Answered step by step

Verified Expert Solution

Question

1 Approved Answer

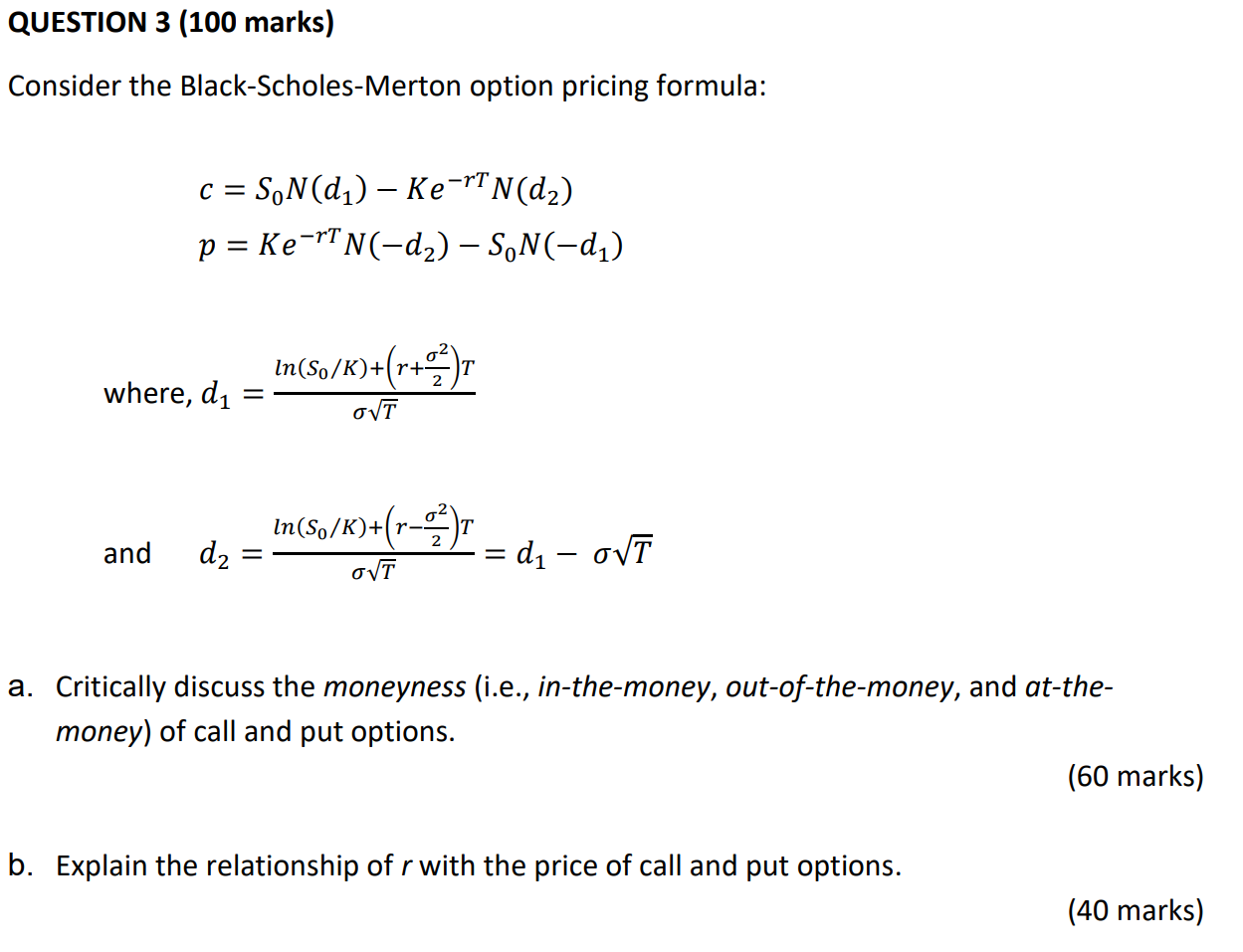

QUESTION 3 (100 marks) Consider the Black-Scholes-Merton option pricing formula: -rT c = SN(d) Ke N(d) p= Ke-TN(-d) - SoN(-d) 0 In(So/K)+r+ T where, d

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Analysis Concentrate On Analyzing Economic Indicators Company Financials And Market News

Authors: Brandom Elder

1st Edition

1806216604, 978-1806216604