Question 2(a) will truly be appreciated.

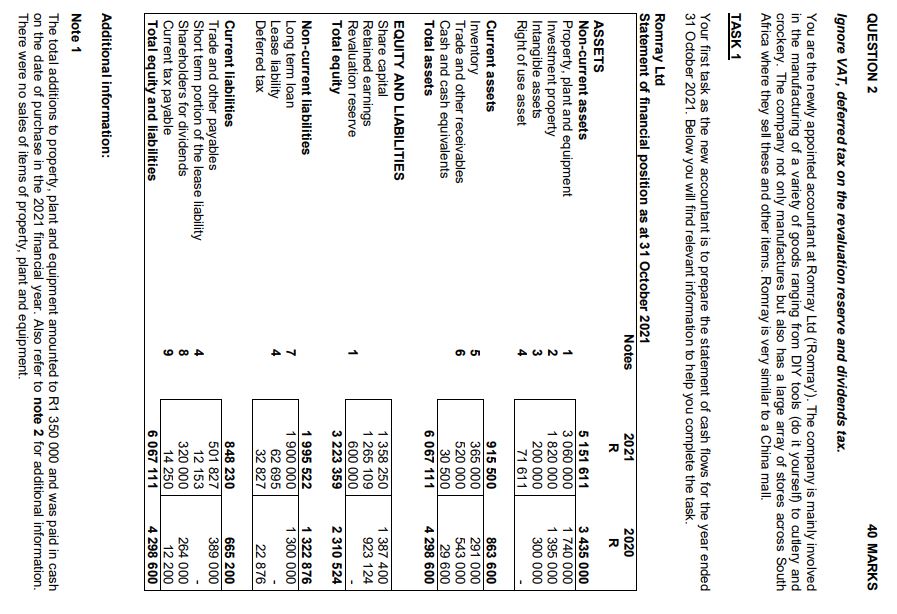

QUESTION 2 40 MARKS Ignore VAT, deferred tax on the revaluation reserve and dividends tax. You are the newly appointed accountant at Romray Ltd ('Romray'). The company is mainly involved in the manufacturing of a variety of goods ranging from DIY tools (do it yourself) to cutlery and crockery. The company not only manufactures but also has a large array of stores across South Africa where they sell these and other items. Romray is very similar to a China mall. TASK 1 Your first task as the new accountant is to prepare the statement of cash flows for the year ended 31 October 2021. Below you will find relevant information to help you complete the task. Romray Ltd Statement of financial position as at 31 October 2021 Notes 2021 2020 R R ASSETS Non-current assets 5 151 611 3 435 000 Property, plant and equipment 1 3 060 000 1 740 000 Investment property 2 1 820 000 1 395 000 Intangible assets 3 200 000 300 000 Right of use asset 71 611 Current assets 915 500 863 600 Inventory 5 365 000 291 000 Trade and other receivables 6 520 000 543 000 Cash and cash equivalents 30 500 29 600 Total assets 6 067 111 4 298 600 4 1 358 250 1 265 109 600 000 3 223 359 1 387 400 923 124 EQUITY AND LIABILITIES Share capital Retained earnings Revaluation reserve Total equity Non-current liabilities Long term loan Lease liability Deferred tax 1 2 310 524 1 995 522 1 900 000 62 695 32 827 1 322 876 1 300 000 N4 22 876 665 200 389 000 Current liabilities Trade and other payables Short term portion of the lease liability Shareholders for dividends Current tax payable Total equity and liabilities 848 230 501 827 12 153 320 000 14 250 6 067 111 4 8 9 con 264 000 12 200 4 298 600 Additional information: Note 1 The total additions to property, plant and equipment amounted to R1 350 000 and was paid in cash on the date of purchase in the 2021 financial year. Also refer to note 2 for additional information. There were no sales of items of property, plant and equipment. On 31 October 2021 the property owned by Romray was revalued to its fair value. At the date of the revaluation the historical carrying amount amounted to R1 200 000. The total revaluation of this property resulted in a total increase of R700 000 to the value of the property. A previous revaluation took place on 31 October 2019 to a fair value that was lower than the historical carrying amount of the property. All items of property, plant and equipment are accounted for on the cost model in terms of IAS 16 Property, plant and Equipment, except the property that was revalued on 31 October 2021, which is accounted for on the revaluation model in terms of IAS 16 by applying the net replacement value method. The revaluation reserve transfers to retained earnings as the property is used. Note 2 The only addition to investment property was a transfer from property, plant and equipment on 1 November 2020. The carrying amount on the transfer date amounted to R200 000 and the fair value on the transfer date amounted to R225 000. The historical carrying amount of the property amounted to R230 000 on the same date. There were no sales of items of investment property. Investment property is accounted for on the fair value model in terms of IAS 40 Investment Property. Note 3 Romray owns two intangible assets. The first intangible asset has an indefinite useful life and the recoverable amount of the intangible asset on 31 October 2021 was lower than its carrying amount at that date. The second intangible asset (two years old at year end) has a total useful life of five years and an estimated residual value of R5 000. It was originally purchased for R50 000 and has never been impaired since acquisition. None of the intangible assets have an active market. There has been no commitment from a third party to purchase these assets at the end of its useful life. Neither of the intangible assets were sold during the 2021 financial year. Note 4 Romray entered into a lease contract during the 2021 financial year whereby Romray would lease equipment from LML Ltd ('LML") for five years, commencing on 1 June 2021. The lease instalments are payable quarterly in arrears starting from 31 August 2021. The instalments amount to R4 915 and the implicit interest rate of the lease is 2.5% per quarter. There are no guaranteed or unguaranteed residual values. Romray incurred initial direct costs of R1 500 in order to obtain the lease. The lease is a lease as defined by IFRS 16 Leases. Note 5 Included in the inventory movement is a net realisable value write down of R2 500. Note 6 The allowance for credit losses account increased with R15 000 from the prior year allowance. A credit loss of R5 000 was written off during the year. Also included in trade and other debtors is an operating lease receivable. The lease is for a period of three years with the payment for the first year being R10 000 per year and thereafter escalating with 10% on 1 November every year. The lease commenced