Question

Question 2 Parent Ltd acquired equity in Sub Ltd on 1 April 2009. At that date, the identifiable net assets were considered to be fairly

Question 2

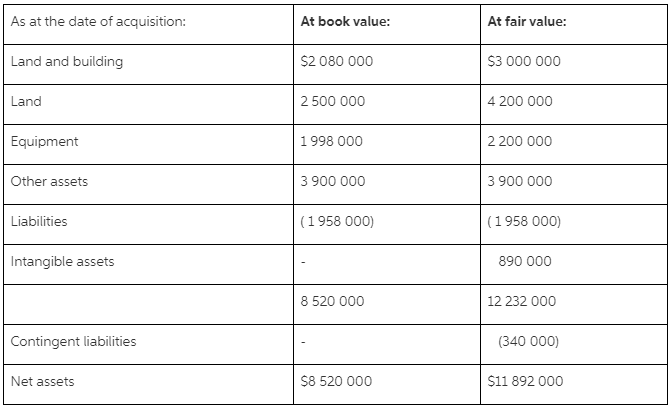

Parent Ltd acquired equity in Sub Ltd on 1 April 2009. At that date, the identifiable net assets were considered to be fairly valued and the equity of Sub Ltd comprised:

| Share capital | $700 000 |

| Asset revaluation surplus | 45 000 |

| Retained earnings | 278 000 |

| $1 023 000 |

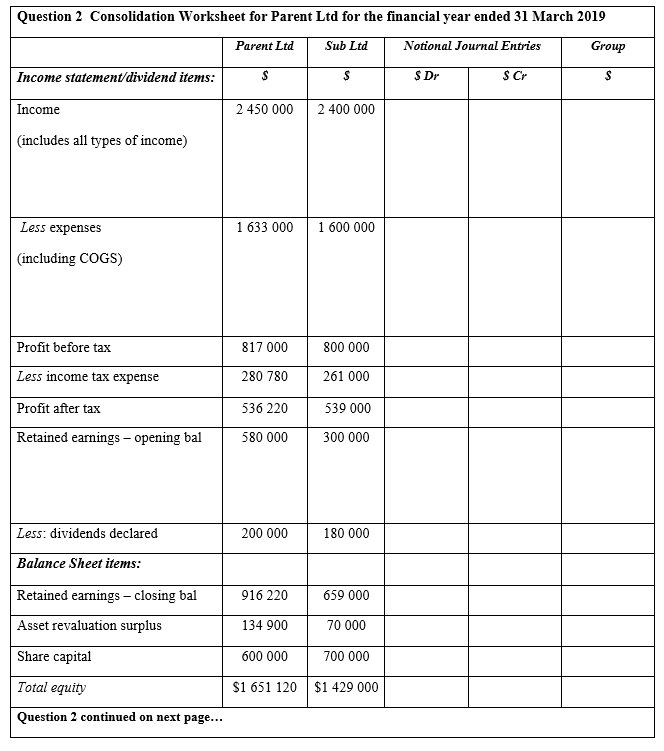

Parent Ltd has requested your help in the preparation of their consolidated financial statements for the financial year ended 31 March 2019 and has provided you with the following information:

- During March 2018 Sub Ltd made sales to Parent Ltd of $8 000 and recognised a profit of $4 200. Parent Ltd sold this purchase of inventory to Robert Ltd during May 2018.

- During March 2019 Sub Ltd made sales to Parent Ltd of $ 8 500. The inventory sold has cost Sub Ltd $5 400. At 31 March 2019, the inventory Parent Ltd had on hand included this purchase from Sub Ltd.

- Parent Ltd borrowed $60 000 from Sub Ltd during November 2017. Interest of $1 200 is outstanding on this loan as at 31 March 2019. The total interest for the financial year ended 31 March 2019 was $1 500.

- In 2011 the total goodwill of Sub Ltd was considered by the directors to be impaired by $ 15 000 and impaired again in 2016 by $ 72 600. The directors of Parent Ltd believe that the total goodwill has been further impaired by $63 000 during this financial year ended 31 March 2019.

- During March 2018 Parent Ltd made sales to Sub Ltd of $3 200 and recognised a profit of $1 600. Sub Ltd sold this inventory to Alex Ltd on 31 March 2018.

