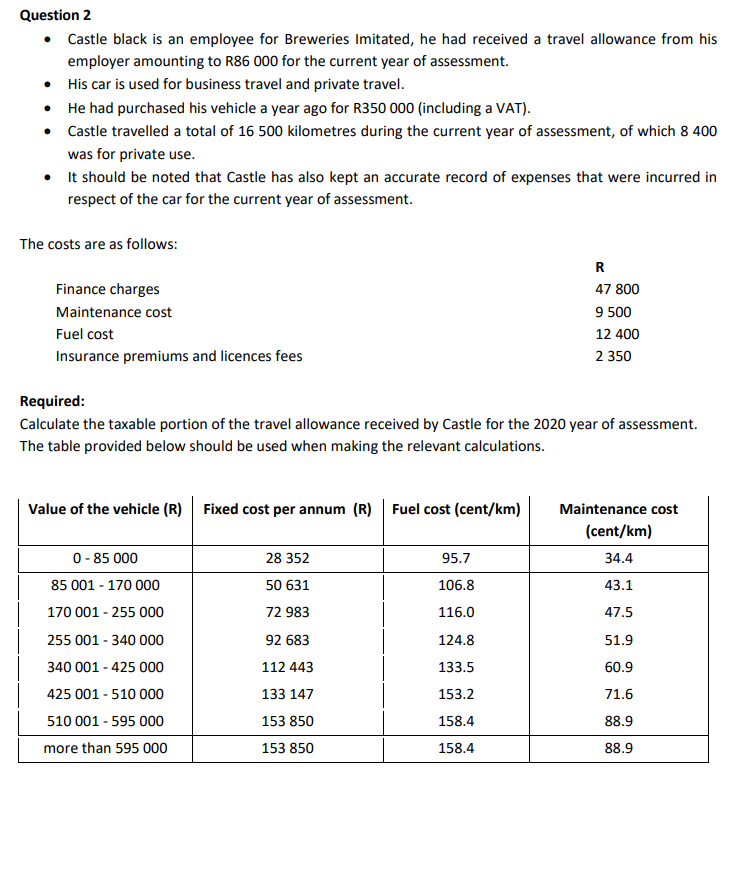

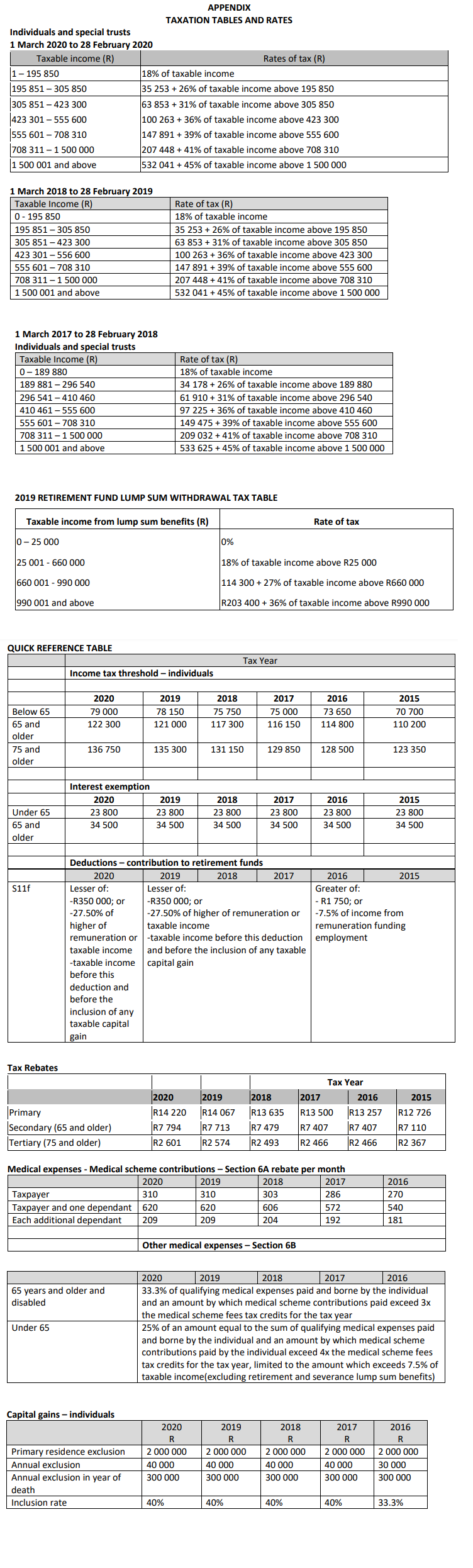

Question 2 Castle black is an employee for Breweries Imitated, he had received a travel allowance from his employer amounting to R86 000 for the current year of assessment. His car is used for business travel and private travel. He had purchased his vehicle a year ago for R350 000 (including a VAT). Castle travelled a total of 16 500 kilometres during the current year of assessment, of which 8 400 was for private use. It should be noted that Castle has also kept an accurate record of expenses that were incurred in respect of the car for the current year of assessment. The costs are as follows: Finance charges Maintenance cost Fuel cost Insurance premiums and licences fees R 47 800 9 500 12 400 2 350 Required: Calculate the taxable portion of the travel allowance received by Castle for the 2020 year of assessment. The table provided below should be used when making the relevant calculations. Value of the vehicle (R) Fixed cost per annum (R) Fuel cost (cent/km) Maintenance cost (cent/km) 34.4 95.7 106.8 43.1 28 352 50 631 72 983 92 683 116.0 47.5 124.8 51.9 0-85 000 85 001 - 170 000 170 001 - 255 000 255 001 - 340 000 340 001 - 425 000 425 001 - 510 000 510 001 - 595 000 more than 595 000 112 443 133.5 60.9 153.2 71.6 133 147 153 850 158.4 88.9 153 850 158.4 88.9 APPENDIX TAXATION TABLES AND RATES Individuals and special trusts 1 March 2020 to 28 February 2020 Taxable income (R) Rates of tax (R) 1 - 195 850 18% of taxable income 195 851 - 305 850 35 253 +26% of taxable income above 195 850 305 851 - 423 300 63 853 +31% of taxable income above 305 850 423 301 - 555 600 100 263 + 36% of taxable income above 423 300 555 601 - 708 310 147 891 +39% of taxable income above 555 600 708 311 - 1 500 000 207 448 + 41% of taxable income above 708 310 |1 500 001 and above 532 041 +45% of taxable income above 1 500 000 1 March 2018 to 28 February 2019 Taxable income (R) 0 - 195 850 195 851 - 305 850 305 851 - 423 300 423 301-556 600 555 601 - 708 310 708 311 -1 500 000 1 500 001 and above Rate of tax (R) 18% of taxable income 35 253 +26% of taxable income above 195 850 63 853 +31% of taxable income above 305 850 100 263 +36% of taxable income above 423 300 147 891 + 39% of taxable income above 555 600 207 448 + 41% of taxable income above 708 310 532 041 +45% of taxable income above 1 500 000 1 March 2017 to 28 February 2018 Individuals and special trusts Taxable income (R) 0-189 880 189 881 - 296 540 296 541 - 410 460 410 461-555 600 555 601 - 708 310 708 311 - 1 500 000 1 500 001 and above Rate of tax (R) 18% of taxable income 34 178 +26% of taxable income above 189 880 61 910 + 31% of taxable income above 296 540 97 225 + 36% of taxable income