QUESTION 2

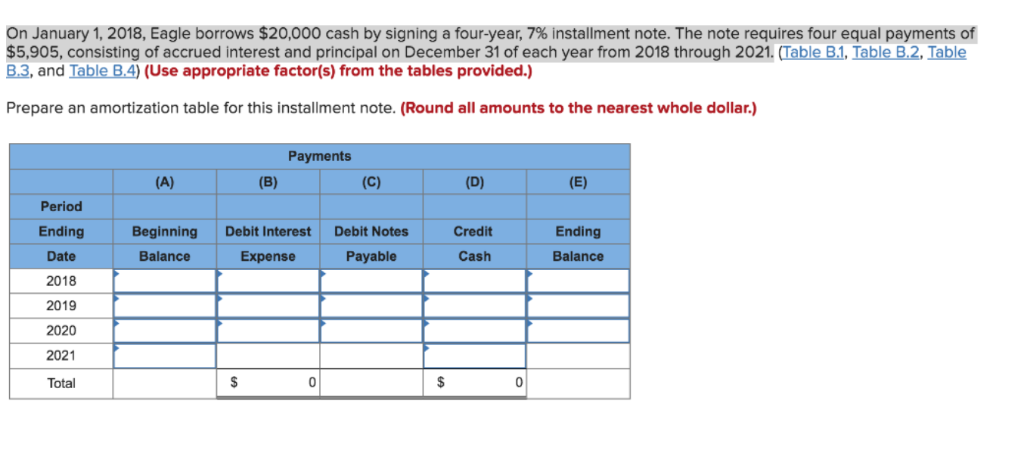

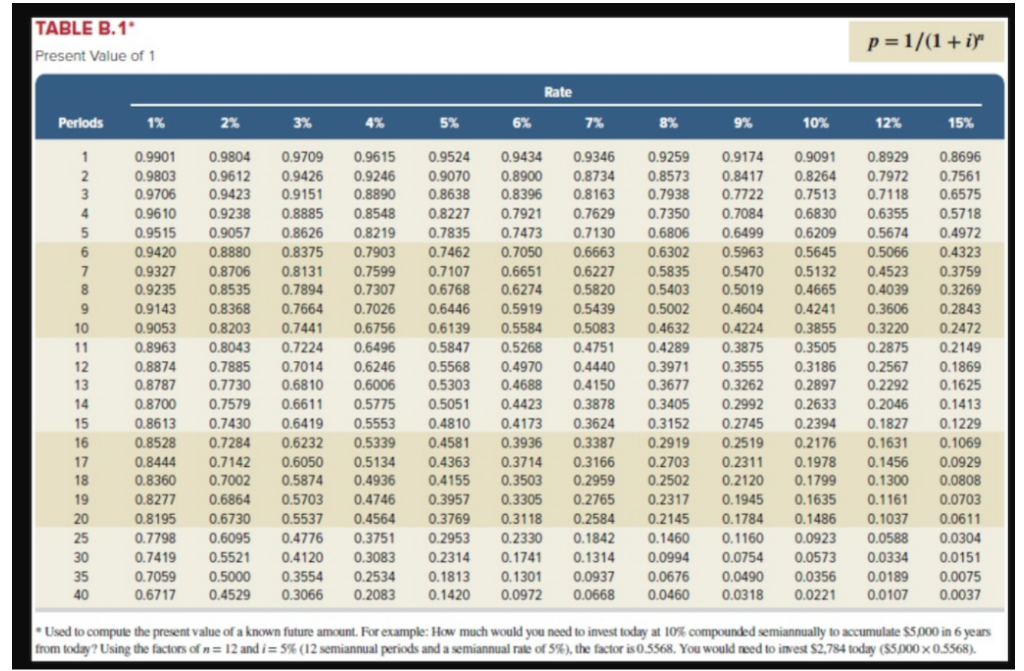

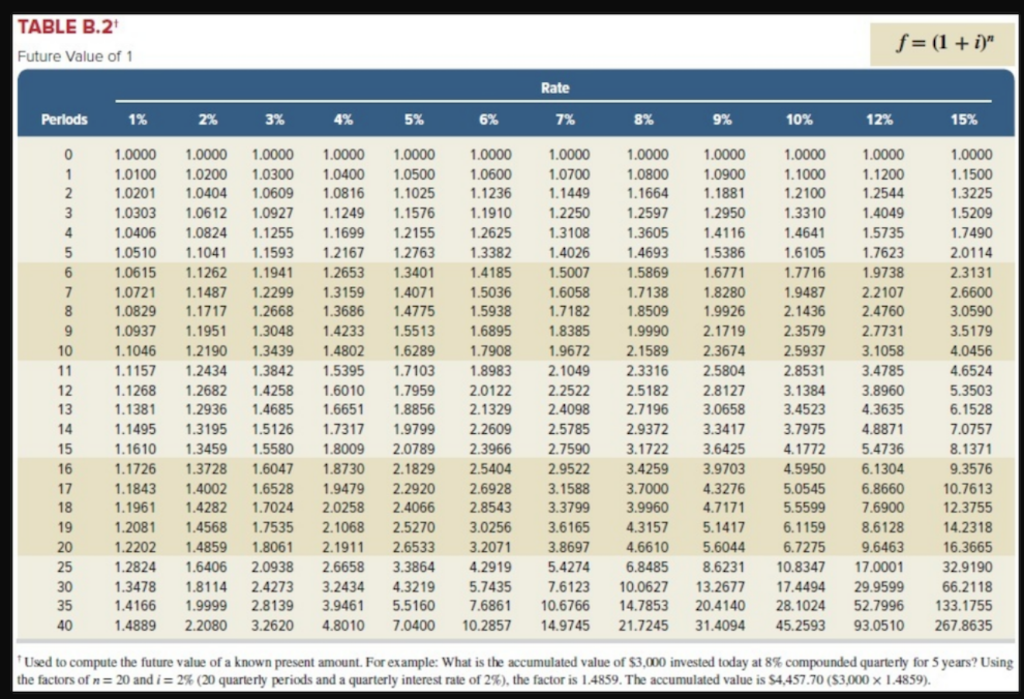

On January 1, 2018, Eagle borrows $20,000 cash by signing a four-year, 7% installment note. The note requires four equal payments of $5,905, consisting of accrued interest and principal on December 31 of each year from 2018 through 2021(Table B1, Table B.2, Table B.3, and Table B.4) (Use appropriate factor(s) from the tables provided.) Prepare an amortization table for this installment note. (Round all amounts to the nearest whole dollar.) Payments Period Ending Date 2018 2019 2020 2021 Total Credit Ending Beginning Debit Interest Debit Notes Expense Balance Payable Cash Balance Present Value of an Annuity of 1 Rate Perlods 1% 2% 3% 5% 6% 7% 9% 10% 125 15% 0.99010.9804 0.97090.9615 0.9524 0.94340.9346 0.9259 0.9174 0.9091 0.89290.8696 2 1.9704 1.9416 1.9135 1.8861 1.8594 1.8334 1.8080 1.7833 1.7591 1.7355 1.6901 1.6257 294102.8839 2.8286 2.775 2.7232 2.6730 2.6243 2.5771 2.5313 2.4869 2.4018 2.2832 4 3.9020 3.80773.71713.6299 3.5460 3.4651 3.3872 3.3121 3.2397 3.1699 3.0373 2.8550 4.85344.71354.5797 4.4518 4.3295 4.2124 4.1002 3.9927 3.8897 3.79083.60483.3522 5.7955 5.60145.4172 5.2421 5.0757 4.9173 4.7665 4.6229 4.4859 4.35534.11143.7845 6.72826.4720 6.2303 6.0021 5.78645.5824 5.3893 5.2064 5.03304.8684 4.5638 4.1604 7.6517 7.3255 7.01976.7327 6.4632 6.2098 5.9713 5.7466 5.5348 5.33494.96764.4873 9 8.5660 8.1622 7.78617.4353 7.1078 6.8017 6.5152 6.2469 5.9952 5.7590 5.3282 4.7716 10 9.4713 8.9826 8.5302 8.1109 7.7217 7.3601 7.0236 6.7101 6.41776.1446 5.6502 5.0188 0.3676 9.78689.2526 8.7605 8.3064 7.8869 7.4987 7.1390 6.80526.49515.93775.2337 2551 10.57539.95409.3851 8.8633 8.3838 7.9427 7.5361 7.1607 6.8137 6.19445.4206 2.1337 11.348410.6350 9.9856 9.3936 8.8527 8.3577 7.90387.48697.10346.42355.5831 8.7455 8.2442 7.78627.3667 6.6282 5.7245 3.8651 12.849311.9379 11.1184 10.3797 9.7122 9.1079 8.55958.06077.60616.81095.8474 16 14.7179 13.5777 12.5611 11.6523 10.8378 10.1059 9.4466 8.8514 8.3126 7.8237 6.9740 5.9542 15.5623 14.291913.1661 12.1657 11.2741 10.4773 9.7632 