on 1 November 2019. Note 7 During the 2021 financial year, no interest payments were made on the loan. The loan incurs interest at 12% per year, compounded yearly. The loan is only repayable from 1 November 2022. The loan was increased on 1 November 2020 with an amount of R396 429. Note 8 A payment of R500 000 was made during the 2021 financial year to shareholders for outstanding dividends. Note 9 Provisional tax payments amounting to R300 000 were made during the year. TASK 2 The second task you were giving after helping with the statement of cash flows, was to give some advice with regards to IFRS 15 Revenue from contracts with customers. Romray recently started selling computer tablets together with data packages. These sales have been very lucrative due to the current economic situation where many employees and students work from home and require a smart device and data. Since this is a newer line of business for Romray, they are a little uncertain of how to account for transactions like this. A typical sale would be the tablet together with 10 gigs of data per month for a price of between R800 and R2 000 per month depending on the make and model of the tablet. Only once a customer's credit score has been obtained and approved, a written contract is offered to the customer and signed by the customer and the sales representative of Romray. The contract stipulates the amount, date and number of payments to be made as well as the make and model of the tablet and it specifies that 10 gigs of data will be provided per month. A customer can decide on the length of the contract ranging from six months to two years. The financial manager, Mr D Watson, is aware that revenue can only be recognised if there is a contract with a customer but he is however very uncertain as to what that entails. He knows that you have an up to date knowledge of IFRS 15 and therefore requested your help. REQUIRED: MARKS Sub- Total total 29 1 30 (a) Prepare the reconciliation between profit before tax and cash generated from operations note to the statement of cash flows for the year ended 31 October 2021. Disclose all non-cash items separately in the reconciliation. Comparative figures are not required. Communication skills - presentation and layout (b) Write an email to the financial manager (Mr D Watson), where you discuss step 1 (identify if a contract with a customer exists) of the revenue recognition model of IFRS 15 with regards to the sale of the tablets and data packages. Communication skills - presentation and layout TOTAL MARKS 9 1 10 40 QUESTION 2 40 MARKS Ignore VAT, deferred tax on the revaluation reserve and dividends tax. You are the newly appointed accountant at Romray Ltd ('Romray'). The company is mainly involved in the manufacturing of a variety of goods ranging from DIY tools (do it yourself) to cutlery and crockery. The company not only manufactures but also has a large array of stores across South Africa where they sell these and other items. Romray is very similar to a China mall. TASK 1 Your first task as the new accountant is to prepare the statement of cash flows for the year ended 31 October 2021. Below you will find relevant information to help you complete the task. Romray Ltd Statement of financial position as at 31 October 2021 Notes 2021 2020 R R ASSETS Non-current assets 5 151 611 3 435 000 Property, plant and equipment 1 3 060 000 1 740 000 Investment property 2 1 820 000 1 395 000 Intangible assets 3 200 000 300 000 Right of use asset 71 611 Current assets 915 500 863 600 Inventory 5 365 000 291 000 Trade and other receivables 6 520 000 543 000 Cash and cash equivalents 30 500 29 600 Total assets 6 067 111 4 298 600 4 1 358 250 1 265 109 600 000 3 223 359 1 387 400 923 124 EQUITY AND LIABILITIES Share capital Retained earnings Revaluation reserve Total equity Non-current liabilities Long term loan Lease liability Deferred tax 1 2 310 524 1 995 522 1 900 000 62 695 32 827 1 322 876 1 300 000 N4 22 876 665 200 389 000 Current liabilities Trade and other payables Short term portion of the lease liability Shareholders for dividends Current tax payable Total equity and liabilities 848 230 501 827 12 153 320 000 14 250 6 067 111 4 8 9 con 264 000 12 200 4 298 600 Additional information: Note 1 The total additions to property, plant and equipment amounted to R1 350 000 and was paid in cash on the date of purchase in the 2021 financial year. Also refer to note 2 for additional information. There were no sales of items of property, plant and equipment. On 31 October 2021 the property owned by Romray was revalued to its fair value. At the date of the revaluation the historical carrying amount amounted to R1 200 000. The total revaluation of this property resulted in a total increase of R700 000 to the value of the property. A previous revaluation took place on 31 October 2019 to a fair value that was lower than the historical carrying amount of the property. All items of property, plant and equipment are accounted for on the cost model in terms of IAS 16 