Answered step by step

Verified Expert Solution

Question

1 Approved Answer

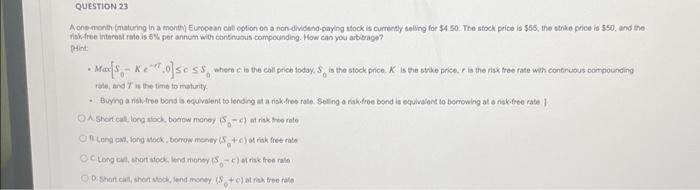

QUESTION 23 A one-month (maturing in a month) European call option on a non-dividend-paying stock is currently selling for $4.50. The stock price is $55,

QUESTION 23 A one-month (maturing in a month) European call option on a non-dividend-paying stock is currently selling for $4.50. The stock price is $55, the strike price is $50, and the risk-free interest rate is 6% per annum with continuous compounding. How can you arbitrage? [Hint: . -rT Maxs - Ke 7,0] S where c is the call price today, S is the stock price, K is the strike price, r is the risk free rate with continuous compounding 0 0 rate, and T is the time to maturity. Buying a risk-free bond is equivalent to lending at a risk-free rate. Selling a risk-free bond is equivalent to borrowing at a risk-free rate. ] OA. Short call, long stock, borrow money (S-c) at risk free rate OB. Long call, long stock, borrow money (S + c) at risk free rate 0 OC. Long call, short stock, lend money (S-c) at risk free rate . OD. Short call, short stock, lend money (S+c) at risk free rate 0

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of The Fundamentals Of Financial Decision Making

Authors: Leonard C MacLean, William T Ziemba

1st Edition

9814417343, 978-9814417341