- During March 2019 Parent Ltd made sales to Sub Ltd of $4 860. The inventory sold has cost Parent Ltd $2 000. The inventory of Sub Ltd at 31 March 2019 included this purchase.

- At 31 March 2019 Sub Ltd declared a final dividend of $120 000 and Parent Ltd declared a final dividend of $75 000. Both these dividends were paid during April 2019.

- Parent Ltd rents a small office to Sub Ltd at a cost of $26 000 per annum. At 31 March 2019, Sub Ltd still owed Parent Ltd $5 000 of rental for the year ended 31 March 2019.

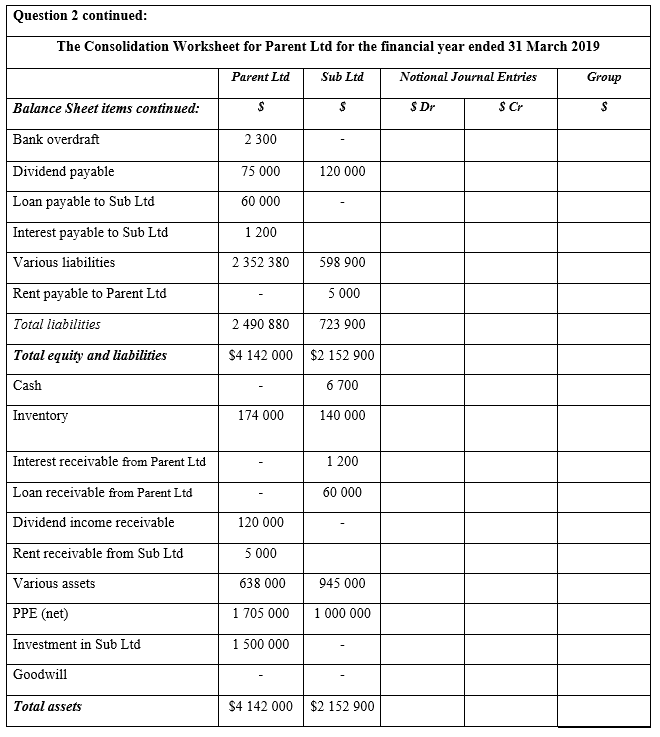

Question 2 continued:

Required:

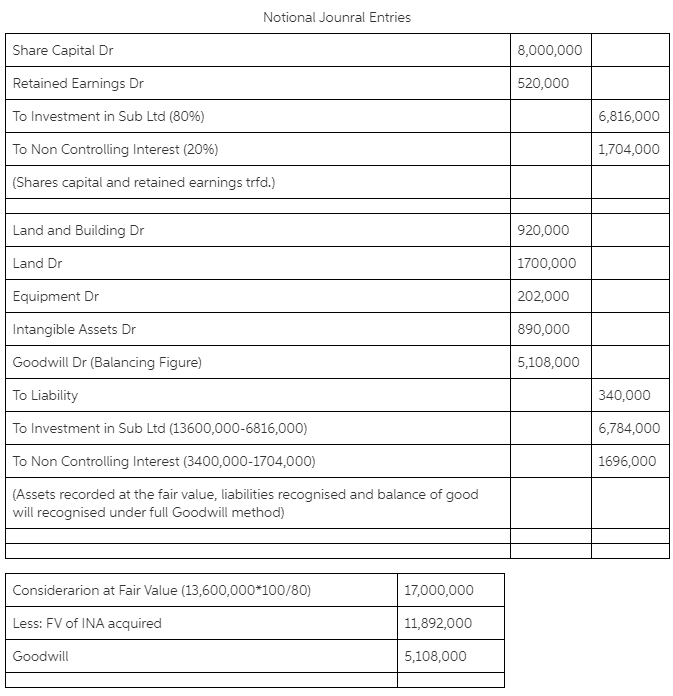

Assume Parent Ltd acquired 100% of the equity in Sub Ltd for $1 500 000 on

1 April 2009. Complete the consolidation worksheet, in the answer booklet, for Parent Ltd for the financial year ended 31 March 2019 in accordance with NZ IFRS 10 Consolidated Financial Statements and NZ IFRS 3 Business Combinations.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Principles Understanding Important Terms And Principles Of Accounting

Authors: Lyndsay Sudduth

1st Edition

B0B5KV57NJ, 979-8840104033