Answered step by step

Verified Expert Solution

Question

1 Approved Answer

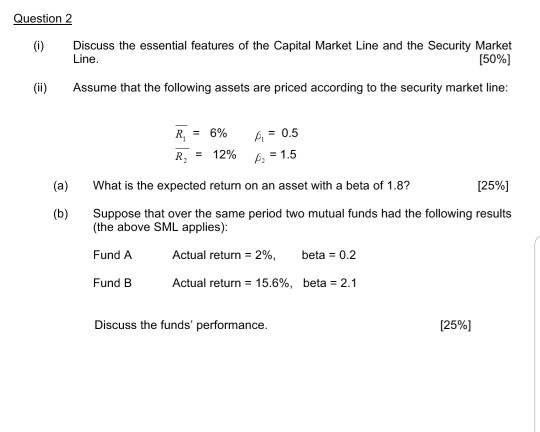

Question 2 () Discuss the essential features of the Capital Market Line and the Security Market [5096] Line () Assume that the following assets are

Question 2 () Discuss the essential features of the Capital Market Line and the Security Market [5096] Line () Assume that the following assets are priced according to the security market line: 0.5 A-1.5 R2-12% (a) What is the expected return on an asset with a beta of 1.8? [2596] (b) Suppose that over the same period two mutual funds had the following results (the above SML applies): Fund A Actual return-2%, beta-0.2 Fund B Actual return: 15.6%, beta-2.1 Discuss the funds' performance [25%)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance for Executives Managing for Value Creation

Authors: Gabriel Hawawini, Claude Viallet

4th edition

9781133169949, 538751347, 978-0538751346