above 410 460 149 475 +39% of taxable income above 555 600 209 032 +41% of taxable income above 708 310 533 625 +45% of taxable income above 1 500 000 2019 RETIREMENT FUND LUMP SUM WITHDRAWAL TAX TABLE Taxable income from lump sum benefits (R) Rate of tax 0-25 000 0% 25 001 - 660 000 18% of taxable income above R25 000 660 001 - 990 000 114 300 + 27% of taxable income above R660 000 990 001 and above R203 400 + 36% of taxable income above R990 000 QUICK REFERENCE TABLE Tax Year Income tax threshold - individuals 2018 2016 2020 79 000 122 300 2019 78 150 121 000 75 750 117 300 2017 75 000 116 150 73 650 114 800 2015 70 700 110 200 Below 65 65 and older 75 and older 136 750 135 300 131 150 129 850 128 500 123 350 Interest exemption 2020 23 800 34 500 Under 65 65 and older 2019 23 800 34 500 2018 23 800 34 500 2017 23 800 34 500 2016 23 800 34 500 2015 23 800 34 500 S11f 2016 2015 Greater of: - R1 750; or -7.5% of income from remuneration funding employment Deductions - contribution to retirement funds 2020 2019 2018 2017 Lesser of: Lesser of: -R350 000; or -R350 000; or -27.50% of -27.50% of higher of remuneration or higher of taxable income remuneration or -taxable income before this deduction taxable income and before the inclusion of any taxable -taxable income capital gain before this deduction and before the inclusion of any taxable capital gain Tax Rebates 2020 2015 Primary Secondary (65 and older) Tertiary (75 and older) R12 726 R14 220 R7 794 R2 601 2019 R14 067 R7 713 R2 574 2018 R13 635 R7 479 R2 493 Tax Year 2017 2016 R13 500 R13 257 R7 407 R7 407 R2 466 R2 466 R7 110 R2 367 Medical expenses - Medical scheme contributions - Section 6A rebate per month 2020 2019 2018 2017 Taxpayer 310 310 303 286 Taxpayer and one dependant 620 620 606 572 Each additional dependant 209 209 204 192 2016 270 540 181 Other medical expenses - Section 65 years and older and disabled Under 65 2020 2019 2018 2017 2016 33.3% of qualifying medical expenses paid and borne by the individual and an amount by which medical scheme contributions paid exceed 3x the medical scheme fees tax credits for the tax year 25% of an amount equal to the sum of qualifying expenses paid and borne by the individual and an amount by which medical scheme contributions paid by the individual exceed 4x the medical scheme fees tax credits for the tax year, limited to the amount which exceeds 7.5% of taxable income(excluding retirement and severance lump sum benefits) Capital gains - individuals Primary residence exclusion Annual exclusion Annual exclusion in year of death Inclusion rate 2020 R 2 000 000 40 000 300 000 2019 R 2 000 000 40 000 300 000 2018 R 2 000 000 40 000 300 000 2017 R 2 000 000 40 000 300 000 2016 R 2 000 000 30 000 300 000 40% 40% 40% 40% 33.3%