Property, plant and Equipment, except the property that was revalued on 31 October 2021, which is accounted for on the revaluation model in terms of IAS 16 by applying the net replacement value method. The revaluation reserve transfers to retained earnings as the property is used. Note 2 The only addition to investment property was a transfer from property, plant and equipment on 1 November 2020. The carrying amount on the transfer date amounted to R200 000 and the fair value on the transfer date amounted to R225 000. The historical carrying amount of the property amounted to R230 000 on the same date. There were no sales of items of investment property. Investment property is accounted for on the fair value model in terms of IAS 40 Investment Property. Note 3 Romray owns two intangible assets. The first intangible asset has an indefinite useful life and the recoverable amount of the intangible asset on 31 October 2021 was lower than its carrying amount at that date. The second intangible asset (two years old at year end) has a total useful life of five years and an estimated residual value of R5 000. It was originally purchased for R50 000 and has never been impaired since acquisition. None of the intangible assets have an active market. There has been no commitment from a third party to purchase these assets at the end of its useful life. Neither of the intangible assets were sold during the 2021 financial year. Note 4 Romray entered into a lease contract during the 2021 financial year whereby Romray would lease equipment from LML Ltd ('LML") for five years, commencing on 1 June 2021. The lease instalments are payable quarterly in arrears starting from 31 August 2021. The instalments amount to R4 915 and the implicit interest rate of the lease is 2.5% per quarter. There are no guaranteed or unguaranteed residual values. Romray incurred initial direct costs of R1 500 in order to obtain the lease. The lease is a lease as defined by IFRS 16 Leases. Note 5 Included in the inventory movement is a net realisable value write down of R2 500. Note 6 The allowance for credit losses account increased with R15 000 from the prior year allowance. A credit loss of R5 000 was written off during the year. Also included in trade and other debtors is an operating lease receivable. The lease is for a period of three years with the payment for the first year being R10 000 per year and thereafter escalating with 10% on 1 November every year. The lease commenced on 1 November 2019. Note 7 During the 2021 financial year, no interest payments were made on the loan. The loan incurs interest at 12% per year, compounded yearly. The loan is only repayable from 1 November 2022. The loan was increased on 1 November 2020 with an amount of R396 429. Note 8 A payment of R500 000 was made during the 2021 financial year to shareholders for outstanding dividends. Note 9 Provisional tax payments amounting to R300 000 were made during the year. TASK 2 The second task you were giving after helping with the statement of cash flows, was to give some advice with regards to IFRS 15 Revenue from contracts with customers. Romray recently started selling computer tablets together with data packages. These sales have been very lucrative due to the current economic situation where many employees and students work from home and require a smart device and data. Since this is a newer line of business for Romray, they are a little uncertain of how to account for transactions like this. A typical sale would be the tablet together with 10 gigs of data per month for a price of between R800 and R2 000 per month depending on the make and model of the tablet. Only once a customer's credit score has been obtained and approved, a written contract is offered to the customer and signed by the customer and the sales representative of Romray. The contract stipulates the amount, date and number of payments to be made as well as the make and model of the tablet and it specifies that 10 gigs of data will be provided per month. A customer can decide on the length of the contract ranging from six months to two years. The financial manager, Mr D Watson, is aware that revenue can only be recognised if there is a contract with a customer but he is however very uncertain as to what that entails. He knows that you have an up to date knowledge of IFRS 15 and therefore requested your help. REQUIRED: MARKS Sub- Total total 29 1 30 (a) Prepare the reconciliation between profit before tax and cash generated from operations note to the statement of cash flows for the year ended 31 October 2021. Disclose all non-cash items separately in the reconciliation. Comparative figures are not required. Communication skills - presentation and layout (b) Write an email to the financial manager (Mr D Watson), where you discuss step 1 (identify if a contract with a customer exists) of the revenue recognition model of IFRS 15 with regards to the sale of the tablets and data packages. Communication skills - presentation and layout TOTAL MARKS 9 1 10 40