade receivables 300,000 Inventory 200,000 Trade payables 265,000 Non-controlling interest is valued using the fair value method and at the date of disposal was valued at 120,000. (3) During the year ended 31 December 2018 Spaghetti pic: made a profit for the year of 1,035,000, of which 200,000 was attributable to the non-controlling interest paid ordinary dividends sold a machine for 829,000. The cost at acquisition was 1,600,000 and accumulated depreciation 700,000 charged depreciation of 314,000 Required As far as the information provided allows, prepare the following extracts from Spaghetti ple's Consolidated Statement of Cash Flows: Cash generated from operations Cash flows from financing activities (15 marks) You should ignore tax for the purposes of this question. (1) Explain why it is necessary to produce a consolidated statement of cash flows in addition to the consolidated statement of financial position and consolidated statement of profit or loss (5 marks) Total for question 2: 50 marks Page 6