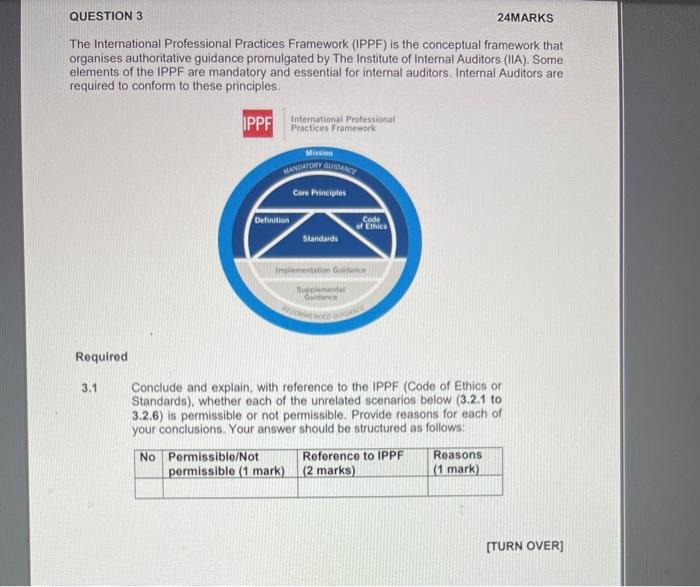

QUESTION 3 24MARKS The International Professional Practices Framework (IPPF) is the conceptual framework that organises authoritative guidance promulgated by The Institute of Internal Auditors (IIA). Some elements of the IPPF are mandatory and essential for internal auditors. Internal Auditors are required to conform to these principles. IPPF International Professional Practices Framework Mission MANDATORY GUINE Core Principles Definition Code Standards of Ethics Implementation Guide Supplement Guidance Required 3.1 Conclude and explain, with reference to the IPPF (Code of Ethics or Standards), whether each of the unrelated scenarios below (3.2.1 to 3.2.6) is permissible or not permissible. Provide reasons for each of your conclusions. Your answer should be structured as follows: No Permissible/Not Roforonco to IPPF Reasons permissiblo (1 mark) (2 marks) (1 mark) [TURN OVER] 3.1.1 Nkosinathi Kwena, a senior internal auditor has recently been appointed in the internal audit function of Plastic Design Ltd. In his quest to understand the division, he reviewed previous internal audit files and noted that the internal audit reports include the clause "the internal audit activity conforms with the International Standards for the Professional Practice of Internal Auditing" Upon enquiry with the CAE on the quality assurance improvement programme, the CAE stated that external quality assessment has not been done for the past eight years but the internal audit function continuously performs internal quality assessment, hence he includes that clause in the report 4 [4] 3.1.2 Mr Bell, the Director at Plastic Design Ltd, is Nkosinathi's neighbour and they have become good friends. During the procurement audit, Nkosinathi performed a conflict search on Mr Bell and identified some red flags. Mr Bell awarded a contract worth Rimillion for maintenance of generators to his brother-in-law. Upon enquiry, Mr Bell threatened to publish all personal matters Nkosinathi that he had told him on Facebook, In fear of losing his dignity and respect, Nkosinathi decided not to include the finding in the working papers and the report [4] [] 3.1.3 Nkosinathi was allocated an audit in the human resource division. The division is known for fraudulent activities and there are allegations that people had to pay bribes to be employed. The previous internal audit reports also indicated non-compliance with recruitment policies. During planning, Nkosinathi decided that he has no role to play in fraud as an internal auditor and decided not to guide his team to be aware of the potential risk of fraud in human resource division (4] () 3.1.4 The internal audit function has been receiving requests from external auditors of Plastic Designs Ltd to make available all final internal audit reports and follow-up reviews to assist them in determining and adjusting the scope of their work. The CAE ignored the request from the external auditors. 141 3.1.5 The CAE adjusted the risk-based internal audit plan due to the impact of the coronavirus pandemic on the company operations for approval by the board. In the plan, the CAE cancelled the leave management internal audit and prioritised the business continuity audit , which the CFO deemed as being irresponsible as leave management is also important [4 3.1.5 The CAE adjusted the risk-based internal audit plan due to the impact of the coronavirus pandemic on the company operations for approval by the board. In the plan, the CAE cancelled the leave management internal audit and prioritised the business continuity audit, which the CFO deemed as being irresponsible as leave management is also important. [4] 3.1.6 Maggie, an internal auditor in Plastic Designs Ltd, is part of the team that is auditing the accounts payable section. She was previously the supervisor in the account payable division and it has been eighteen (18) months since she transferred to internal audit function. There is [4] dispute between herself and the senior auditor on whether she will be objective during the audit. (TURN OVER]