9.12168.54368.02167.1196 6.0472 16.3983 14.992013.7535 12.6593 11.6896 10.8276 10.0591 9.3719 8.75568.20147.24976.1280 17.2260 15.678514.3238 13.1339 12.0853 11.1581 10.3356 9.60368.95018.36497.3658 6.1982 8.0456 16.3514 14.8775 13.5903 12.4622 11.4699 10.5940 9.81819.12858.5136 7.46946.2593 3.0037 2.1062 11.2961 10.5631 9.89869.2950 22.0232 19.5235 17.4131 15.6221 14.0939 12.7834 116536 10.67489.8226 9.0770 7.8431 6.464 5.807722.3965 19.6004 17.2920 15.3725 13.764812.4090 11.2578 10.27379.4269 8.0552 6.5660 29.4086 24.9986 21.4872 18.6646 16.3742 14.4982 12.9477 11.6546 10.5668 9.6442 8.17556.6166 2.8347 27.3555 23.114819.7928 17.1591 15.046313.3317 11.924610.7574 9.7791 8.2438 6.6418 35 Used to calculate the present value of a series of equal payments made at the end of each period. For example: What is the present value of $2,000 per year for 10 years assuming an annual interest rate of 9% For (n 10.1 9%), the PV factor s 6.4 l T7 S2.000 per year for lo years is the equivalent of S 12,835 today (S2.0006.41 T7). Future Value of an Annuity of Rate 2% 3% 5% 7% 8% 9% 10 0000 10000 1.0000 1.0000 1.00000000 1.0000 1.0000 .0000 1.0000 1.0000 2.0100 2.0200 2.0300 2.0400 2.0500 2.0600 2.0700 2.0800 2.09002.1000 2.1200 3 3.0301 3.0604 3.0909 3.1216 3.1525 3.18363.21493.2464 3.2781 3.3100 3.3744 3.4725 0604 4.1216 4.18364.24654.310143746 4.4399 4.5061 4.5731 4.6410 4.7793 5.1010 5.2040 5.3091 5.41635.5256 5.6371 5.75075.8666 5.98476.1051 6.3528 6 6.1520 6.3081 6.4684 6.6330 6.8019 6.97537.15337.3359 7.5233 7.7156 8.1152 8.7537 7.2135 7.43437.6625 7.8983 8.1420 8.39388.6540 8.9228 9.2004 9.4872 10.0890 11.0668 8 8.2857 8.5830 8.8923 9.2142 9.5491 9.8975 10.2598 10.6366 11.0285 11.4359 12.2997 13.7268 9 9.3685 9.7546 10.1591 10.5828 11.0266 11.4913 11.978012.4876 13.0210 13.5795 14.775716.7858 10 10.4622 10.9497 11.4639 12.0061 12.5779 13.1808 13.8164 14.4866 15.1929 15.937417.548720.3037 11.5668 12.1687 12.8078 13.4864 14.2068 14.971615.7836 16.6455 7.5603 18.5312 20.6546 24.3493 2 12.6825 13.4121 14.1920 15.0258 15.9171 16.869917.8885 18.9771 20.1407 21.3843 24.1331 29.0017 3 13.8093 14.6803 15.6178 16.6268 17.713018.8821 20.1406 21.4953 229534 24.5227 28.0291 34.3519 4 14.9474 15.9739 17.086318.2919 19.5986 21.0151 22.5505 24.2149 26.0192 27.9750 32.3926 40.5047 15 16.0969 17.2934 18.5989 20.0236 21.5786 23.2760 25.1290 27.1521 293609 3m25 372,97 47500. 