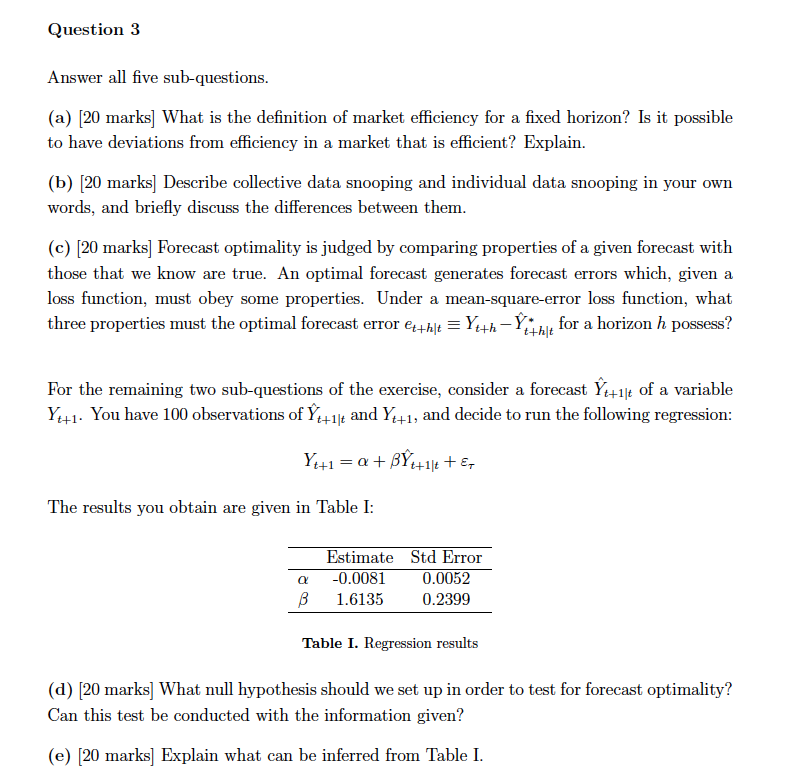

Question 3 Answer all five sub-questions. (a) [20 marks] What is the definition of market efficiency for a fixed horizon? Is it possible to have deviations from efficiency in a market that is efficient? Explain. (b) (20 marks] Describe collective data snooping and individual data snooping in your own words, and briefly discuss the differences between them. (c) (20 marks] Forecast optimality is judged by comparing properties of a given forecast with those that we know are true. An optimal forecast generates forecast errors which, given a loss function, must obey some properties. Under a mean-square-error loss function, what three properties must the optimal forecast error etthlt = Yith - Yithle for a horizon h possess? For the remaining two sub-questions of the exercise, consider a forecast Y4+1]t of a variable Y:+1. You have 100 observations of Yz+11+ and Y:+1, and decide to run the following regression: Y4+1 = a + Bd+1]++ Er The results you obtain are given in Table I: a Estimate Std Error -0.0081 0.0052 1.6135 0.2399 B Table I. Regression results (d) [20 marks] What null hypothesis should we set up in order to test for forecast optimality? Can this test be conducted with the information given? (e) [20 marks] Explain what can be inferred from Table I. Question 3 Answer all five sub-questions. (a) [20 marks] What is the definition of market efficiency for a fixed horizon? Is it possible to have deviations from efficiency in a market that is efficient? Explain. (b) (20 marks] Describe collective data snooping and individual data snooping in your own words, and briefly discuss the differences between them. (c) (20 marks] Forecast optimality is judged by comparing properties of a given forecast with those that we know are true. An optimal forecast generates forecast errors which, given a loss function, must obey some properties. Under a mean-square-error loss function, what three properties must the optimal forecast error etthlt = Yith - Yithle for a horizon h possess? For the remaining two sub-questions of the exercise, consider a forecast Y4+1]t of a variable Y:+1. You have 100 observations of Yz+11+ and Y:+1, and decide to run the following regression: Y4+1 = a + Bd+1]++ Er The results you obtain are given in Table I: a Estimate Std Error -0.0081 0.0052 1.6135 0.2399 B Table I. Regression results (d) [20 marks] What null hypothesis should we set up in order to test for forecast optimality? Can this test be conducted with the information given? (e) [20 marks] Explain what can be inferred from Table