Answered step by step

Verified Expert Solution

Question

1 Approved Answer

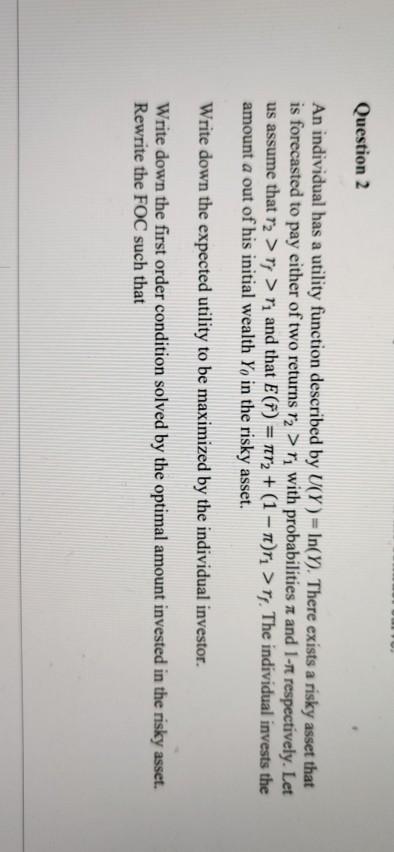

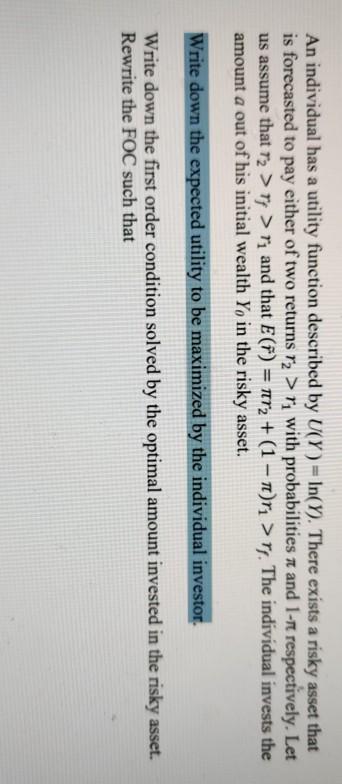

Question 2 An individual has a utility function described by U(Y) = In(Y). There exists a risky asset that is forecasted to pay either of

Question 2 An individual has a utility function described by U(Y) = In(Y). There exists a risky asset that is forecasted to pay either of two returns r2 >r with probabilities n and 1-nt respectively. Let us assume that r2 > >r, and that Ef) = nr2 + (1 - Tr > The individual invests the amount a out of his initial wealth Yo in the risky asset. Write down the expected utility to be maximized by the individual investor. Write down the first order condition solved by the optimal amount invested in the risky asset. Rewrite the FOC such that An individual has a utility function described by U(Y) = In(Y). There exists a risky asset that is forecasted to pay either of two returns r2 >r with probabilities i and 1-rt respectively. Let us assume that 72 >ry >r and that E(F) = nr2 + (1 - i)ri > The individual invests the amount a out of his initial wealth Yo in the risky asset. Write down the expected utility to be maximized by the individual investor. Write down the first order condition solved by the optimal amount invested in the risky asset. Rewrite the FOC such that Question 2 An individual has a utility function described by U(Y) = In(Y). There exists a risky asset that is forecasted to pay either of two returns r2 >r with probabilities n and 1-nt respectively. Let us assume that r2 > >r, and that Ef) = nr2 + (1 - Tr > The individual invests the amount a out of his initial wealth Yo in the risky asset. Write down the expected utility to be maximized by the individual investor. Write down the first order condition solved by the optimal amount invested in the risky asset. Rewrite the FOC such that An individual has a utility function described by U(Y) = In(Y). There exists a risky asset that is forecasted to pay either of two returns r2 >r with probabilities i and 1-rt respectively. Let us assume that 72 >ry >r and that E(F) = nr2 + (1 - i)ri > The individual invests the amount a out of his initial wealth Yo in the risky asset. Write down the expected utility to be maximized by the individual investor. Write down the first order condition solved by the optimal amount invested in the risky asset. Rewrite the FOC such that

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Principles And Applications

Authors: J William Petty, Sheridan Titman, Arthur J Keown, John D Martin, Peter Martin, Michael Burrow, Hoa Nguyen

6th Edition

1442539178, 9781442539174