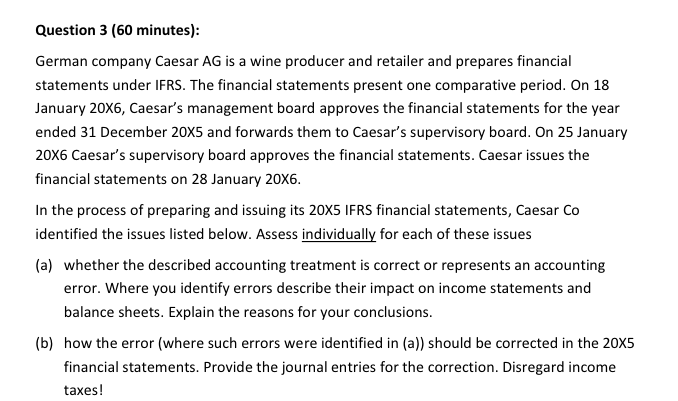

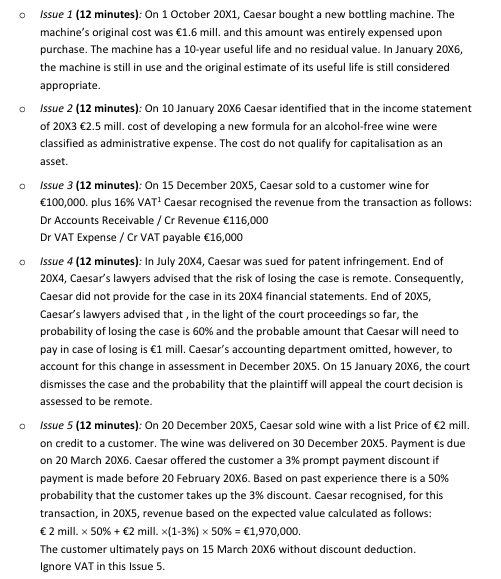

Question 3 (60 minutes): German company Caesar AG is a wine producer and retailer and prepares financial statements under IFRS. The financial statements present one comparative period. On 18 January 20x6, Caesar's management board approves the financial statements for the year ended 31 December 20x5 and forwards them to Caesar's supervisory board. On 25 January 20x6 Caesar's supervisory board approves the financial statements. Caesar issues the financial statements on 28 January 20x6. In the process of preparing and issuing its 20x5 IFRS financial statements, Caesar Co identified the issues listed below. Assess individually for each of these issues (a) whether the described accounting treatment is correct or represents an accounting error. Where you identify errors describe their impact on income statements and balance sheets. Explain the reasons for your conclusions. (b) how the error (where such errors were identified in (a)) should be corrected in the 20x5 financial statements. Provide the journal entries for the correction. Disregard income taxes! o Issue 1 (12 minutes): On 1 October 20x1, Caesar bought a new bottling machine. The machine's original cost was 1.6 mill. and this amount was entirely expensed upon purchase. The machine has a 10-year useful life and no residual value. In January 20X6, the machine is still in use and the original estimate of its useful life is still considered appropriate Issue 2 (12 minutes): On 10 January 20x6 Caesar identified that in the income statement of 20x3 2.5 mill. cost of developing a new formula for an alcohol-free wine were classified as administrative expense. The cost do not qualify for capitalisation as an asset. o Issue 3 (12 minutes): On 15 December 20X5, Caesar sold to a customer wine for 100,000. plus 16% VAT Caesar recognised the revenue from the transaction as follows: Dr Accounts Receivable / Cr Revenue 116,000 Dr VAT Expense / Cr VAT payable 16,000 Issue 4 (12 minutes): In July 20x4, Caesar was sued for patent infringement. End of 20x4, Caesar's lawyers advised that the risk of losing the case is remote. Consequently, Caesar did not provide for the case in its 20x4 financial statements. End of 20x5, Caesar's lawyers advised that, in the light of the court proceedings so far, the probability of losing the case is 60% and the probable amount that Caesar will need to pay in case of losing is 1 mill. Caesar's accounting department omitted, however, to account for this change in assessment in December 20X5. On 15 January 20X6, the court dismisses the case and the probability that the plaintiff will appeal the court decision is assessed to be remote. o Issue 5 (12 minutes): On 20 December 20X5, Caesar sold wine with a list Price of 2 mill. on credit to a customer. The wine was delivered on 30 December 20X5. Payment is due on 20 March 20X6. Caesar offered the customer a 3% prompt payment discount if payment is made before 20 February 20X6. Based on past experience there is a 50% probability that the customer takes up the 3% discount. Caesar recognised, for this transaction, in 20x5, revenue based on the expected value calculated as follows: 2 mill. x 50% + 2 mill. *(1-3%) 50% = 1,970,000. The customer ultimately pays on 15 March 20x6 without discount deduction. Ignore VAT in this issue 5