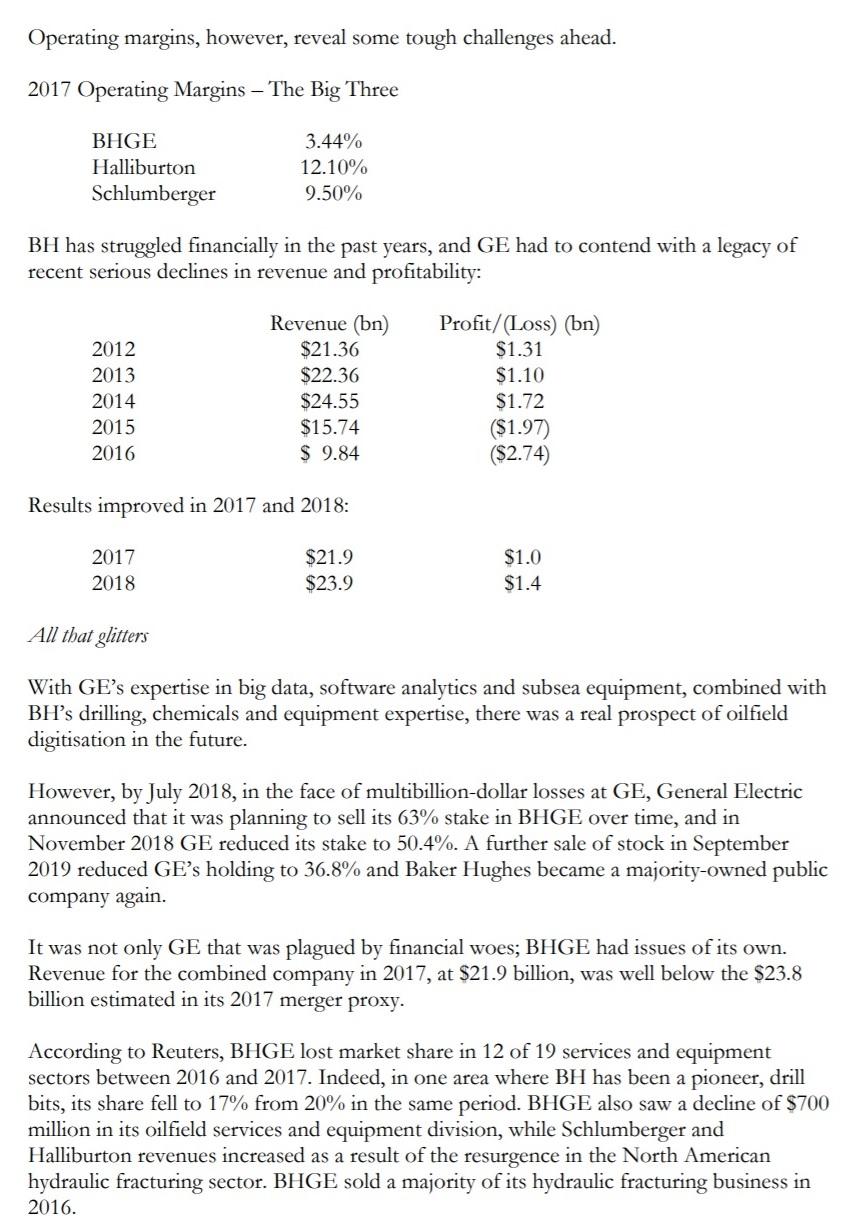

Question 2 Fullstream abead? In 2016 General Electric (GE) was in the process of restructuring and decided to expand its oil and gas operations by merging with America's Baker Hughes (BH), an oilfield services group. The new name of the company was Baker Hughes, a GE Company (BHGE). With headquarters in London and Houston, the combined firm would have a predicted $23 billion in annual revenue. One key rationale for the merger was that the new company would benefit from GE's big-data analytics technology, giving BHGE a clear edge' over its two largest rivals, Schlumberger and Halliburton. The deal was based on an expected recovery in the oil price to $60 per barrel by 2019. Both organisations were large players in the energy services sector, but combined they were able to offer 'fullstream' services, i.e. from finding and drilling for oil and gas (upstream about 60% of revenues) through midstream assets such as pipelines and processing plants (25%), to downstream refineries and product deliveries (5%). The remainder of revenues came from activities described as others'. The CEO of the merged company would be GE Oil & Gas CEO Lorenzo Simonelli. He declared that he would seek to reduce the costs of doing business by increasing efficiencies, innovation, integration and collaboration across the energy value chain'. The optimisation of working capital and disciplined resource allocation, stated Simonelli, were part of the goal of delivering 90% free cash flow conversion over time'. With a fullstream portfolio, Simonelli argued that the boom and bust cycle of the oil industry could be softened by balancing the company's short-term equipment and service contracts in the oil patch with long-term contracts for the liquefied natural gas (LNG) and offshore industries. The LNG market is one of the fastest-growing parts of the fossil fuel industry, and as BHGE is the only major company that manufactures the equipment to liquefy natural gas, this is a very lucrative area. BHGE continued its aggressive pursuit of market share in the LNG industry, now with the benefit of technology originally developed by GE, and during 2017 and 2018, the company was awarded contracts to supply high- horsepower and cleaner-burning gas turbines to LNG plants under development in Texas, the Russian Arctic Circle and other locations around the world. BHGE Subsea Connect product line, developed by GE, can be deployed on the sea floor thousands of feet below the ocean's surface. As it is able to withstand the deep-water high pressures and temperatures, BHGE estimates that it can unlock an additional 16 billion barrels of global oil reserves. Operating margins, however, reveal some tough challenges ahead. 2017 Operating Margins - The Big Three BHGE Halliburton Schlumberger 3.44% 12.10% 9.50% BH has struggled financially in the past years, and GE had to contend with a legacy of recent serious declines in revenue and profitability: 2012 2013 2014 2015 2016 Revenue (bn) $21.36 $22.36 $24.55 $15.74 S 9.84 Profit/(Loss) (bn) $1.31 $1.10 $1.72 ($1.97 ($2.74) Results improved in 2017 and 2018: $1.0 2017 2018 $21.9 $23.9 $1.4 All that glitters With GE's expertise in big data, software analytics and subsea equipment, combined with BH's drilling, chemicals and equipment expertise, there was a real prospect of oilfield digitisation in the future. However, by July 2018, in the face of multibillion-dollar losses at GE, General Electric announced that it was planning to sell its 63% stake in BHGE over time, and in November 2018 GE reduced its stake to 50.4%. A further sale of stock in September 2019 reduced GEs holding to 36.8% and Baker Hughes became a majority-owned public company again. It was not only GE that was plagued by financial woes; BHGE had issues of its own. Revenue for the combined company in 2017, at $21.9 billion, was well below the $23.8 billion estimated in its 2017 merger proxy. According to Reuters, BHGE lost market share in 12 of 19 services and equipment sectors between 2016 and 2017. Indeed, in one area where BH has been a pioneer, drill bits, its share fell to 17% from 20% in the same period. BHGE also saw a decline of $700 million in its oilfield services and equipment division, while Schlumberger and Halliburton revenues increased as a result of the resurgence in the North American hydraulic fracturing sector. BHGE sold a majority of its hydraulic fracturing business in 2016. Financial and cultural clashes In addition to falling market share, the merger was not working well in other areas. GE managers took 11 of BHGE's top 15 positions and introduced what one analyst described as a by-the-book' culture, replacing the oil industry's