Answered step by step

Verified Expert Solution

Question

1 Approved Answer

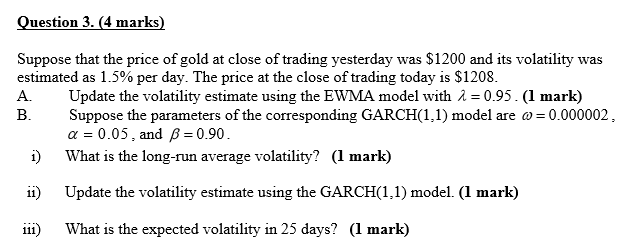

Question 3. (4 marks) Suppose that the price of gold at close of trading yesterday was $1200 and its volatility was estimated as 1.5% per

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Art Of Distressed M And A Buying Selling And Financing Troubled And Insolvent Companies

Authors: H. Peter Nesvold, Jeffrey Anapolsky , Alexandra Reed Lajoux

1st Edition

0071750193,0071750304