Answered step by step

Verified Expert Solution

Question

1 Approved Answer

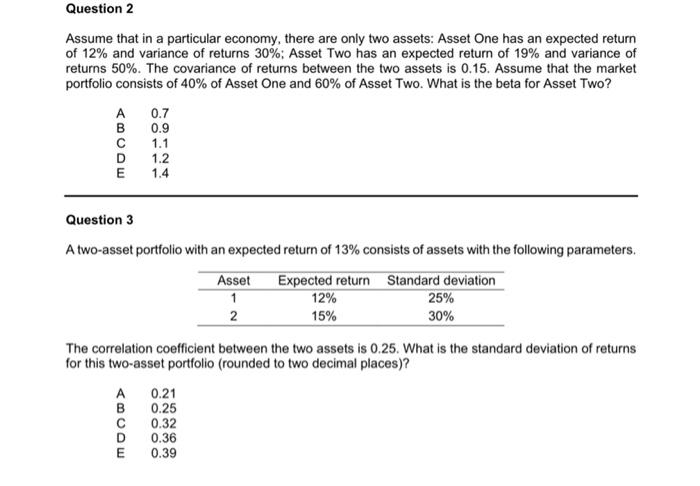

Question 2 Assume that in a particular economy, there are only two assets: Asset One has an expected return of 12% and variance of

Question 2 Assume that in a particular economy, there are only two assets: Asset One has an expected return of 12% and variance of returns 30%; Asset Two has an expected return of 19% and variance of returns 50%. The covariance of returns between the two assets is 0.15. Assume that the market portfolio consists of 40% of Asset One and 60% of Asset Two. What is the beta for Asset Two? 0.7 %3D A B 0.9 1.1 1.2 1.4 E Question 3 A two-asset portfolio with an expected return of 13% consists of assets with the following parameters. Expected return Standard deviation 12% Asset 25% 2 15% 30% The correlation coefficient between the two assets is 0.25. What is the standard deviation of returns for this two-asset portfolio (rounded to two decimal places)? 0.21 0.25 0.32 0.36 0.39 ABCDE

Step by Step Solution

★★★★★

3.47 Rating (150 Votes )

There are 3 Steps involved in it

Step: 1

1 Choose option D 12 2 Expected return of the Portfolio ErP 13 Ex...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investments, Valuation and Management

Authors: Bradford Jordan, Thomas Miller, Steve Dolvin

8th edition

1259720697, 1259720691, 1260109437, 9781260109436, 978-1259720697