relationship- and trust- based business methods. Commentators pointed to mismanagement and culture clashes that were reported to have unsettled employees and frustrated suppliers and customers. Suppliers had suffered under tight cost-cutting demands, staff had had to cope with tougher sales targets, and some customers left BHGE after abrupt service-fee increases and contract changes. One company, when faced with a demand for a 3.5% discount on goods and a 120-day grace period on payments, rejected the conditions outright. The normal payment terms within the industry are 30 to 60 days. An oil producer that uses BHGE's artificial lift products said the company raised its service prices by 20% late in 2017 with little notice. They're not managing the account as personally as they need to,' the customer said. The untidy transition caused cultural problems too; 'The old culture was torn apart, observed an equity research director. A move to cut staff just before the end-of-year holidays was said to have reduced staff morale, and BHGE lost a number of key employees, many of them veterans of BH. One headhunter reported that more than 50 CVs from BH employees had been received by one professional recruiter in the year from July 2017. BHGE's Chief Global Operations Officer - one of only a few BH executives to remain in senior management after the merger resigned in January 2018 without announcing a new position. BHGE's response was to decline to comment on the departure but to call its overall retention rates 'strong and in line with the market. Now BHGE has started dividing itself even before the two firms were ever fully integrated. As of late September 2019, GE's share fell to below 50%. As an independent company, Baker Hughes has been rebranding itself, and has New York Stock Exchange ticker initials of BKR. The future In concluding his statement in the BHGE 2018 Annual Report, CEO Simonelli wrote: 2018 was a year of significant change in which we made great progress toward our strategic and financial goals. In 2019, we have a renewed sense of purpose and determination to support our customers and take energy forward.' Required: Applying the process model, analyse Mr Simonelli's strategy and state why it was not the success originally predicted. How do you see the future for Baker Hughes, and what are some of the challenges it is likely to face? (Total 100 marks) Question 2 Fullstream abead? In 2016 General Electric (GE) was in the process of restructuring and decided to expand its oil and gas operations by merging with America's Baker Hughes (BH), an oilfield services group. The new name of the company was Baker Hughes, a GE Company (BHGE). With headquarters in London and Houston, the combined firm would have a predicted $23 billion in annual revenue. One key rationale for the merger was that the new company would benefit from GE's big-data analytics technology, giving BHGE a clear edge' over its two largest rivals, Schlumberger and Halliburton. The deal was based on an expected recovery in the oil price to $60 per barrel by 2019. Both organisations were large players in the energy services sector, but combined they were able to offer 'fullstream' services, i.e. from finding and drilling for oil and gas (upstream about 60% of revenues) through midstream assets such as pipelines and processing plants (25%), to downstream refineries and product deliveries (5%). The remainder of revenues came from activities described as others'. The CEO of the merged company would be GE Oil & Gas CEO Lorenzo Simonelli. He declared that he would seek to reduce the costs of doing business by increasing efficiencies, innovation, integration and collaboration across the energy value chain'. The optimisation of working capital and disciplined resource allocation, stated Simonelli, were part of the goal of delivering 90% free cash flow conversion over time'. With a fullstream portfolio, Simonelli argued that the boom and bust cycle of the oil industry could be softened by balancing the company's short-term equipment and service contracts in the oil patch with long-term contracts for the liquefied natural gas (LNG) and offshore industries. The LNG market is one of the fastest-growing parts of the fossil fuel industry, and as BHGE is the only major company that manufactures the equipment to liquefy natural gas, this is a very lucrative area. BHGE continued its aggressive pursuit of market share in the LNG industry, now with the benefit of technology originally developed by GE, and during 2017 and 2018, the company was awarded contracts to supply high- horsepower and cleaner-burning gas turbines to LNG plants under development in Texas, the Russian Arctic Circle and other locations around the world. BHGE Subsea Connect product line, developed by GE, can be deployed on the sea floor thousands of feet below the ocean's surface. As it is able to withstand the deep-water high pressures and temperatures, BHGE estimates that it can unlock an additional 16 billion barrels of global oil reserves. Operating margins, however, reveal some tough challenges ahead. 