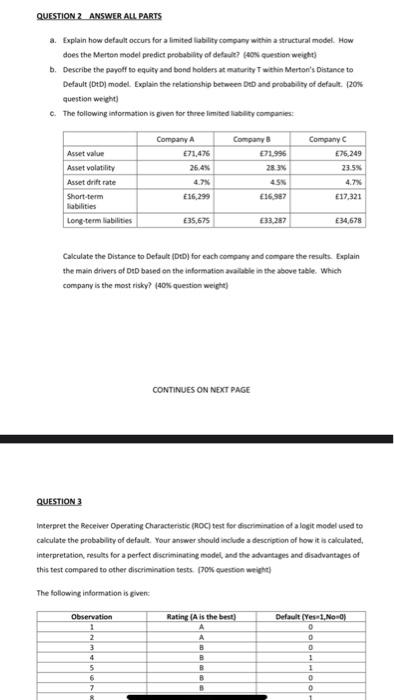

QUESTION 2 ANSWER ALL PARTS a. Explain how default occurs for a limited liability company within a structural model. How does the Merton model predict probability of default? (0 question weight b. Describe the payoff to equity and bond holders at maturity within Merton's Distance to Default (DD) model. Explain the relationship between DD and probability of default 20% question weight c. The following information is given for three limited liability companies Company E71,470 26.4% 4. E16,299 Company E71.996 283 Company 76,249 235 Asset value Asset volatility Asset drift rate Short-term labilities Long-term abilities 4SN 4.7% E17,321 E16.987 E35,675 33.282 E34.678 Calculate the Distance to Default (DD) for each company and compare the results. Explain the main drivers of DD based on the information available in the above table. Which company is the most risky? (40% question weight CONTINUES ON NEXT PAGE QUESTION Interpret the Receiver Operating Characteristic (ROC) test for discrimination of a logit model used to calculate the probability of default. Your answer should include a description of how it is calculated, interpretation, results for a perfect discriminating model and the advantages and disadvantages of this test compared to other discrimination tests (701 question weight The following information is given Rating (A is the best A Observation 1 2 3 4 5 6 7 Default (Yes No O 0 0 1 1 B B B B O 0 QUESTION 2 ANSWER ALL PARTS a. Explain how default occurs for a limited liability company within a structural model. How does the Merton model predict probability of default? (0 question weight b. Describe the payoff to equity and bond holders at maturity within Merton's Distance to Default (DD) model. Explain the relationship between DD and probability of default 20% question weight c. The following information is given for three limited liability companies Company E71,470 26.4% 4. E16,299 Company E71.996 283 Company 76,249 235 Asset value Asset volatility Asset drift rate Short-term labilities Long-term abilities 4SN 4.7% E17,321 E16.987 E35,675 33.282 E34.678 Calculate the Distance to Default (DD) for each company and compare the results. Explain the main drivers of DD based on the information available in the above table. Which company is the most risky? (40% question weight CONTINUES ON NEXT PAGE QUESTION Interpret the Receiver Operating Characteristic (ROC) test for discrimination of a logit model used to calculate the probability of default. Your answer should include a description of how it is calculated, interpretation, results for a perfect discriminating model and the advantages and disadvantages of this test compared to other discrimination tests (701 question weight The following information is given Rating (A is the best A Observation 1 2 3 4 5 6 7 Default (Yes No O 0 0 1 1 B B B B O 0