6 17.2579 18.6393 20.1569 21.8245 23.6575 25.6725 27.8881 30.3243 33.0034 35.9497 42.7533 55.7175 7 18.4304 20.0121 21.7616 23.6975 25.8404 28.2129 30.840233.7502 36.9737 40.5447 48.883765.0751 8 19.6147 21.4123 23.414425.6454 28.1324 30.9057 33.9990 37.4502 41.301345.5992 55.7497 75.8364 19 20.8109 22.8406 25.1169 27.6712 30.5390 33.7600 37.3790 41.4463 46.0185 51.1591 63.4397 88.2118 20 22.0190 24.2974 26.8704 29.7781 33.0660 36.7856 40.995545.7620 51.1601 57.2750 72.0524102.4436 25 28.2432 32.0303 36.4593 41.6459 47.7271 54.8645 63.2490 73.1059 84.700998.3471 133.3339 212.7930 0 34.7849 40.5681 47.5754 56.0849 66.4388 79.0582 94.4608113.2832 136.3075 164.4940 241.3327434.7451 5 41.6603 49.9945 60.4621 73.6522 90.3203 111.4348 138.2369 172.3168 215.7108 271.0244 431.6635 881.1702 40 48.8864 60.4020 75.4013 95.0255 120.7998 154.7620 199.6351259.0565 337.8824 442.5926 767.0914 1,779.0903 3 Used to calculate the future value of a series of equal payments made at the end of each period. For example: What is the future value of $4,000 per year for 6 years assuming an annual interest rate of 8%. For (n 6= 8%), the FV factor is 7.3359. S4.000 per year for 6 years accumulates to $29.343.60 ($4,000 7.3359). Ellis issues 6.5%, five-year bonds dated January 1, 2018, with a $570,000 par value. The bonds pay interest on June 30 and December 31 and are issued at a price of $582159. The annual market rate is 6% on the issue date. (TableB 1, Table 32. Table B.3, and Table B.4) (Use appropriate factor(s) from the tables provided.) Required: 1. Compute the total bond interest expense over the bonds' life. 2. Prepare an effective interest amortization table for the bonds' life. 3. Prepare the journal entries to record the first two interest payments 4. Use the market rate at issuance to compute the present value of the remaining cash flows for these bonds as of December 31, 2020