2017 Operating Margins - The Big Three BHGE Halliburton Schlumberger 3.44% 12.10% 9.50% BH has struggled financially in the past years, and GE had to contend with a legacy of recent serious declines in revenue and profitability: 2012 2013 2014 2015 2016 Revenue (bn) $21.36 $22.36 $24.55 $15.74 S 9.84 Profit/(Loss) (bn) $1.31 $1.10 $1.72 ($1.97 ($2.74) Results improved in 2017 and 2018: $1.0 2017 2018 $21.9 $23.9 $1.4 All that glitters With GE's expertise in big data, software analytics and subsea equipment, combined with BH's drilling, chemicals and equipment expertise, there was a real prospect of oilfield digitisation in the future. However, by July 2018, in the face of multibillion-dollar losses at GE, General Electric announced that it was planning to sell its 63% stake in BHGE over time, and in November 2018 GE reduced its stake to 50.4%. A further sale of stock in September 2019 reduced GEs holding to 36.8% and Baker Hughes became a majority-owned public company again. It was not only GE that was plagued by financial woes; BHGE had issues of its own. Revenue for the combined company in 2017, at $21.9 billion, was well below the $23.8 billion estimated in its 2017 merger proxy. According to Reuters, BHGE lost market share in 12 of 19 services and equipment sectors between 2016 and 2017. Indeed, in one area where BH has been a pioneer, drill bits, its share fell to 17% from 20% in the same period. BHGE also saw a decline of $700 million in its oilfield services and equipment division, while Schlumberger and Halliburton revenues increased as a result of the resurgence in the North American hydraulic fracturing sector. BHGE sold a majority of its hydraulic fracturing business in 2016. Financial and cultural clashes In addition to falling market share, the merger was not working well in other areas. GE managers took 11 of BHGE's top 15 positions and introduced what one analyst described as a by-the-book' culture, replacing the oil industry's relationship- and trust- based business methods. Commentators pointed to mismanagement and culture clashes that were reported to have unsettled employees and frustrated suppliers and customers. Suppliers had suffered under tight cost-cutting demands, staff had had to cope with tougher sales targets, and some customers left BHGE after abrupt service-fee increases and contract changes. One company, when faced with a demand for a 3.5% discount on goods and a 120-day grace period on payments, rejected the conditions outright. The normal payment terms within the industry are 30 to 60 days. An oil producer that uses BHGE's artificial lift products said the company raised its service prices by 20% late in 2017 with little notice. They're not managing the account as personally as they need to,' the customer said. The untidy transition caused cultural problems too; 'The old culture was torn apart, observed an equity research director. A move to cut staff just before the end-of-year holidays was said to have reduced staff morale, and BHGE lost a number of key employees, many of them veterans of BH. One headhunter reported that more than 50 CVs from BH employees had been received by one professional recruiter in the year from July 2017. BHGE's Chief Global Operations Officer - one of only a few BH executives to remain in senior management after the merger resigned in January 2018 without announcing a new position. BHGE's response was to decline to comment on the departure but to call its overall retention rates 'strong and in line with the market. Now BHGE has started dividing itself even before the two firms were ever fully integrated. As of late September 2019, GE's share fell to below 50%. As an independent company, Baker Hughes has been rebranding itself, and has New York Stock Exchange ticker initials of BKR. The future In concluding his statement in the BHGE 2018 Annual Report, CEO Simonelli wrote: 2018 was a year of significant change in which we made great progress toward our strategic and financial goals. In 2019, we have a renewed sense of purpose and determination to support our customers and take energy forward.' Required: Applying the process model, analyse Mr Simonelli's strategy and state why it was not the success originally predicted. How do you see the future for Baker Hughes, and what are some of the challenges it is likely to face? (Total 100 marks)