Answered step by step

Verified Expert Solution

Question

1 Approved Answer

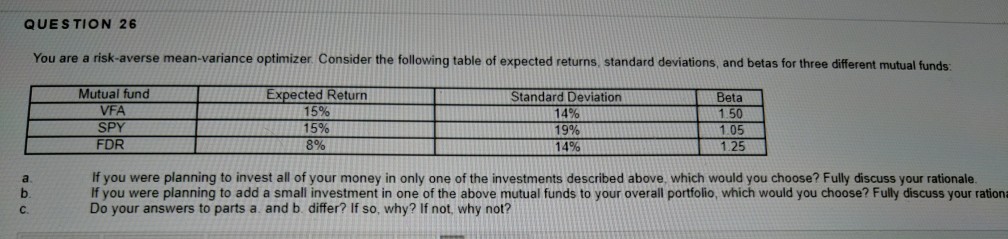

QUESTION 26 You are a risk-averse mean-variance optimizer. Consider the following table of expected returns, standard deviations, and betas for three different mutual funds: Mutual

QUESTION 26 You are a risk-averse mean-variance optimizer. Consider the following table of expected returns, standard deviations, and betas for three different mutual funds: Mutual fund Expected Return 15% 15% 8% tandard Deviation VFA SPY FDR 14% 19% 14% Beta 1.50 1.05 1.25 If you were planning to invest all of your money in only one of the investments described above, which would you choose? Fully discuss your rationale If you were planning to add a small investment in one of the above mutual funds to your overall portfolio, which would you choose? Fully discuss your rationa b. c. Do your answers to parts a and b differ? If so, why? If not, why not

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Successful Fundraising For Arts And Cultural Organizations

Authors: Carolyn S. Friedman, Karen B. Hopkins

2nd Edition

1573560294, 978-1573560290